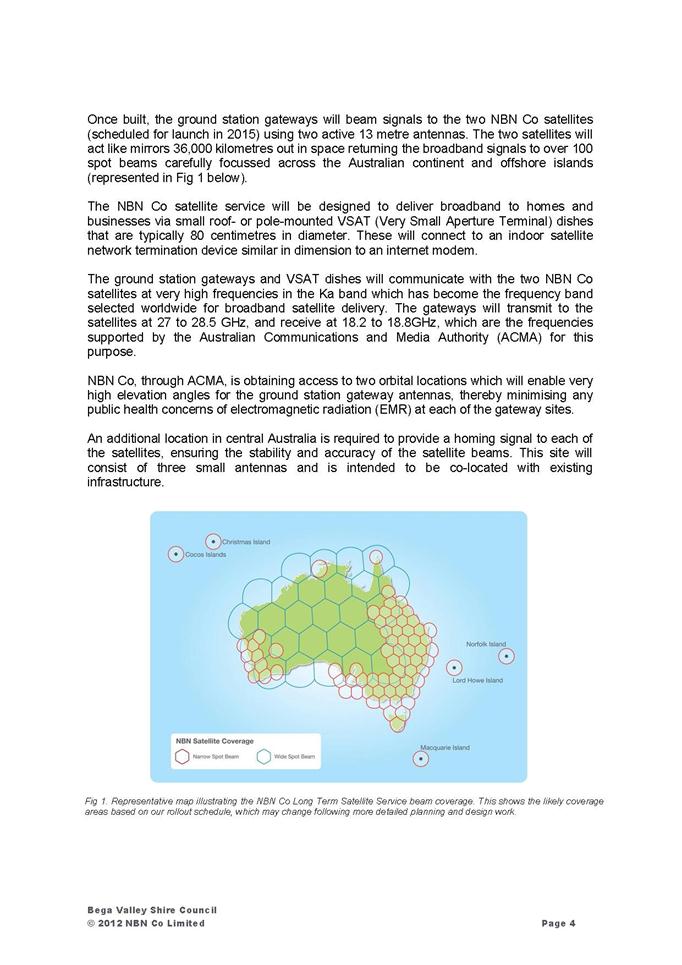

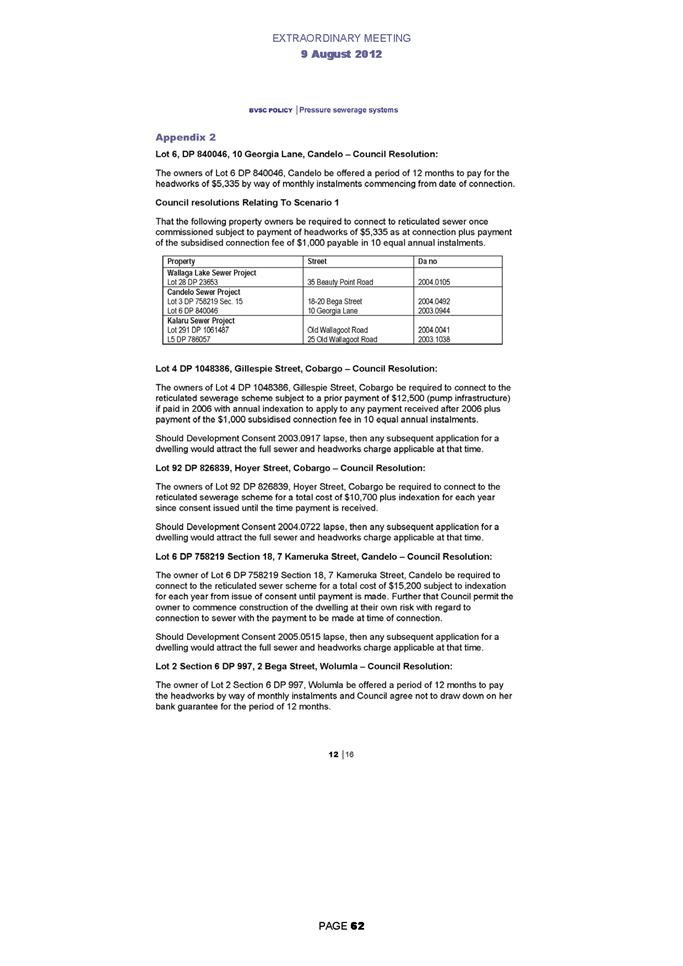

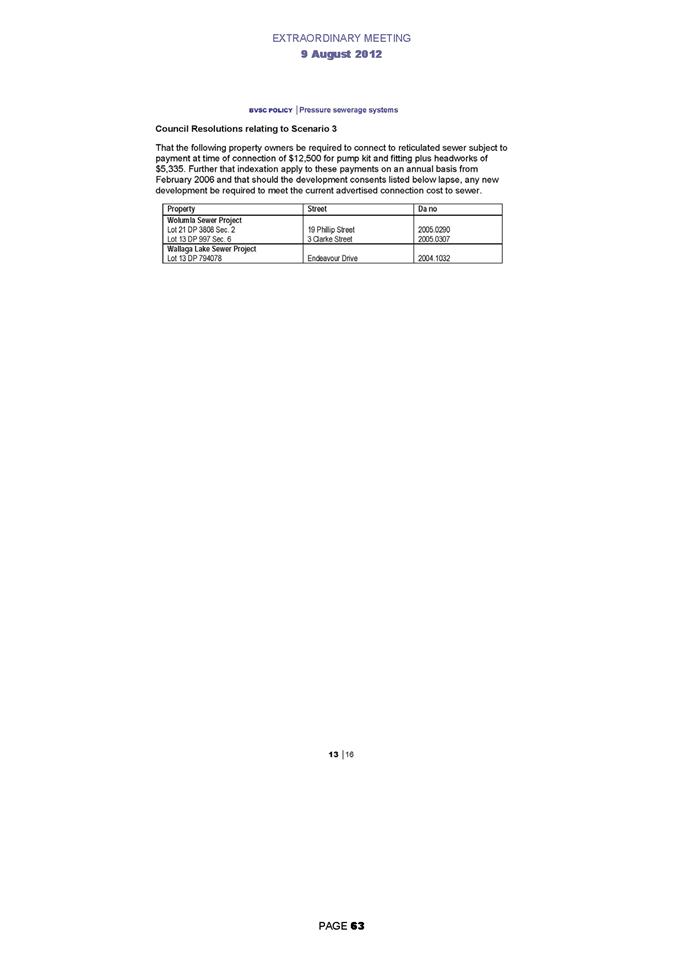

BEGA

VALLEY SHIRE COUNCIL

Ordinary

MEETING NOTICE AND AGENDA

An

Ordinary Meeting of the Bega Valley Shire Council will be held at Council Chambers,

Bega on Wednesday, 31 October 2012 commencing

at 2.00 pm to consider

and resolve on the matters set out in the attached Agenda.

Peter Tegart

General Manager

24 October 2012

|

TO:

Cr Bill Taylor, Mayor

Cr Russell Fitzpatrick, Deputy

Mayor

Cr Tony Allen

Cr Michael Britten

Cr Keith Hughes

Cr Ann Mawhinney

Cr Kristy McBain

Cr Cr Liz Seckold

Cr Sharon Tapscott

|

COPY:

General

Manager, Mr Peter Tegart

Group Manager Infrastructure, Waste and Water, Mr Wayne Sartori

Group

Manager Planning and Environment, Mr Andrew Woodley

Community and

Relationships, Ms Leanne Barnes

Minute

Secretary

|

PUBLISHING OF AGENDAS AND MINUTES

The Agendas for Council Meetings and Council

Reports for each meeting are available from 5.00 pm one week prior to each

Ordinary Meeting, on Council’s website. A hard copy is also made available to

each Library Branch and at the Bega Administration Building reception desk.

The Minutes of Committee and

Council Meetings are available from 5.00pm on Council's Web Site on the Friday

after the Meeting on Councils website and hard copies distributed with the

Agenda for the following meeting.

1. Please

be aware that the recommendations in the Council Meeting Agenda are

recommendations to the Council for consideration. They are not the resolutions

(decisions) of Council.

2. Background

for reports is provided by staff to the General Manager for his presentation to

Council.

3. The

Council may adopt these recommendations, amend the recommendations, determine a

completely different course of action, or it may decline to pursue any course

of action.

4. The

decision of the Council becomes the resolution of the Council, and is recorded

in the Minutes of that meeting.

5. The

Minutes of each Council meeting are published in draft format, and are

confirmed, with amendments by Councillors if necessary, at the next available

Council Meeting.

If you require any further

information or clarification regarding a report to Counci, please contact

Council’s Executive Assistant who can provide you with the appropriate contact

details

Phone

(6499 2104) or email execassist@begavalley.nsw.gov.au.

ETHICAL

DECISION MAKING AND CONFLICTS OF INTEREST

A GUIDING CHECKLIST FOR COUNCILLORS,

OFFICERS AND COMMUNITY COMMITTEES

Ethical

decision making

Is the decision or conduct legal?

Is it consistent with Government policy, Council’s objectives

and Code of Conduct?

What will the outcome be for you, your colleagues, the

Council, anyone else?

Does it raise a conflict of interest?

Do you stand to gain personally at public expense?

Can the decision be justified in terms of public

interest?

Would it withstand public scrutiny?

Conflict of

interest

A

conflict of interest is a clash between private interest and public duty. There

are two types of conflict:

Pecuniary – regulated by the Local Government Act

and Department of Local Government

Non-pecuniary – regulated by Codes of

Conduct and policy. ICAC, Ombudsman, Department of Local Government (advice

only). If declaring a Non-Pecuniary Conflict of Interest, Councillors can

choose to either disclose and vote, disclose and not vote or leave the Chamber.

The test

for conflict of interest

Is it likely I could be influenced by personal

interest in carrying out my public duty?

Would a fair and reasonable person believe I could be

so influenced?

Conflict of interest is closely tied to the

layperson’s definition of ‘corruption’ – using public office for private gain.

Important to consider public perceptions

of whether you have a conflict of interest.

Identifying

problems

1st Do I have private interests affected by a matter I am officially

involved in?

2nd Is my official role one of influence or perceived influence over

the matter?

3rd Do my private interests conflict with my official role?

Whilst

seeking advice is generally useful, the ultimate decision rests with the person

concerned.

Agency advice

Officers

of the following agencies are available during office hours to discuss the

obligations placed on Councillors, officers and community committee members by

various pieces of legislation, regulation and codes.

|

Contact

|

Phone

|

Email

|

Website

|

|

Bega Valley Shire

Council

|

(02) 6499 2222

|

council@begavalley.nsw.gov.au

|

www.begavalley.nsw.gov.au

|

|

ICAC

|

8281 5999

Toll Free 1800 463 909

|

icac@icac.nsw.gov.au

|

www.icac.nsw.gov.au

|

|

Division of Local Government (DPC)

|

(02) 4428 4100

|

dlg@dlg.nsw.gov.au

|

www.dlg.nsw.gov.au

|

|

NSW Ombudsman

|

(02) 8286 1000

Toll Free 1800 451 524

|

nswombo@ombo.nsw.gov.au

|

www.ombo.nsw.gov.au

|

TO: The

General Manager

Bega Valley Shire Council

Disclosure

of pecuniary interests / non-pecuniary conflict of interests

In accordance

with the Council’s Code of Meeting Practice and the requirements of the Local

Government Act and regulations or dispensation issued by the Division of

Local Government I hereby disclose the following pecuniary interests and/or

non-pecuniary conflict of interests at the meeting as indicated below:

Ordinary

meeting held on _____ / _____ / 20___

dd mm yy

|

Item no

& subject

|

|

|

Interest (tick one)

|

Pecuniary

interest Non-pecuniary

conflict of interest

|

|

* Nature of

interest

|

|

|

If

Non-pecuniary (tick

one)

|

Disclose

& vote Disclose

& not vote Leave

chamber

|

|

|

|

|

|

|

|

Item no

& subject

|

|

|

Interest (tick one)

|

Pecuniary

interest Non-pecuniary

conflict of interest

|

|

* Nature of

interest

|

|

|

If

Non-pecuniary (tick

one)

|

Disclose

& vote Disclose

& not vote Leave

chamber

|

|

|

|

|

|

|

|

Signed

|

|

|

Print Name

|

Councillor

|

* Note: Under

the provisions of Section 451(1) of the Local Government Act 1993

(pecuniary interests) and Part 6.11 of the Model Code of Conduct prescribed by

the Local Government (Discipline) Regulation 2004 (conflict of interests) it is

necessary for you to disclose the nature of the interest when making a

disclosure of a pecuniary interest or a non-pecuniary conflict of interest at a

meeting.

AGENDA

1 Confirmation Of Minutes

That the Minutes of the Ordinary

and Standing Committee Meetings held on 9 October, 2012, as circulated, be

taken as read and confirmed.

2 Apologies and requests for leave of absence

Pecuniary, Non-Pecuniary and Political Donation

Disclosures to be declared and tabled.

4 Deputations (by prior

arrangement)

7 Adjournment to Standing Committees

|

|

Recommendation

|

|

|

That the Ordinary meeting of the Council

be adjourned for the purpose of dealing with staff reports to Standing

Committees.

|

8 Staff Reports

– Planning and Environment (Sustainability)

In accordance with Council’s Code of Meeting Practice, this

section of the agenda will be chaired by Councillor Britten.

8.1 Use of Bermagui Surf Life Saving Club

as a Reception Establishment................. 13

8.2 Draft Planning Reforms................................................................................... 33

9 Staff Reports

– Community and Relationships (Liveability)

In accordance with Council’s Code of Meeting Practice , this

section of the agenda will be chaired by Councillor Seckold.

Nil Reports

10 Staff Reports –

Economic (Enterprising)

In accordance with Council’s Code of Meeting Practice, this

section of the agenda will be chaired by Councillor McBain.

10.1 National Broadband Network........................................................................... 93

11 Staff Reports –

Infrastructure Waste and Water (Accessibility)

In accordance with Council’s Code of Meeting Practice, this

section of the agenda will be chaired by Councillor Fitzpatrick.

11.1 Bega Valley Local Traffic Committee

Meeting 10 October 2012........................ 115

11.2 Water Allocation Payments to

Sportsground Committees................................ 117

11.3 Developer Charges Guidelines for

Water Supply and Sewerage (Consultation Draft) 121

11.4 Tender 26/12 Littleton Gardens Public

Toilet................................................... 165

11.5 Bega Town Hall Expression of Interest

(Stage 2)............................................. 169

12 Staff Reports –

Governance and Strategy (Leading Organisation)

In accordance with Council’s Code of Meeting Practice, this

section of the agenda will be chaired by Councillor Mawhinney.

12.1 Certificate of Investments made under

Section 625 of the Local Government Act 1993 181

12.2 Pecuninary Interest Returns 1 July

2011 to 30 June 2012................................. 185

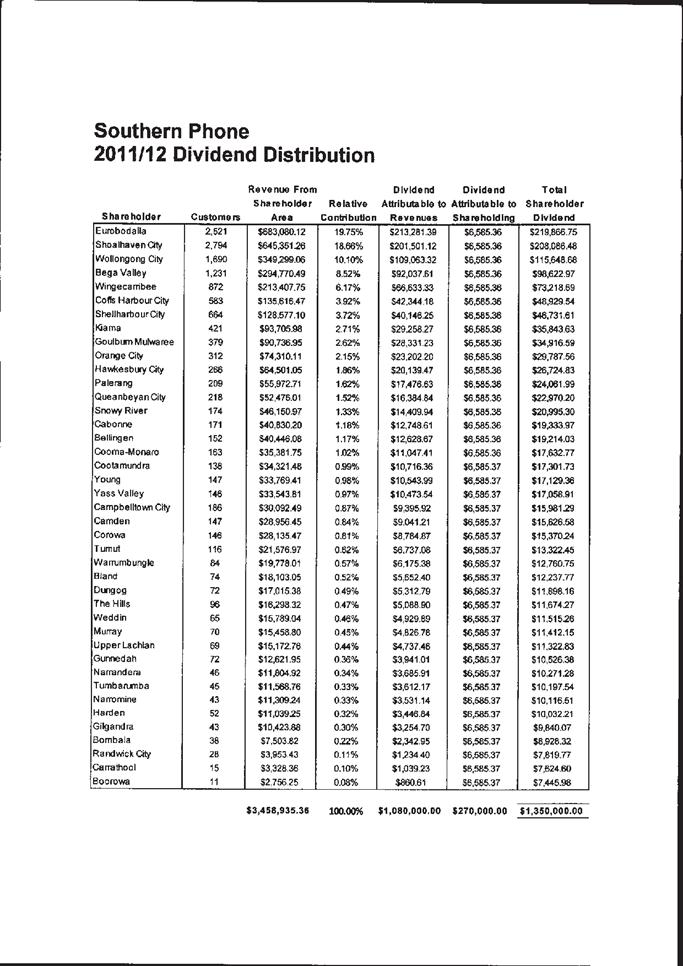

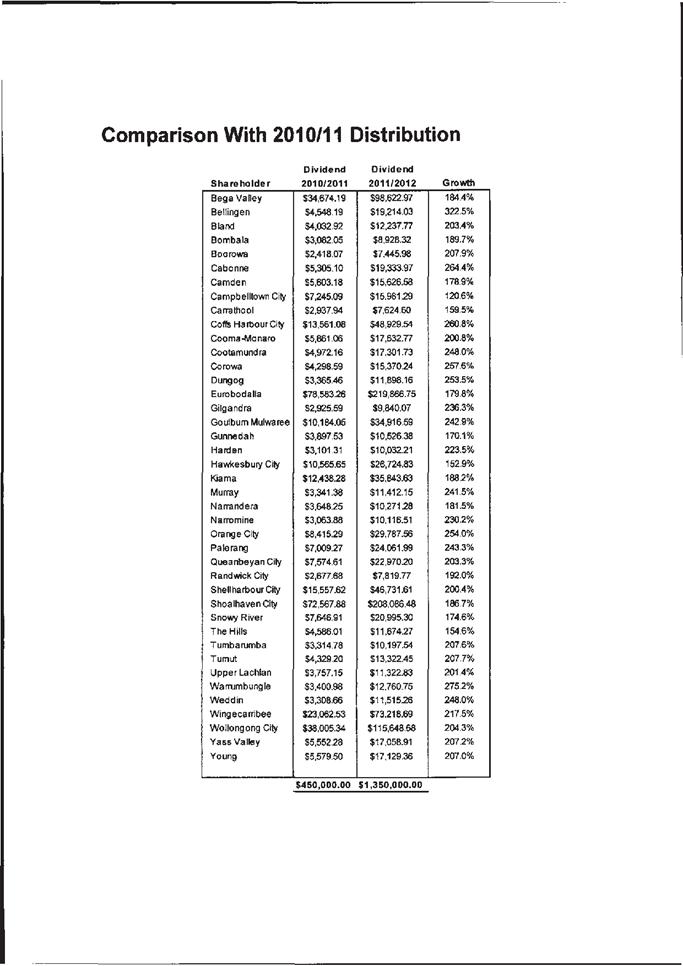

12.3 Southern Phone Company Dividend............................................................... 189

12.4 Australian Local Government Women’s

Association (ALGWA) NSW Branch – State Conference 193

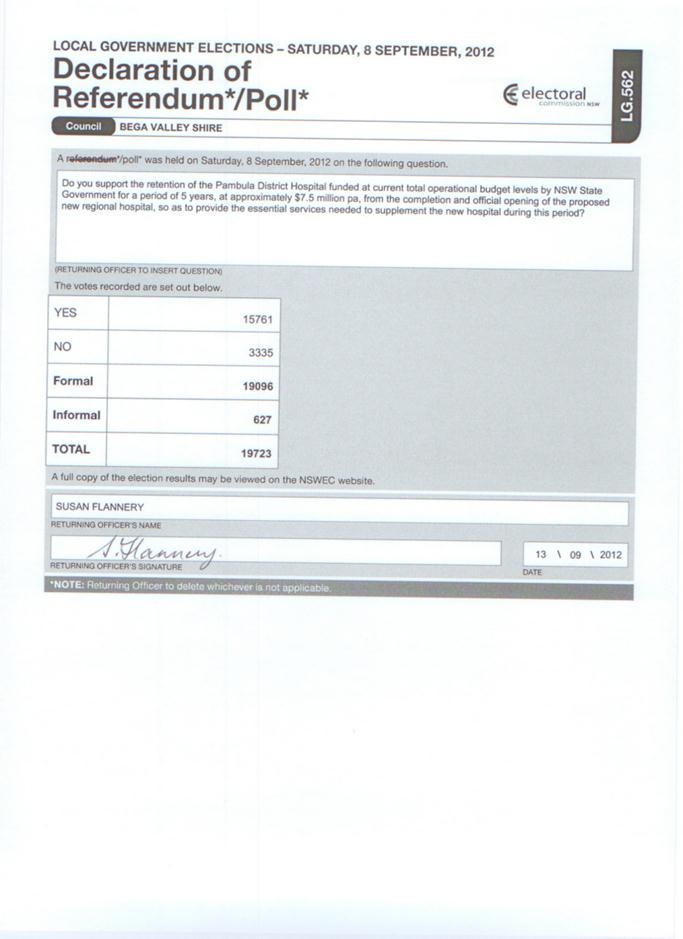

12.5 Result of Hospital Poll - Local

Government Elections....................................... 203

12.6 Local Government Infrastructure

Renewal Scheme (LIRS) Funding Update......... 207

12.7 Community strategic plan review -

community survey and special rate variation process 287

12.8 Quarterly Budget Review Statement for

30 June 2012...................................... 303

12.9 Presentation of Financial Statements

and Audit report for the year ended 30 June 2012 313

12.10 Presentation of Draft Financial

Statements for the year ended 30 June 2012.... 315 .

13 Adoption of Reports

from Standing Committees

15 Rescission/alteration

Motions

16.1 Cobargo Public Toilets.................................................................................. 327

16.2 Wolumla Public Toilets................................................................................. 329

18.1 Cr Fitzpatrick Lake Curalo Boardwalk ............................................................ 333

18.2 Cr Fitzpatrick - Native Vegetation

Act............................................................. 335

19 Questions for the

Next Meeting

20.. Confidential

Business

21 Adoption of reports

from Closed Session

22 Resolutions to

declassify reports considered in closed session

staff

reports – Planning and Environment (Sustainability)

31 October

2012

In accordance with Council’s Code of Meeting Practice

(2011), this section of the agenda will be chaired by Councillor Surname.

8.1 Use

of Bermagui Surf Life Saving Club as a Reception Establishment..... 13

8.2 Draft

Planning Reforms.................................................................................... 33

Council 31 October 2012 Item

8.1

8.1. DA 2012.149:

Use of Bermagui Surf Life Saving Club as a Reception Establishment

Group Manager Planning & Environment

|

Applicant

|

Bermagui Surf Life Saving Club

|

|

Owner

|

Department of Primary Industries (Catchments &

Lands)

|

|

Site

|

Lot 7305 DP 1128706 and Lot 7034 DP 1118743 within

Dickinson Reserve 83225, off Lamont Street, Bermagui

|

|

Zone

|

6(a) Existing Open Space

|

|

Site

area

|

5.4ha

|

|

Proposed

development

|

Use of Bermagui Surf Life Saving Club as a Reception

Establishment

|

Precis

Council is in receipt of a

development application seeking consent for the use of the Bermagui Surf Club building

(a Community Facility) as a Reception Establishment under the provisions of

Clause 71 of Bega Valley Local Environmental Plan 2002 (BVLEP 2002).

The application is reported to

Council for determination due to the broader issues raised with the proposed

use of a Community Facility as a reception establishment, catering for private

functions.

Objections to the proposal were

received during public exhibition.

The proposal is recommended for

approval.

Background

In May 2007 Council consented to

the construction of the Surf Life Saving Club building within Dickinson

Reserve, Bermagui. Construction of the building commenced in January 2009 and

Interim Occupancy was issued on 25 May 2012. There are a number of matters that

remain outstanding for the Final Occupation Certificate, and these matters are

being actively attended to by the Club.

Description of

the proposal

Consent is sought for the building

to be used as a Reception Establishment for up to 18 times per year. The

applicant originally sought approval for up to 28 days per year but this was

reduced to 18 during the assessment of the application. The proposal would

require upgrading of the existing kitchen to a commercial grade suitable for

catering purposes. It is also proposed to install a bar area at the eastern end

of the hall. The application proposes hours of operation up until 12.30am, with

service of alcohol to cease at 11.30pm (as per the Club’s current liquor

licence) and music to cease at 11.40pm. The maximum number of patrons is

proposed at 120 persons for seated functions and 200 persons for cocktail

functions.

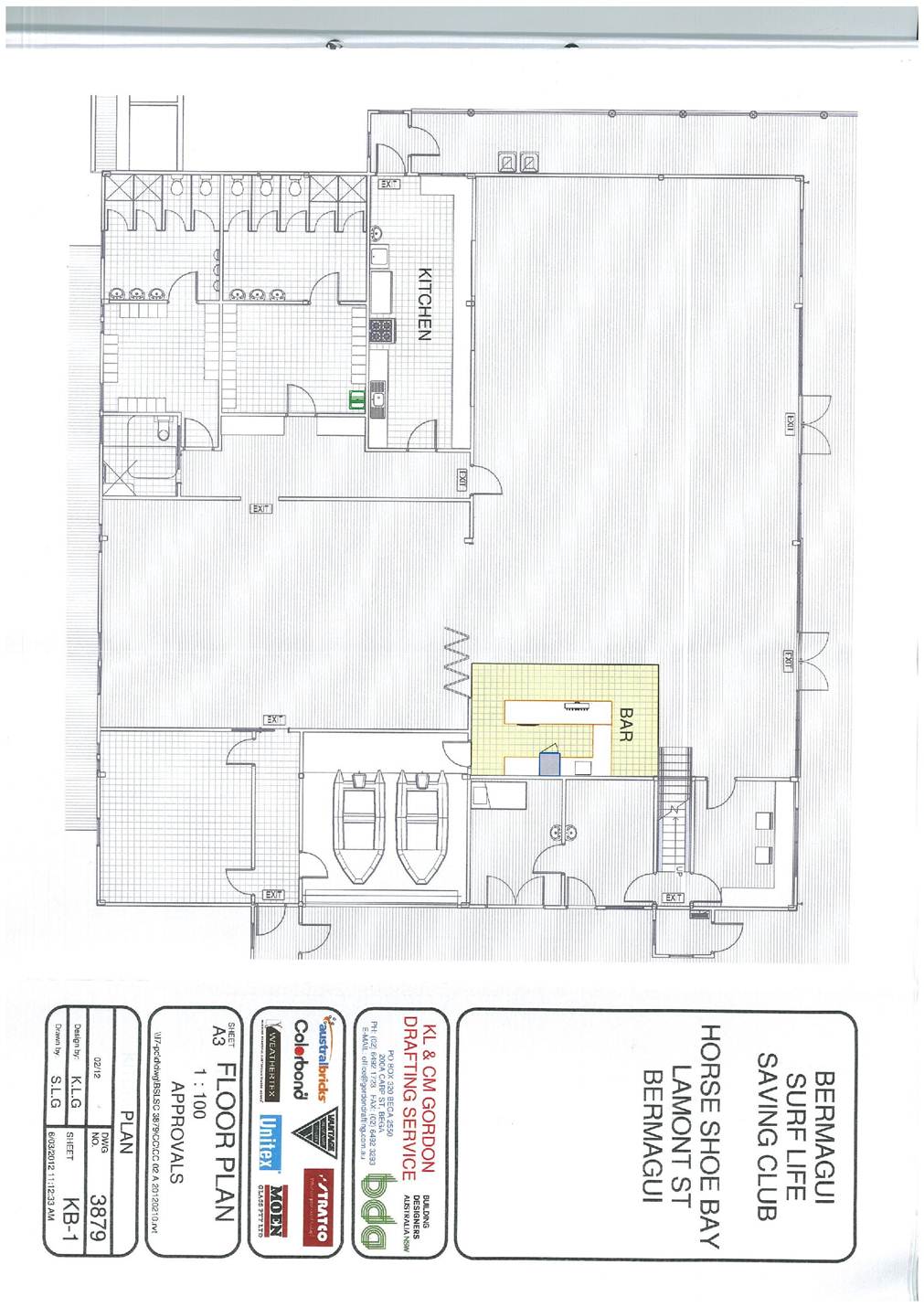

A copy of the submitted development

plan is provided as Attachment 1.

Description of

the site

The surf club building is located

within Dickinson Park Reserve, immediately adjacent to the existing amenities

block. The Reserve is bounded by Horseshoe Bay to the north, the Lamont Street

business precinct to the south-east and the oval facilities to the south and

south-west.

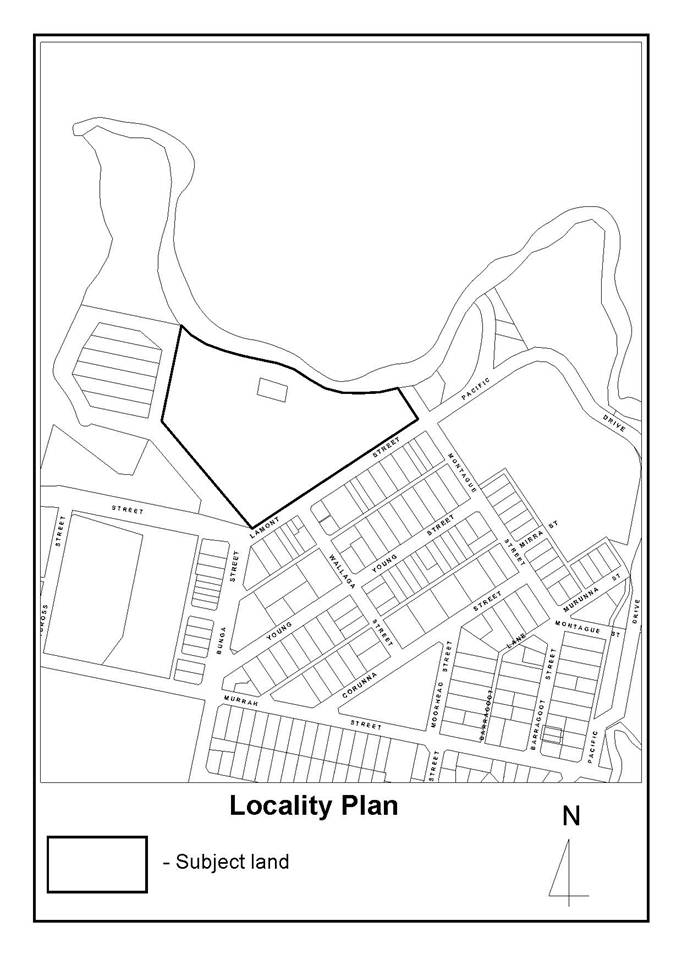

A locality plan is provided as

Attachment 2.

Planning

assessment

The proposal has been assessed in accordance with the

Matters for Consideration under Section 79C of the Environmental Planning and

Assessment Act 1979. Staff highlight the key issues of the proposal in this

report for Council’s consideration.

A copy of the assessing officer’s Section 79C assessment

will be available at the meeting.

Zoning

Bega Valley Local Environmental

Plan 2002

The subject land is zoned 6(a)

Existing Open Space under the provisions of BVLEP 2002. The proposed use is

defined as a Reception Establishment, which means;

A

building or place used for the purpose of wedding receptions, birthday parties

and the like where admission is by private invitation, but does not include a

refreshment room or hotel.

Reception Establishments are prohibited

in the 6(a) zone. The applicant has requested the proposed use be considered in

accordance with Clause 71 of BVLEP 2002, under the provisions of temporary use

of land. Clause 71 states:

“71 Temporary use of land

Despite any other provision of this plan, consent may be

granted to the carrying out of development for the purpose of a street stall or

carnival or to other temporary development in any zone for a maximum period of

28 days, whether consecutive or not consecutive, in any one year.“

This issue will be discussed later in this report.

Notwithstanding the land use being

prohibited in the zone, the objectives of the zone are relevant and must be

considered in the determination of the application.

The objectives of the 6(a) zone are

as follows;

(a) to recognise the importance of land in the

zone as open space and allow a limited range of uses compatible with the

keeping of the land as open space and in public ownership,

(b) to

permit a range of uses, especially recreational uses, where those uses comply

with the plan of management of the land,

(c) to

ensure that development in areas of environmental significance does not reduce

that significance.

For the purpose of Clause 8(3) and

38(2) of BVLEP 2002, the proposed use of the Surf Club building as a Reception

Establishment to enable wedding receptions, birthday parties and the like, is

considered to be consistent with the objectives of the 6(a) zone.

The proposed use provides an

additional income source for the Club to maintain the Surf Club building and

secure its continued primary function as a Community Facility, being for the

physical, social, cultural, economic or intellectual development or welfare of

the local community.

The proposed use is not expected to

conflict or take away from the main use of the reserve, being for passive and

active recreation. Most of the proposed private functions to be conducted at

the Surf Club building would occur in the evening, when the public use of the

reserve is limited. The proposed reception establishment would allow for either

the Surf Club building to be hired to private caterers to come in and use the

kitchen facilities to service a function, or allow the Surf Club Committee to

provide catering to functions, at a fee.

It is considered that the proposal

complies with the applicable plan of management (see later discussion of

issues).

It is considered that the proposal

would not reduce the environmental significance of the Reserve setting and

surrounds.

Draft Bega Valley Local

Environmental Plan 2012

The subject site is proposed to be

zoned RE1 Public Recreation under Draft Bega Valley Local Environmental Plan

2012 (Draft BVLEP 2012). The proposed land use would be defined as a Function

Centre under the Standard Instrument definitions, which means;

A

building or place used for the holding of events, functions, conferences and

the like, and includes convention centres, exhibition centres and receptions

centres, but does not include an entertainment facility.

Function Centres would be

prohibited in the RE1 zone. Notwithstanding, consideration of a temporary use

can be made under Clause 2.8 of Draft BVLEP 2012. This matter is discussed in

more detailed later in this report.

The objectives of the RE1 zone are;

· To enable land to be used for

public open space or recreational purposes.

· To provide a range of

recreational settings and activities and compatible land uses.

· To protect and enhance the

natural environment for recreational purposes.

It is considered that the proposed use of the Surf Club

building for the purpose of conducting non-surf club functions, such as

weddings and birthday parties, would be a compatible activity within the

recreation reserve. It is unlikely that such functions would adversely impact

on the other reserve uses during day time or evening events. Suitable

conditions of consent are recommended to control activities, in terms of noise,

hours of operation and service of alcohol. In this regard, the proposal is

considered to be consistent with the objectives of the proposed RE1 zone.

Issues

Permissibility

of proposed land use

The building was approved as a

Community Facility (erection

of a building for the purpose of a surf life saving club and radio control

room). A Community Facility is defined by BVLEP 2002 as;

a

building or place owned or controlled by a public authority or a body of

persons associated for the purpose of providing for the physical, social,

cultural, economic or intellectual development or welfare of the local

community, but does not include a building or place (other than a club)

elsewhere specifically defined in this Dictionary.

A condition of consent was included

on the development consent (2006.508) for the surf club, limiting the uses of

the building. Condition 33 states;

The

Club Room and Training Room shall be used for Surf Club or community based

purposes only.

The Club now seek to upgrade the

kitchen area to a commercial grade kitchen and to include a bar area to be able

to hold private functions in the hall area of the Club building, such as

weddings and birthday parties.

Clause 71 allows Council to

consider temporary uses that would otherwise be prohibited in the zone. Clause

71 states;

Despite

any other provision of this plan, consent may be granted to the carrying out of

development for the purpose of a street stall or carnival or to other temporary

development in any zone for a maximum period of 28 days, whether consecutive or

not consecutive, in any one year.

Draft Bega Valley Local

Environmental Plan 2012 (Draft BVLEP 2012) also contains a clause which permits

temporary land uses with the consent of Council. The assessment of the proposal

in light of Clause 2.8 of Draft BVLEP 2012 is relevant as the gazettal of the

plan is considered to be imminent as at the time of writing this report.

Clause 2.8 of Draft BVLEP 2012

states;

2.8 Temporary

use of land

(1) The

objective of this clause is to provide for the temporary use of land if the use

does not compromise future development of the land, or have detrimental

economic, social, amenity or environmental effects on the land.

(2) Despite

any other provision of this Plan, development consent may be granted for

development on land in any zone for a temporary use for a maximum period of 52

days (whether or not consecutive days) in any period of 12 months.

(3) Development

consent must not be granted unless the consent authority is satisfied that:

(a) the

temporary use will not prejudice the subsequent carrying out of development on

the land in accordance with this Plan and any other applicable environmental

planning instrument, and

(b) the

temporary use will not adversely impact on any adjoining land or the amenity of

the neighbourhood, and

(c) the

temporary use and location of any structures related to the use will not

adversely impact on environmental attributes or features of the land, or

increase the risk of natural hazards that may affect the land, and

(d) at

the end of the temporary use period the site will, as far as is practicable, be

restored to the condition in which it was before the commencement of the use.

(4) Despite

subclause (2), the temporary use of a dwelling as a sales office for a new

release area or a new housing estate may exceed the maximum number of days

specified in that subclause.

(5) Subclause

(3) (d) does not apply to the temporary use of a dwelling as a sales office

mentioned in subclause (4).

The objective of the clause

It is considered that the proposed

use of the Bermagui Surf Club building for the purpose of a Reception

Establishment, which would enable the Club to hire the premises for the purpose

of weddings, birthdays and the like, would not compromise the future

development potential of the land. The land is located within Dickinson Reserve

of which Council is Trustee and is managed under the Bermagui Foreshore

Reserves Plan of Management 2004 (PoM).

The Plan of Management establishes

objectives which specify what is to be achieved within the subject land. The

‘Tourism/Commercial’ Values’ of the PoM state (p.24);

· Ensure a sustainable tourism

industry by careful planning to maintain and enhance those natural qualities

that attract visitors to the area without disadvantaging the permanent

residents of Bermagui.

· Allow for commercial enterprise

on foreshore land where such enterprise is appropriate to its environmental and

social settings and where a clear net gain to the community can be

demonstrated.

The Club submit that the proposal

will provide a net gain to the community in being able to secure income which

will enable the Club to service its debts and to continue to fundraise for

essential surf life saving equipment.

Temporary use not to prejudice

the subsequent carrying out of development on the land

As the use would be conducted

wholly within the confines of the Surf Club building, it is considered that

there would be no significant impact on the development potential of adjoining

reserve lands.

No adverse impact on any

adjoining land or the amenity of the neighbourhood

It is considered that there would

be minimal adverse impact on adjoining lands. The Surf Club building sits

within the Reserve which enables a suitable buffer to adjoining businesses and

residential properties beyond. Specific conditions of consent are recommended

which define hours of operation and ensure strict compliance with the

responsible service of alcohol.

There is adequate car parking

available within the Reserve (both formal and informal) to cater for the

proposed functions without adversely impacting on the on-street parking in

Lamont Street.

In terms of noise impact, the

proposal would be required to comply with the provisions of the NSW Industrial

Noise Policy and the Protection of the Environment Operations Act.

No adverse impact on environmental

attributes or features of the land, or increase the risk of natural hazards

that may affect the land

There is no envisaged adverse

impact on any environmental attributes or features of the land as a result of

the proposed development.

The site will, as far as

practicable, be restored to the condition in which it was before the

commencement of the use

As the proposal relates to a use of

a building, that use can cease at any time without impact on any of the

facilities provided within the building or the reserve. The upgraded kitchen

and bar area would still be able to be used by normal surf club functions and

currently permissible community uses.

Summary

Whilst Council can consider the use

of the building for the purpose of a Reception Establishment up to 28 days per

year under the current LEP and up to 52 days under the Draft LEP, the Club seek

development consent for up to 18 days per year.

The proposal is considered to be a

minor use of the premises, which primary function is to provide surf life

saving services to the community and as a venue for use by community groups.

The proposal is considered to be a

reasonable use of this community asset.

Asset

Council is Trustee of the subject reserve and the building

is leased to Bermagui Surf Life Saving Club Incorporated under a license

agreement. The license agreement would need amendment to permit the hire of the

premises by non-community groups (ie for private functions).

Consultation

The proposal has been considered by

the Department of Lands as the owner of the land. No objection is raised by

Lands in relation to the proposed use.

Submissions

The development application was

placed on exhibition for a period of 14 days from 6 June 2012 until 20

June 2012. A total of three submissions were received in relation to the

development.

The key issues raised in

submissions are discussed below followed by staff comment.

A copy of the submissions will be

available at the Council meeting.

I

object to having to compete in a limited market place with individuals who are

using a public facility and have no risks attached.

It

simply is not a level playing field when competing for the same wedding or

function.

Every

time the Life Saving Club undercuts us to host a wedding at least 10 staff will

not be working at Mimosa that night.

Mimosa

Wines request that you do not cater to the whims of a club whose primary

objective while essentially worthy, with this proposal goes beyond the

boundaries of sustaining a supposedly not for profit organisation at the

expense of the local business community.

COMMENT:

The impact on existing businesses within the township as a

result of the proposed development, in terms of business competition, is not a

matter for Council in its planning consent authority role.

Notwithstanding, the Club have reconsidered their initial

application for a maximum of 28 days per year and have agreed to limit the

number of non-community events to 18 per year. The Club does not seek to

compete directly with other function centres in the local area but offer an

alternative venue for the community to hold functions. The Club has indicated

that their primary purpose is conducting surf life saving functions and seeks

to utilise the asset in a viable way to provide financial sustainability.

The

surf club has been used for several receptions already. I would like the noise

from music to cease at 10pm – as I sell sleep.

COMMENT:

The applicant seeks consent for hours of operation up to

12.30am, with music to finish at 11.40pm and service of alcohol to finish at 11.30pm

(as per the current liquor licence). The objection from the proprietor of the

Beachview Motel in Lamont Street suggests that music from functions should

cease at 10pm.

Assessing staff recommend the inclusion of Councils standard

condition for licensed premises which states;

The

LA10 noise level emitted from the licensed premises should not exceed the

background noise level by more than 5dB(A) from 7am to midnight and shall not

exceed the background level from midnight until 7am. No correction for tonality

is applied. Measurement is taken at the boundary of the worst affected

premises.

This would ensure the premises complies with the provisions

of the Environment Protection Authority NSW Industrial Noise Policy at

all times.

Given the separation distance between the Surf Club and the

Motel and the fact that the Motel is located within a commercial precinct and

adjoining other licensed premises, staff consider it unreasonable to impose a

10pm curfew on music.

Any concerns raised in relation to noise from the subject

premises would be appropriately investigated by Council officers in accordance

with the Protection of the Environment Operations Act and the NSW industrial

Noise Policy.

We

are concerned that there appears to have been no proper notice of the proposal

to turn a volunteer surf club into a potentially large commercial business

competing directly with struggling private small business.

COMMENT:

Notification of all properties along Lamont Street between

Montague and Wallaga Streets was undertaken, a notice placed in the local

newspapers and all documentation displayed at the Bermagui Library for viewing

by the public. The provisions of Councils Development Control Plan No. 3 –

Notification have been satisfied in this regard.

As

a reception venue and bar the club will directly compete with struggling

businesses in and around Bermagui. In this regard we note that the club has not

had to pay for its land or its buildings and is staffed by volunteers. It has

received extremely generous Government grants and as far as we are aware it

pays no land tax or rates. In other words it has virtually none of the

overheads, capital expenses or running costs of the businesses it will directly

compete with.

COMMENT:

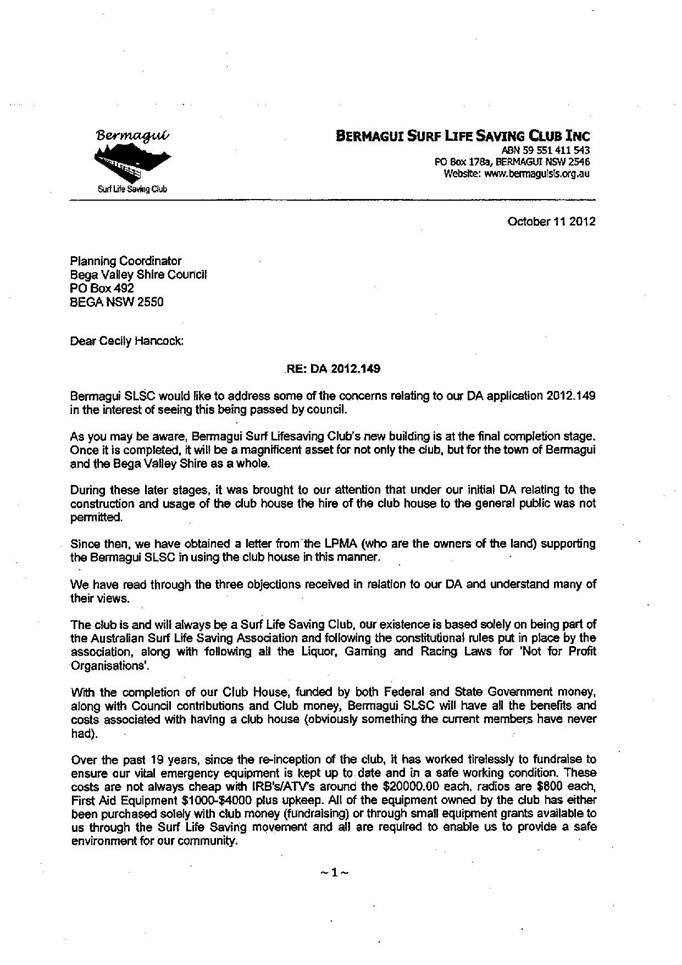

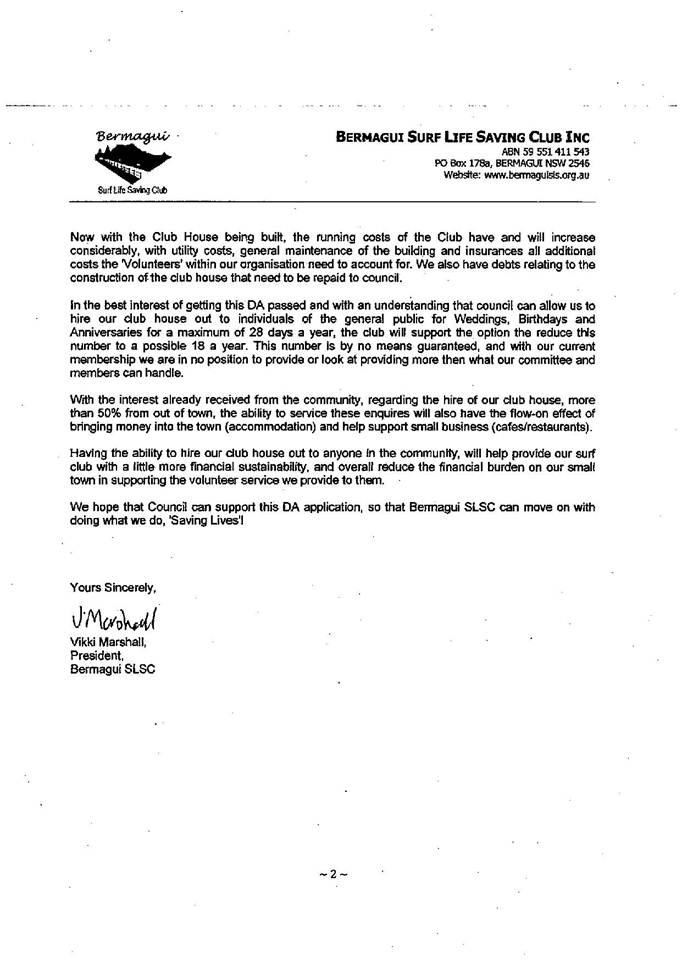

A copy of a letter from the Bermagui Surf Life Saving Club

in response to submissions is provided as Attachment 3 to this report.

As mentioned previously in this report, the impact on

existing businesses within the township as a result of the proposed

development, in terms of business competition, is not a matter for Council in

its planning consent authority role.

conclusion

The proposed development application has been assessed in

accordance with the relevant Matters for Consideration under Section 79C of the

Environmental Planning and Assessment Act 1979.

Whilst Reception Establishments are prohibited in the zone,

the provisions of BVLEP 2002 allow the consent authority to consider the use up

to 28 days per year. The Club, in considering the concerns raised in

submissions, only propose to operate up to 18 days per year.

The proposal is considered to be consistent with the

objectives of the zone and is not considered to adversely conflict with the

principles of the Bermagui Foreshore Reserves Plan of Management.

In this regard, the proposal is recommended for approval

subject to conditions as outlined in Attachment 4 to this report.

ATTACHMENTS

1View. Proposed development

plan

2View. Locality Plan

3View. Letter from Bermagui

Surf Life Saving Club

4View. Draft Consent

|

Recommendation

1. That

Development Application 2012.149 for the use of the Bermagui Surf Life Saving

Club (a Community Facility) as a Reception Establishment for up to 18 days

per year at Lot 7305 DP 1128706 and Lot 7034 DP 1118743 within Dickinson

Reserve 83225, off Lamont Street, Bermagui be approved subject to conditions

outlined in the draft consent.

2. That those persons who made a submission be

advised of Council’s decision.

|

|

Council

|

31

October 2012

|

|

Item 8.1 - Attachment 1

|

Proposed development plan

|

|

Council

|

31

October 2012

|

|

Item 8.1 - Attachment 2

|

Locality Plan

|

|

Council

|

31

October 2012

|

|

Item 8.1 - Attachment 3

|

Letter from Bermagui Surf Life

Saving Club

|

|

Council

|

31

October 2012

|

|

Item 8.1 - Attachment 4

|

Draft Consent

|

2.

Council 31 October 2012 Item

8.2

8.2. Draft

Planning Reforms

To provide Council with an overview of the Draft

Planning Reforms contained in the Green Paper published by the NSW Government.

Group Manager Planning & Environment

Background

The NSW Government has been undertaking a review of the

Environmental Planning and Assessment Act over the past 9 months. The

Government has released a “Green Paper” which broadly sets out the proposed

changes to be introduced into a new Planning Act.

“Frequently asked questions for councils” as published by

the Government is attached, as is the response to the Green Paper by the NSW

Local Government & Shires Associations.

ISSUES

The Environmental Planning and Assessment Act was introduced

in 1979 and commenced in 1980. The Act has been amended over 150 times since

its introduction and has become very difficult to interpret, to implement and

to explain to the community. It has also become unwieldy for applicants wishing

to undertake development.

The review was undertaken by a former Minister for the

Environment, Tim Moore, and a former Minister for Public Works, Ron Dyer. Both

are lawyers and Mr Moore is also a Town Planner. As part of the review there

were many community forums held across NSW involving approx. 2000 people. There

were also 900 written submissions received.

The review resulted in a two volume report which included

issues and recommendations. The Government responded with the release of the

Green Paper, which was on exhibition until 5 October 2012. Council wrote a

submission requesting that, as the new Council was not meeting until after the

closing date, this should be extended. The Minister for Planning responded

indicating that he was not prepared to agree to an extension.

Legal

A new Planning Act will have significant ramifications

across NSW and, in particular, for Local Government. At this stage there is

very little available to guide Council in terms of the legal aspects. However,

it will mean a whole new set of precedents will be set by the Land and

Environment Court. The Department of Planning and Infrastructure will also have

to provide new policies and guidelines. Consequently these precedents will take

many years to evolve.

It is considered that Council will need to provide for a

larger legal budget as it is considered that many more legal opinions will need

to be sought.

Policy

Whilst it is not specifically known what changes will be

necessary Council will most probably need to again review its Local

Environmental Plan and Development Control Plan.

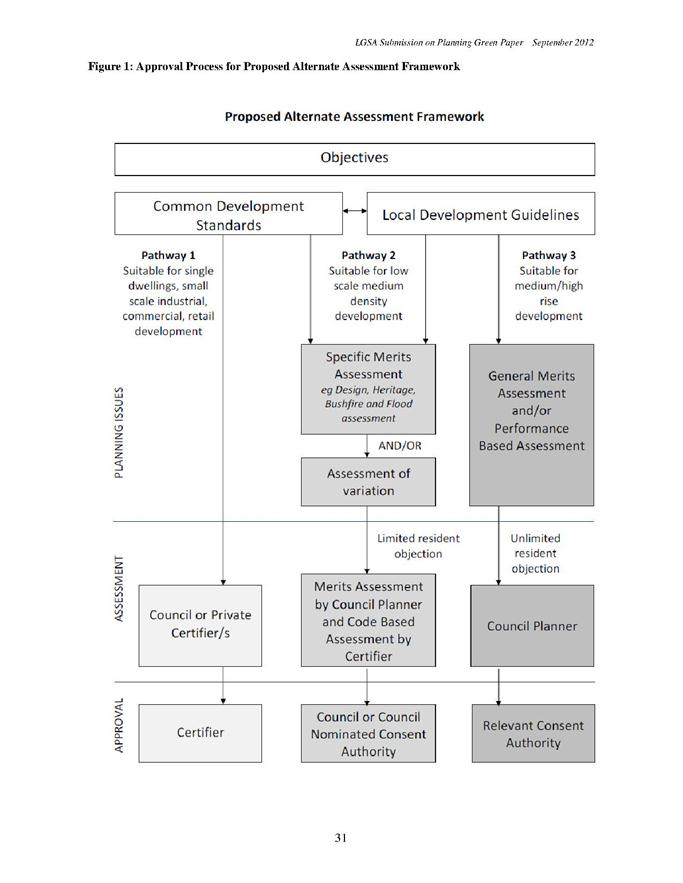

The Green Paper is divided into four (4) key reform areas.

These areas are:-

Community Participation where the following is

proposed;

- Establishment of a public

participation charter,

- Imposing a statutory

requirement for consultation on strategic planning documents relating to

sub-regional planning;

- Ensuring that there is a plain

English explanation of all planning documents;

- Ensuring that there is a

genuine and effective community consultation and stakeholder involvement;

- Adoption of evidence based

planning;

- Ensuring that there is a “clear

line of sight” through the hierarchy of plans;

- Increased use of the Planning

Assessment Commission (PAC), Joint Regional Planning Panels (JRPP) and local

expert panels “in order to take politics out of decision making”;

- Make

strategic plans and policies and information relating to development

applications and approvals available on line.

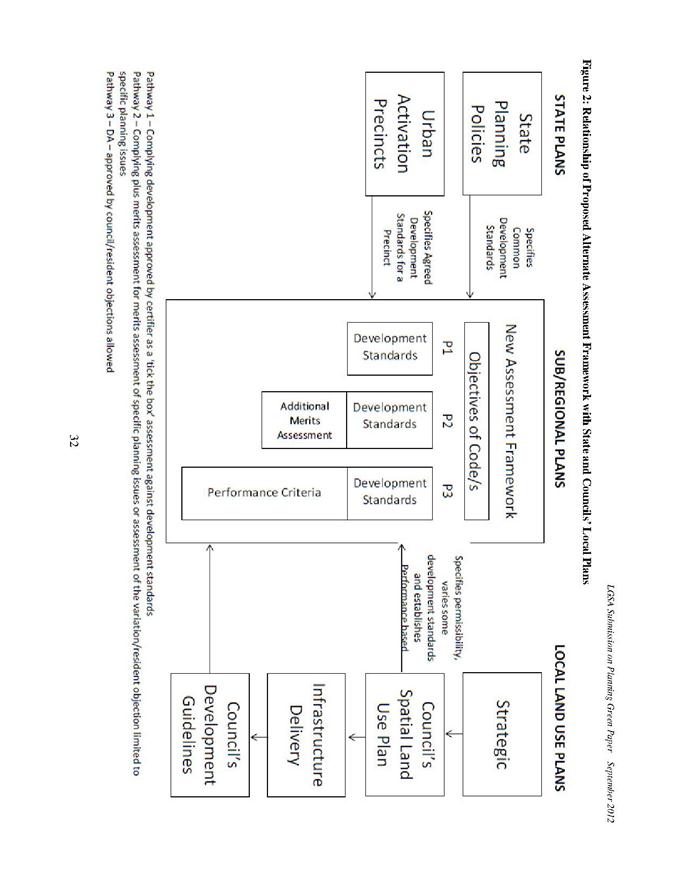

Strategic Planning

- 10-12 consolidated

non-statutory NSW Planning policies will replace the myriad of existing State

Environmental Planning Policies (SEPPs) and Ministerial Section 117 directions;

- Development controls in SEPPs

will be collapsed into local land use plans and guidelines or incorporated into

subregional delivery plans;

- Non statutory regional growth

plans with a 20 year horizon, identifying development capacities scenarios and

targets, supported by market and feasibility data and containing 10 year growth

targets for subregions will be introduced;

- Sectorial strategies and growth

infrastructure plans underpinning sub regional delivery plans will be

introduced;

- Regional planning boards will

be formed on a regional basis and will determine how subregions meet their

obligations through subregional delivery plans;

- Plain English Local Land Use

Plans (LLUPs) will be introduced in four parts 1) an explanation of the

strategic planning framework, 2) a spatial land use plan, 3) an outline of

infrastructure requirements, and 4) development guidelines;

- Councils will be allowed to

amend Local Land Use Plans subject to consistency with the higher order plans;

- Existing Development Control

Plans will be abolished and replaced with development guidelines contained in

the LLUP;

- Three new zones will be

introduced. These will be an Enterprise Zone, a Future Urban Release Area Zone

and a Suburban Character Zone;

- Land

use zones will generally be more flexible.

Development Assessment and

Compliance

- There will be a hierarchy of

“generally depoliticised decision makers”;

- The PAC and JRPP will determine

applications to carry out State Significant Development (SSD) and regional

development respectively;

- Local expert panels, council

officers or accredited certifiers will determine applications to carry out

local development depending on whether the development is merit assessable or

code assessable;

- Code assessment will be

introduced for development that conforms with a subregional delivery plan and

must be approved within a prescribed timeframe;

- Code assessment development

will be either “consent authority code assessment” or “accredited certifier

code assessment”;

- Strategic compatibility

certificates issued by the Director General (DG) of the Department of Planning

and Infrastructure will enable conforming development to go ahead in the

absence of a subregional delivery plan;

- JRPPs will be allowed to review

the DG’s decision not to issue a strategic compatibility certificate;

- Different components of the one

development project will be able to be code assessable or merit assessable;

- For

multi-stage development, code assessment will be able to follow the approval of

a concept plan for the development.

Infrastructure Planning and

Co-ordination

- The private sector will be able

to design, fund, deliver, manage and operate infrastructure in growth areas;

- Competitive tendering will be

introduced in growth areas to facilitate private sector participation in

infrastructure provision;

- Voluntary Planning Agreements

(VPAs) might be phased out or significantly changed and, if kept, could be

linked to larger precinct development and governed by clear minimum benchmarks;

- A new development contributions

framework will be introduced based on key principles including cost recovery,

competiveness, housing affordability and delivery, beneficiary pays, spreading

of costs, contestability and transparency;

- The development contributions framework

will possibly comprise 1) a local infrastructure levy 2) a regional open space

levy and 3) a regional infrastructure levy in high growth areas;

- Levies

will be payable as late as practically achievable in the development process.

Strategic/Financial

Implications

The changes proposed will have a very large impact on the

work undertaken by Council’s planning staff. Until more details are available

it is not possible to give any precise indication of the implications.

Operational

Plan

The impact on the Operational Plan is yet to be determined.

What is Next?

The Green Paper will be followed before the end of the year

by a White Paper and Exposure Bill which includes the draft legislation. Both

documents will be open to submission.

Conclusion

Given that the newly elected Council was not in a position

to make a submission to the Green Paper, it is expected that Council may wish

to workshop and make a submission at the White Paper stage.

ATTACHMENTS

1View. A New Planning System

for NSW - Green Paper Frequently Asked Questions

2View. LGSA Submission to

NSW Planning System Review - Green Paper September 2012

|

Recommendation

That Council note the report and request the General

Manager to arrange a workshop and further report to Council with a view to

making a submission to the White Paper and Exposure Bill.

|

|

Council

|

31

October 2012

|

|

Item 8.2 - Attachment 1

|

A New Planning System for NSW -

Green Paper Frequently Asked Questions

|

2.

|

Council

|

31

October 2012

|

|

Item 8.2 - Attachment 2

|

LGSA Submission to NSW Planning

System Review - Green Paper September 2012

|

staff

reports – economic (enterprising)

31 October

2012

In accordance with Council’s Code of Meeting Practice

(2011), this section of the agenda will be chaired by Councillor Surname.

10.1 National

Broadband Network.......................................................................... 93

Council 31 October 2012 Item

10.1

10.1. National

Broadband Network

This report will provide Council with additional detail

concerning the negotiations between Council and the NBN Co Ltd.

General Manager

Background

The General Manager, in conjunction with RDA, had worked on

a strategy to present the south coast to NBN as ready for broadband rollout,

outlining the economic and social benefits of that infrastructure investment to

the region. That work led to the preparation and recent adoption of the

Council’s Digital Economy Strategy.

Late in 2011, NBN Co Limited announced the next three-year

program for rollout, which excluded the far south coast. The General Manager

held discussions with Cushman Wakefield, the agents for NBN Co Ltd, concerning

potentially suitable sites for the installation of NBN satellite dishes in the

Shire. NBN were seeking a large site in private or public ownership, being one

of two major sites across the country intended to accommodate satellite dishes.

Following a search of a number of properties, NBN identified

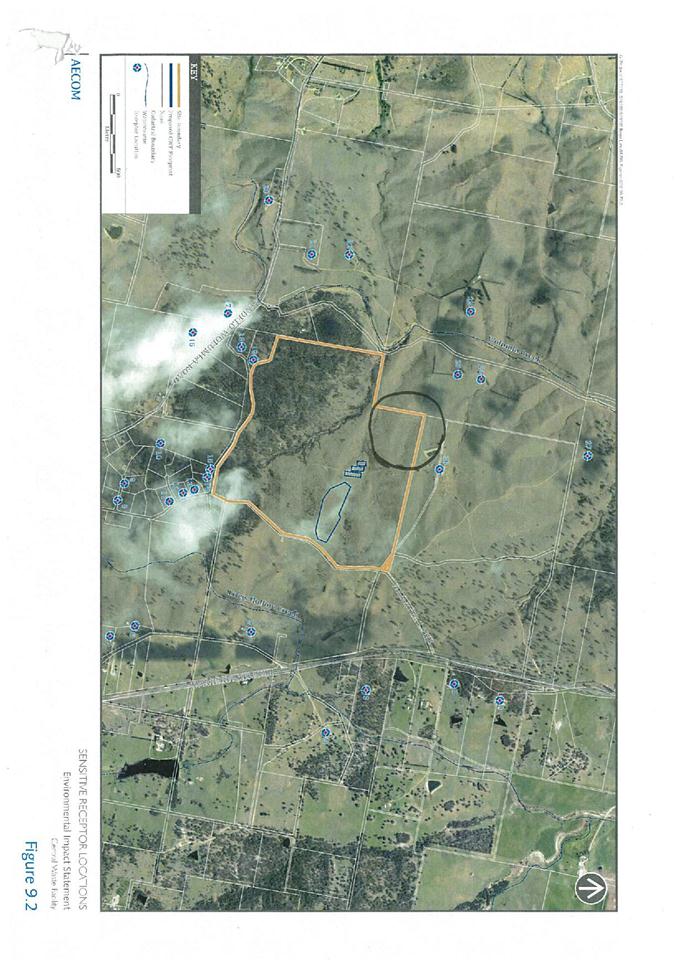

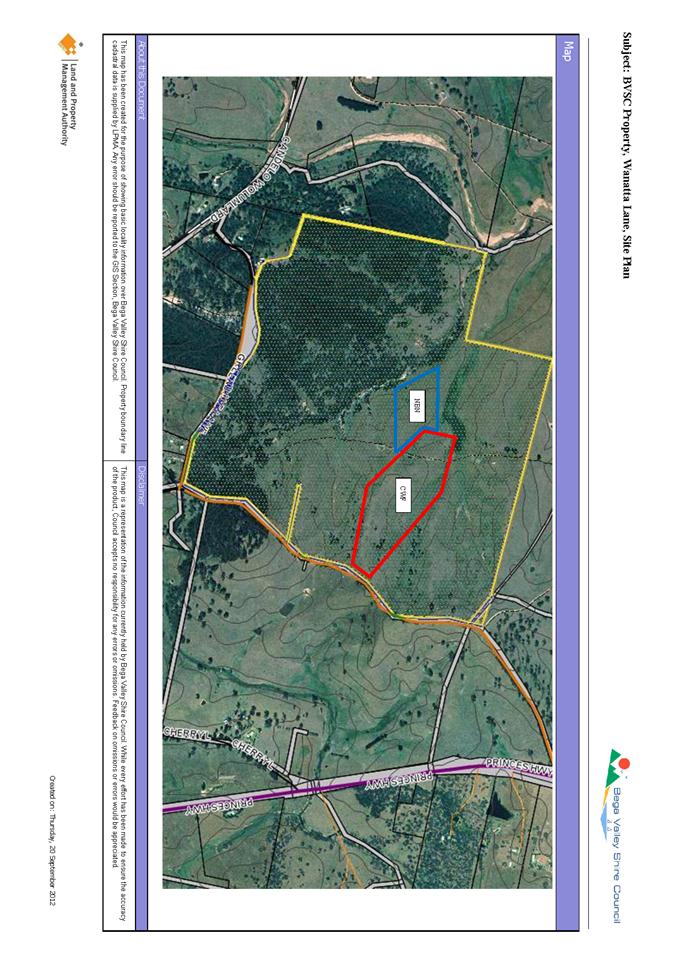

Council’s Wanatta Lane site (Part Lot 3 DP 592206) as ideal geographically and

topographically as an earth satellite tracking station for the purposes of the

National Broadband Network (subject to Development Consent). A copy of that

original site plan is attached (Attachment 1).

Councillors were briefed in confidence of the opportunity to

utilise a Council site, potentially bringing forward high speed satellite

wireless broadband to the Shire and region, in advance of the NBN fibre

rollout. NBN expressed an interest in the site, initially under a lease, with

an option to purchase.

Following subsequent investigations and endorsement by NBN

board, in mid February 2012 Cushman Wakefield submitted a draft heads of

agreement to Council to form a basis for further discussions. The heads of

agreement (HoA) contained in principle terms to identify a suitable 5 ha parcel

on the Wanatta Lane site, nominated initially as a parcel to the NW of the

Central Waste Facility (CWF), for lease with an option to purchase, subject to

the site being subdivided, and the lessee having access for site investigations.

Whilst referred to in discussions as a ‘heads of agreement’, the document

submitted to Council on 13 February 2012 was entitled ‘Offer to lease then

purchase’ and comprised commercial particulars of the proposed transaction, and

suggested general terms and conditions to essentially cover the requirements

for the short term lease whilst the site was subdivided, following which, the

site would be purchased by the NBN Co Ltd.

In late March 2012, the

independent valuation report was received, providing valuations for both the

lease and sale of the site. The Preliminary Engagement Overview prepared by NBN

Co, (Attachment 2) was released in March 2012 and provided additional

information to assist the planning discussions, negotiations and acquisition

process. Legal advice in relation to the draft ‘offer to lease then purchase’

was sought, including provisions regarding sharing access and energy to the

site. A summary of that advice was reported to Council on 10 April 2012.

Council considered the matter

and valuation in closed session on 10 April 2012 and resolved:

1. That Council note the

report and NBN “Preliminary Engagement Overview”.

2. That the General Manager

be authorised to negotiate terms of the lease with NBN, having regard to the

advice from Council’s lawyers and arrange subdivision of Part Lot 3 DP 292206.

3. That the Mayor and

General Manager be delegated authority to execute documents with Council’s

official Seal to be affixed to the Lease Documents/Contract Documents.

4. That a further report be

presented when the option to acquire the site, following subdivision, is

proposed.

Following the resolution of Council, staff commenced

negotiations for the appropriate agreements to give effect to the lease and

sale of the site following subdivision, and to ensure Council access and

operations would not be compromised. NBN also met with Council staff regarding

town planning, environment, CWF conditions, access and energy matters.

A further site visit was conducted in May 2012 by NBN Co and

surveyors, in order to locate the position of the Full Motion Antenna.

Identifying that position would enable the remainder of the site to be

confirmed and surveyed.

Difficulties ensuring the appropriate line of sight to the

horizon ultimately required a change of location within the site. A parcel,

approximately 5 hectares in size and located to the south west of the CWF, was

preferred. The valuer indicated as the area remained the same, no change to

valuation for purchase was required. A site plan is attached (Attachment 3).

As briefed to Councillors, NBN Co pushed to progress the

agreement for the sale of the site following subdivision, with a development

application to be submitted at an early opportunity. The proposed HoA, upon

legal advice, then became an ‘offer to purchase’.

Further legal advice was sought for the appropriate

preliminary agreement to be prepared. The format of the original ‘offer to

lease then purchase’ was used as the basis for negotiations. Significant

negotiation was involved in relation to operational issues relevant to the CWF

and the access road and agreeing on the site plan to be incorporated into the

agreement. This process eventually resulted in agreement to the terms of the

attached ‘offer to purchase’ (Attachment 4).

A holding deposit of $5,000 has been paid by the NBN Co Ltd,

noting a deposit under any contract for sale would be 5% of the purchase price.

ISSUES

Legal

As briefed to Councillors, the Heads of Agreement/Offer to

Purchase was executed in August 2012, and is subject to certain actions before

any contract for sale may be contemplated. Since execution of that agreement,

Council had been prorogued until the local government elections in September.

Whilst the Offer to Purchase does not incorporate a formal

tenancy arrangement for the site, there is provision for NBN Co Ltd to carry

out works on the land prior to completion and includes obligations regarding

indemnities and removal of such works if the contract is rescinded or

terminated.

Further, it is intended that the contract of sale will

contain provisions dealing with the tenancy by NBN Co Ltd. in detail.

Legal advice to Council is that in the absence of a formal lease being entered

into, the access/occupation of the site by NBN Co Ltd would be as a licensee.

Council and NBN Co are currently negotiating the terms of

the contract of sale. A draft is expected to be tabled at the meeting.

Council's solicitors will assist in this process. The status of negotiations is

that a Road Access Agreement in relation to the CWF and NBN sites, is being

drafted to be incorporated into the contract of sale. Finalisation of the

contract is also subject to the draft plan of subdivision which is being

prepared by the surveyors appointed by NBN Co Ltd.

The HoA contained a confidentiality clause.

Asset

The Wanatta Lane property (198 ha) accommodates the approved

(CWF) cells, leachate/stormwater ponds and associated infrastructure

(approximately 10 ha), with stage 1 expected to be constructed by mid-2013. As

emailed to Councillors in September, any DA submitted by NBN will be determined

by JRPP. The claim that the central waste facility EIS/DA restricted the use of

the Wanatta Lane property to the CWF only, may form part of submissions to the

DA considered by JRPP.

Controls to ensure the construction and operation of the CWF

are not compromised by the construction and operation of the NBN installation,

will be contained in the contract of sale and expected to be reinforced as

conditions in any consent by JRPP.

Consultation

While briefings to Councillors in

May signalled the scale of the proposed installation, NBN presented to

Councillors in June 2012, and held community information sessions in Wolumla in

September.

Until this point, the commercial

terms has been dealt with in confidence. It was considered any subsequent

Development Application process would enable community and agency comment based

on the proposed use of the site for the satellite tracking station, and enable

consent conditions to be applied to appropriate protections to avoid compromise

of either parties operations.

Development

Application Process

The development application has been lodged with Council.

As Council is:

· the owner of the land; and

· the proposed development is private infrastructure

with a value over $5m

the proposed development would be classified as Regional

Development under Schedule 4A of the Environmental Planning and Assessment Act

1979.

As a result the Southern Region Joint Regional Planning

Panel (JRPP) would be the consent authority for the development application and

not Council.

As Council is the owner of the land it is proposed that an

independent planning consultant would be engaged to assess any development

application and prepare the report and recommendation for submission to the

JRPP. Council may make a submission to that application.

An Expression of Interest and Brief has been submitted to

consultants and responses are awaited.

Financial

The independent valuation previously provided to Councillors

(Attachment 5) recommended $150,000 to purchase. Legal and survey costs

associated with the subdivision should be borne by NBN.

Conclusion

Following the report to Council in April, the General

Manager facilitated negotiations to enable NBN Co to utilise a 5ha parcel on

the Wanatta Lane site for site investigations to assess planning, access,

infrastructure and antenna suitability, through a heads of agreement. Due to

topographical constraints, the parcel preferred by NBN shifted to the south

west of the CWF. Subject to subdivision, and access road agreement, and based

on an independent valuation of $150,000, it is recommended Council proceed to

sell that parcel to NBN Co, with a contract for sale subject to development

consent and conditioned to protect the CWF and infrastructure assets and

operations on the Wanatta Lane property. Its use as a NBN satellite tracking

station, enabling high speed satellite wireless to the region, is subject to DA

supported by relevant studies, community and agency comment and the

determination of the JRPP.

ATTACHMENTS

1View. Original site

proposed for NBN installation - Wanatta Lane ( March 2012)

2View. Preliminary

Engagement Overview - Satellite Network Deployment Bega Valley Shire Council

3View. National Broadband

Network - Current Site Plan

4View. National

Broadband Network Heads of Agreement - Executed 8/8/12 (Councillor Only)

5View. NBN

installation opteon valuation report executive (Councillor Only)

|

Recommendation

1. That

Council note the report.

2. That

Council enter a contract for sale of Part Lot 3 DP 592206 Wanatta Lane Frogs

Hollow to NBN Co Ltd in consideration of $150,000, subject to:

· the terms outlined in the Offer to

Purchase

· conditions appropriate to protect

the construction and operational interests of the central waste facility

· NBN Co meeting costs of

subdivision and council’s legal costs up to $3000 associated with the sale.

3. That

Council authorise its official seal to be affixed to the necessary documents

under the signature of the Mayor and the General Manager.

|

|

Council

|

31

October 2012

|

|

Item 10.1 - Attachment 1

|

Original site proposed for NBN

installation - Wanatta Lane ( March 2012)

|

|

Council

|

31

October 2012

|

|

Item 10.1 - Attachment 2

|

Preliminary Engagement Overview

- Satellite Network Deployment Bega Valley Shire Council

|

|

Council

|

31

October 2012

|

|

Item 10.1 - Attachment 3

|

National Broadband Network -

Current Site Plan

|

staff

reports – infrastructure Waste and Water (Accessibility)

31 October

2012

In accordance with Council’s Code of Meeting Practice

(2011), this section of the agenda will be chaired by Councillor Surname.

11.1 Bega

Valley Local Traffic Committee Meeting 10 October 2012............. 125

11.2 Water

Allocation Payments to Sportsground Committees........................ 127

11.3 Developer

Charges Guidelines for Water Supply and Sewerage (Consultation Draft) 131

11.4 Tender

26/12 Littleton Gardens Public Toilet.............................................. 207

11.5 Bega

Town Hall Expression of Interest (Stage 2)....................................... 211

Council 31 October 2012 Item

11.1

11.1. Bega

Valley Local Traffic Committee Meeting 10 October 2012

This report recommends that Council adopt the advice of the Bega Valley

Local Traffic Committee meeting held on 10 October 2012.

Group Manager Infrastructure, Waste & Water

Background

The Bega Valley Local Traffic Committee held a meeting on 10

October 2012, the minutes of which have been distributed separately. It is a

requirement that Council formally adopt the recommendations, prior to action

being taken. All recommendations were supported unanimously by the Committee.

ATTACHMENTS

Nil

|

Recommendation

That Council note the advice of the Bega Valley Local

Traffic Committee meeting held on 10 October 2012 and approve the following:

Intersection

of Minyama Parade and Prospect Street, Bega

1 That

the existing Stop sign currently facing traffic entering the Minyama Parade

and Prospect Street intersection from Newtown Road, Bega be retained and an

additional Stop sign be installed facing traffic entering the intersection

from the western leg of Prospect Street.

2 That

this be accompanied by appropriate line marking.

The Snake Track, Kiah - Southern Mountains Rally

1 That,

subject to conditions, The Snake Track between the Princes Highway and

Towamba Road intersections be temporarily closed between 5.30pm to 11.30pm on

Saturday, 3 November 2012 for a competitive stage of the Southern Mountains

Rally.

2 That

the proposed traffic arrangements involving the temporary closure of The

Snake Track for the Southern Mountains Rally on Saturday, 3 November 2012 be

deemed a Class 2 special event and it be conducted under an approved Traffic

Control Plan for night time activities, which is to be provided to Council by

Wednesday, 24 October 2012 and be in accordance with the Roads and Maritime

Services (RMS) Traffic Control Manual.

3 That

persons involved in the preparation and implementation of the Traffic Control

Plan must hold the appropriate RMS accreditation.

4 That

organisers fully implement an approved Special Event Transport Management

Plan.

5 That

organisers have approved public liability insurance of at least $20 million

indemnifying Council, Police and Roads and Maritime Services by name for the

event.

6 That

organisers obtain a Section 40 approval from the Commissioner of Police, or

their delegate, prior to conducting the event.

7 That

local residents be notified of the amended times and evidence of the

notification be provided to Council by Tuesday, 30 October 2012.

|

Council 31 October 2012 Item

11.2

11.2. Water

Allocation Payments to Sportsground Committees

Council currently pays an allowance to sportsground

management committees to subsidise water usage charges, as well as funding for

maintenance. A review of the calculation method, area of sportsgrounds and

procedure of making payments has been now been completed.

Group Manager Infrastructure, Waste & Water

Background

The sportsground committees at George Brown Oval, Pambula

Sports Complex, Berrambool Oval, Lawrence Park and Dickinson Park receive a

maintenance allowance and a water allowance. Both amounts are provided to

assist the committees in the management and upkeep of the respective

sportsgrounds. The committees also receive the generated income at each

facility. The Bega recreation grounds are maintained by Council, and managed

with assistance of the sporting clubs.

Council has previously received a number of reports

regarding water allocations payments to sportsground committees on (27 September

2011, 18 October 2011, 3 July 2012). This review comes at the request of

several sportsground management committees over concerns at the increasing cost

of water usage.

The current approach to water allocations was introduced in

2007 to encourage the efficient use of water, with a view that if more water

than the allowance was used, the difference would be met by the committee. If

underspent, the balance would be allocated to maintenance and upkeep of the

facility at the committees’ discretion.

A formula was introduced using the accepted turf industry

standard minimum amounts for irrigation and the amount of funds allocated to

the specific committees.

Circumstances have changed at the sportsgrounds since the

original payments were made. These include: water access charges no longer

being applied to Council properties (increasing funds available to those

committees for maintenance) , higher than average rainfall, the installation of

irrigation systems, and metering rearrangements to reduce the sewer discharge

factor and charges.

ISSUES

Asset

The process of how each committee has been billed and

reimbursed was reviewed. The outcome is that processes are proposed to be

updated:

· allocations will be made in July,

October, January and April,

· amendments to any increase in the area

of sporting fields made at an annual review.

Further, each sporting complex has been reassessed and the

area for future allocations will be based on the table below.

Opportunities may emerge in the future, to contemplate

reticulating or storing effluent treated to recreation standard from sewer

treatment plants, for irrigation of sporting fields. Capital costs may be

amortised to assign an equivalent value to treated effluent as potable water

initially, recovered initially under a similar water charging regime to the

current arrangements – with the dual benefit of reusing effluent and reducing

the draw on potable water supply.

Social

/ Cultural

Community expectation is that playing surfaces are suitable

and safe for user need. The level of service is to be defined in the Recreation

asset management plan.

Economic

While the cost is considerable, maintaining these sites in

playable condition is more cost-effective than allowing them to deteriorate,

then attempting a restoration. The generosity of volunteers in managing and

maintaining these facilities, using revenues collected for hire of

grounds/facilities, Council’s allocation and any grants, saves Council and the

broader community paying wages or contractors to undertake those activities.

Financial

The annual budget allocation for management of sportsgrounds

is $93,000 in 2012.

The current water allocations are based on the following

formula:

Playing Surface area (size m2)

x 170mm per m2 per annum

Note: the 170mm per m2 per annum is the accepted turf industry standard minimum

amount of irrigation required to supplement rainfall and to keep the turf in

good condition.

Table 1

|

Sporting Oval

|

Average Usage

2008-2012

|

Calculated

Allowance KL/Pa

|

Proposed Water Allocation KL/PA

|

Current Water Allocation (currently

paid)

|

Average Water Bill 2008-2012

|

Proposed equivalent Water

Allocation

KL @$2.25 2012/13

|

|

George Brown Sporting

Complex (Eden)

|

2,292

|

1720

|

1800

|

$4282.00

|

$6,344.57

|

$4,050.00

|

|

Dickinson Park (Bermagui)

|

1627

|

2323

|

2500

|

$2408.00

|

$4,403.94

|

$5,625.00

|

|

Pambula Beach Sporting

Complex

|

3765

|

4303

|

4500

|

$9145.50

|

$17,114.31

|

$10,125.00

|

|

Berrambool Sporting Complex

|

3021

|

3213

|

3500

|

$19298.00

|

$9,377.95

|

$7,875.00

|

|

Lawrence Park

|

5605

|

2278

|

2500

|

$5002.00

|

$13,680.91

|

$5,625.00

|

Note: Bega Rec Ground water usage

2011-2012 is $32,427.00 (paid by Council). The Bega Show Ground (as community

trust) is the only showground to be paid an annual water allocation payment of

$4284.

Any overruns of the water allowance is to be funded through

the sportsground maintenance allocation. Similarly, any underuse enables more

to be spent on maintenance. An assessment of recent annual water accounts has

indicated that while committees have paid accounts up to the annual allowance,

on occasions the maintenance allocation has been overspent in advance of the

water account, leaving higher water accounts being unpaid and causing stress to

committees. In the main, Council has covered those accounts.

Operational

Plan

The differentiation between Bega Rec grounds maintenance and

management from other sportsgrounds, has been a historical and vexed matter.

The Bega town team incorporates its maintenance into work schedules. The advent

of the proposed General Sports and Recreation s355 Management Committee, may

consider appropriate and equitable means of discerning and distributing budget

allocations, with due reference to the asset management plan and the facility

management plans.

Conclusion

It is proposed the assignment of maintenance allocations to

sportsgrounds should be derived from the asset management plan for maintenance

and renewal, while future facility management plans will outline upgrades. In

the interim, the management committee representatives may meet to distribute

budget allocations for upgrades.

A number of factors have previously caused mixed results

with Sportsground Management Committees receiving their water allocation.

However with a fixed formula for water allocation, a review of sporting field

area and review of process, it is anticipated that existing formula will

adequately meet Council’s current allocation/payment for water accounts.

Therefore it is considered appropriate to provide sportsgrounds with a fixed

‘free’ allocation of water up to the volume indicated in the above table, with

water used above this amount being charged to the sportsground committee.

Alternately, Councillors may wish to assign an annual

maintenance allocation and Council meet the water accounts – noting the

‘tension’ of managing water appropriately may be lost. That issue may be

lessened with the opportunity to restricting irrigated use to early

morning/late evenings or in advance of special events, in accord with best

practice water policy.

An investigation in capital and operational options and

costs regarding potential use of treated effluent, may be pursued once

Councillors consider the Merimbula STP effluent reuse study.

ATTACHMENTS

Nil

|

Recommendation

That Councillors determine a preference for identification

and distribution of allowances for maintenance and water for sportsgrounds.

|

Council 31 October 2012 Item

11.3

11.3. Developer

Charges Guidelines for Water Supply and Sewerage (Consultation Draft)

In August 2012 the NSW Office of Water in conjunction with

IPART released In August 2012 the NSW Office of Water in conjunction with IPART

released revised Developer Charges Guidelines for Water Supply, Sewerage and

Stormwater (Consultation Draft) for comment by NSW Local Government Water

Utilities.

This report provides Councillors with a summary of key

elements of the new Guidelines and an update on implementation of revised

Strategic Business Plans and Development Servicing Plans for Water Supply and

Sewerage.

Group Manager Infrastructure, Waste & Water

Background

Developer charges are up-front charges levied to recover

part of the infrastructure costs incurred in servicing new developments or

additions/changes to existing developments. The authority for local government

councils/local water utilities (LWU) to levy developer charges for water supply

and sewerage, derives from Section 64 of the Local Government Act 1993 by means

of reference to Section 306 of the Water Management Act 2000.

Water and Sewerage Developer Charges (also known as

Headworks Charges or Section 64 charges) are regulated by the NSW Office of

Water through Guidelines issued in December 2002. The Guidelines provide a

methodology for calculating the maximum applicable developer charge, and set

out the requirements for the preparation of Development Services Plans (DSP’s).

DSP’s are preceded by preparation of Strategic Business Plans (with associated

asset, demographic and financial models).

DSP’s are the reference documents produced by Councils in

NSW to enable Developer Charges to be levied at a local level.

In 2006 Council adopted the current Development Servicing

Plans (DSP’s) for Water Supply and Sewerage. The DSP’s and their associated

calculations informed the current S64 contributions and replaced a number of

area based interim contribution plans. They also informed the long term

financial plan (LTFP)

The current Section 64 contributions have been levied on the

basis of full cost recovery (user pays) from all developers in accordance with

policy 2.3.1(l).

In 2007 the NSW State Government requested that IPART review

the Developer Guidelines. IPART provided a final report to the then Minister

in late 2007; however the conclusions of the report were not made public by the

Minister.

Council commenced its scheduled review of the DSPs and

associated charges 12 months ago, commissioning consultants to assist the asset

and financial modelling reviews. NSW Office of Water advised Council mid-year

to not continue the review until the new guidelines were issued.

The matter of headworks charges has been the topic of

several questions and notices of motion from councillors, particularly around:

· Application of charges to

council/community facility developments

· Differentiation of portion of capital

works cost between new development, and existing users

· Comparison of headworks charges to

other LWUs (noting Council has recently invested approximately $75 million in

expanded modern sewer systems, requiring recovery of part of that capital cost

over the next 10/20 years)

· Retrospective application of headworks

charges to lots subdivided before adoption of the 2006 DSP

· Differentiated charges between towns,

villages and catchments

· Scale of proposed augmentation works,

having regard to changing demographics, growth patterns, and consumer behaviour

towards sustainability

· Mapping DSP catchments to new LEP urban

boundaries

The Minister for Primary Industries recently advised Council

that she had decided to support all of the recommendations of the 2007 report,

and the report has now been released on the IPART website.

The revised Developer Charges Guidelines for Water Supply,

Sewerage and Stormwater - Consultation Draft, has been released by the Minister

for Primary Industries pursuant to section 306 (3) of the Water Management Act

2000.

The 2012 Developer Charges Guidelines (Consultation Draft)

will update the Water Supply, Sewerage and Stormwater Guidelines, 2002 and

modify them in accordance with the recommendations of the IPART Review Report

available on the NSW Office of Water (NOW) website and IPART website. Links to

the two documents are as follows:

Developer Charges Guidelines for

Water Supply, Sewerage and Stormwater, 2012 – Consultation Draft

IPART Review Report

ISSUES

Legal

In August 2012 a report was submitted to Council to clarify

the applicability of Section 64 contributions to properties in Bega Valley

Shire. A copy of this report is attached since it also details the legal basis

for application of the contributions in NSW by Council local water utilities.

Policy

There are significant financial implications arising from the

policy position that Council ultimately chooses, once the new DSP’s are

adopted. The current policy position is based on a complete cost recovery

approach whereby developers who utilise water and sewer systems pay for all

growth related infrastructure, with no subsidy from the wider community.

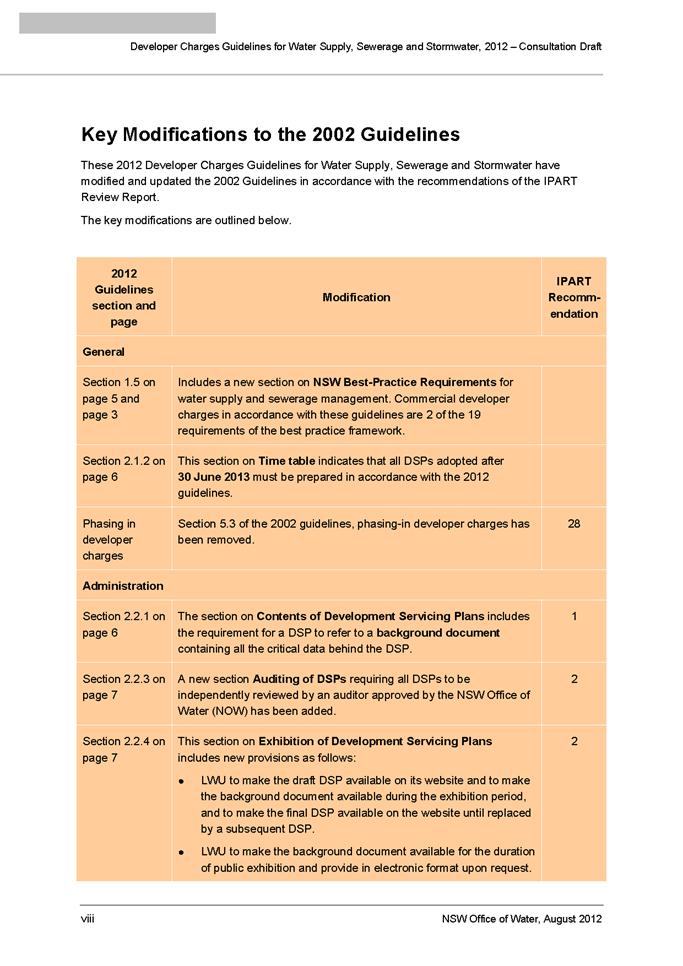

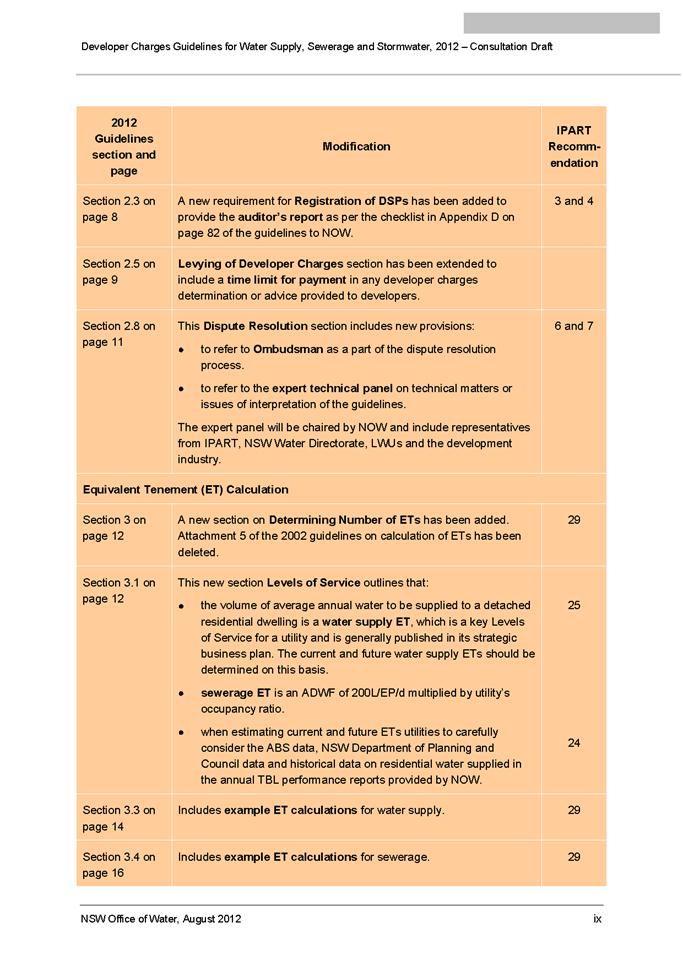

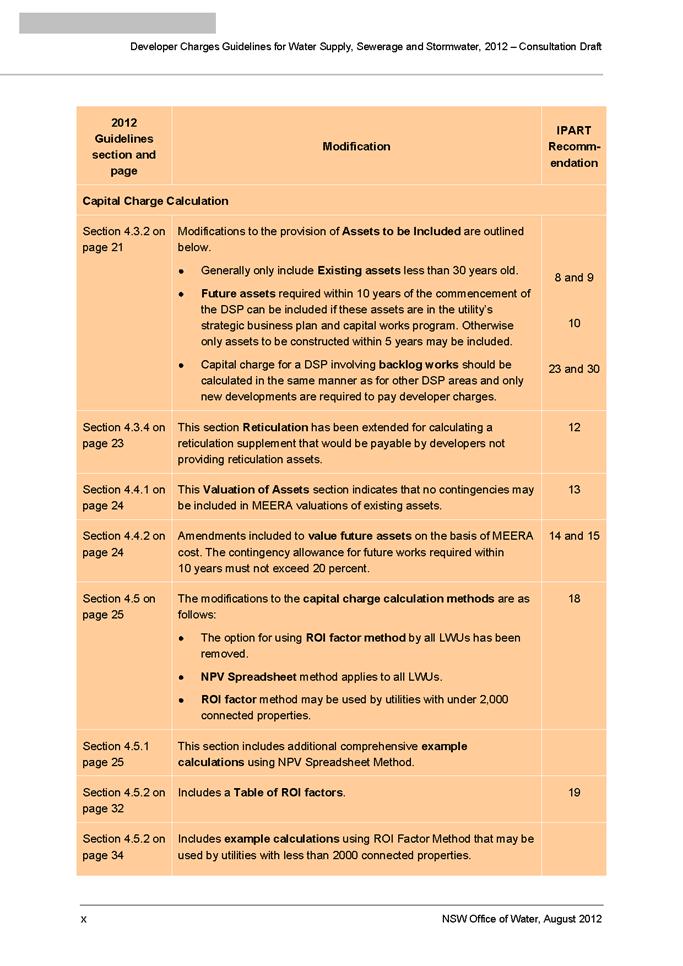

Key

IPART Recommendations

The NSW Office of Water has prepared new guidelines that

incorporate all of the IPART recommendations. There are 30 recommendations and

these are summarised below, together with the potential impacts for Bega Valley

Shire Council.

|

Recommendation

|

General

Comments

|

Impacts

on Bega Valley Shire DSP

|

|

1

Background Information

|

Increased

importance on background documentation, including providing spreadsheet

models

|

Potentially

a little more effort required to prepare background documentation.

|

|

2 Draft

& Final DSPs on BVSC website and review by an independent auditor

|

No real

change.

|

Additional

cost and time associated with having the DSPs audited by an accredited auditor.

|

|

3 & 4

Audit Process

|

DSPs will

now need to be audited prior to being registered with the NSW Office of

Water.

|

Additional

cost and time associated with having the DSPs audited by an accredited

auditor.

|

|

5 CPI

Increase of S64 Charges

|

No change

|

No

impact.

|

|