|

Extraordinary

Meeting Notice and Agenda

An Ordinary Meeting of the Bega Valley Shire Council will be held at Council Chambers, Bega on Wednesday, 26 November 2014 commencing at 11.00

am to consider and resolve on the matters set out in

the attached Agenda.

20

November 2014

|

TO:

Cr Michael Britten, Mayor

Cr Liz Seckold, Deputy Mayor

Cr Tony Allen

Cr Russell Fitzpatrick

Cr Keith Hughes

Cr Ann Mawhinney

Cr Kristy McBain

Cr Liz Seckold

Cr Sharon Tapscott

Cr Bill Taylor

|

COPY:

General Manager, Ms Leanne Barnes

Group Manager Transport and Utilities, Mr Wayne

Sartori

Group Manager Planning and

Environment, Mr Andrew Woodley

Group Manager Community Relations

and Leisure, Mr Anthony Basford

Group Manager Strategy and

Business Services, Mr Lucas Scarpin

Executive Manager

Organisational Development and Governance, Ms Nina Churchward

Minute Secretary

|

|

Publishing Of Agendas And Minutes

The Agendas for Council Meetings

and Council Reports for each meeting are available from 5.00 pm one week prior

to each Ordinary Meeting, on Council’s website. A hard copy is also

made available to each Library Branch and at the Bega Administration Building reception

desk.

The Minutes of Committee and Council

Meetings are available from 5.00pm on Council's Web Site on the Friday after

the Meeting on Councils website and hard copies distributed with the Agenda for

the following meeting.

1. Please

be aware that the recommendations in the Council Meeting Agenda are

recommendations to the Council for consideration. They are not the

resolutions (decisions) of Council.

2. Background

for reports is provided by staff to the General Manager for his presentation to

Council.

3. The

Council may adopt these recommendations, amend the recommendations, determine a

completely different course of action, or it may decline to pursue any course

of action.

4. The

decision of the Council becomes the resolution of the Council, and is recorded

in the Minutes of that meeting.

5. The

Minutes of each Council meeting are published in draft format, and are

confirmed, with amendments by Councillors if necessary, at the next available

Council Meeting.

If you require any further information

or clarification regarding a report to Counci, please contact Council’s

Executive Assistant who can provide you with the appropriate contact details

Phone

(6499 2104) or email execassist@begavalley.nsw.gov.au.

Ethical Decision Making and Conflicts of

Interest

A guiding checklist for Councillors, officers and community committees

Ethical decision making

·

Is the decision or conduct legal?

·

Is it consistent with Government policy, Council’s

objectives and Code of Conduct?

·

What will the outcome be for you, your colleagues, the Council,

anyone else?

·

Does it raise a conflict of interest?

·

Do you stand to gain personally at public expense?

·

Can the decision be justified in terms of public interest?

·

Would it withstand public scrutiny?

Conflict of interest

A conflict of interest is a clash between private interest

and public duty. There are two types of conflict:

·

Pecuniary

– regulated by the Local Government Act and Department of Local

Government

·

Non-pecuniary

– regulated by Codes of Conduct and policy. ICAC,

Ombudsman, Office of Local Government (advice only). If declaring a

Non-Pecuniary Conflict of Interest, Councillors can choose to either disclose

and vote, disclose and not vote or leave the Chamber.

The test for conflict of

interest

·

Is it likely I could be influenced by personal interest in

carrying out my public duty?

·

Would a fair and reasonable person believe I could be so

influenced?

·

Conflict of interest is closely tied to the layperson’s

definition of ‘corruption’ – using public office for private

gain.

·

Important to consider public perceptions of whether you have a

conflict of interest.

Identifying problems

1st Do

I have private interests affected by a matter I am officially involved in?

2nd Is

my official role one of influence or perceived influence over the matter?

3rd Do

my private interests conflict with my official role?

Whilst seeking advice is generally useful, the ultimate

decision rests with the person concerned.

Agency advice

Officers of the following agencies are available during

office hours to discuss the obligations placed on Councillors, officers and

community committee members by various pieces of legislation, regulation and

codes.

|

Contact

|

Phone

|

Email

|

Website

|

|

Bega

Valley Shire Council

|

(02)

6499 2222

|

council@begavalley.nsw.gov.au

|

www.begavalley.nsw.gov.au

|

|

ICAC

|

8281

5999

Toll

Free 1800 463 909

|

icac@icac.nsw.gov.au

|

www.icac.nsw.gov.au

|

|

Office

of Local Government

|

(02)

4428 4100

|

olg@olg.nsw.gov.au

|

http://www.olg.nsw.gov.au/

|

|

NSW

Ombudsman

|

(02)

8286 1000

Toll

Free 1800 451 524

|

nswombo@ombo.nsw.gov.au

|

www.ombo.nsw.gov.au

|

TO: The

General Manager

Bega Valley Shire Council

Disclosure of pecuniary interests / non-pecuniary conflict of interests

In accordance with the

Council’s Code of Meeting Practice and the requirements of the Local

Government Act and regulations or dispensation issued by the Office

of Local Government I hereby disclose the following pecuniary interests

and/or non-pecuniary conflict of interests at the meeting as indicated below:

Ordinary meeting held on _____ / _____ / 20___

dd mm yy

|

Item no

& subject

|

|

|

Interest (tick one)

|

Pecuniary

interest Non-pecuniary

conflict of interest

|

|

* Nature of

interest

|

|

|

If

Non-pecuniary (tick

one)

|

Disclose

& vote Disclose

& not vote Leave

chamber

|

|

|

|

|

|

|

|

Item no

& subject

|

|

|

Interest (tick one)

|

Pecuniary

interest Non-pecuniary

conflict of interest

|

|

* Nature of

interest

|

|

|

If

Non-pecuniary (tick

one)

|

Disclose

& vote Disclose

& not vote Leave

chamber

|

|

|

|

|

|

|

|

Signed

|

|

|

Print Name

|

Councillor

|

* Note: Under the provisions of Section

451(1) of the Local Government Act 1993 (pecuniary interests) and Part

6.11 of the Model Code of Conduct prescribed by the Local Government

(Discipline) Regulation 2004 (conflict of interests) it is necessary for you to

disclose the nature of the interest when making a disclosure of a pecuniary

interest or a non-pecuniary conflict of interest at a meeting.

Agenda

Acknowledgement of Traditional Owners of Bega Valley Shire

I would like to commence by

acknowledging, on behalf of Bega Valley Shire Council the Traditional

Custodians of the lands and waters of the Shire – the people of Yuin

nation and show our respect to elders past and present.

1 Confirmation Of Minutes

Recommendation

That the Minutes of the Ordinary Meeting held on 12 November

2014 as circulated, be taken as read and confirmed.

2 Apologies and requests for leave of

absence

3 Declarations

Pecuniary,

Non-Pecuniary and Political Donation Disclosures to be declared and tabled.

4 Deputations (by prior arrangement)

5 Petitions

6 Mayoral Minutes

7 Adjournment to Standing Committees

Recommendation

That the Ordinary meeting of the

Council be adjourned for the purpose of dealing with staff reports to Standing

Committees.

8 Staff Reports – Planning and

Environment (Sustainability)

In accordance with Council’s Code of Meeting

Practice, this section of the agenda will be chaired by Cr Ftizpatrick.

Nil Reports

9 Staff Reports – Community, Culture

and Leisure (Liveability)

In accordance with Council’s Code of Meeting Practice

, this section of the agenda will be chaired by Cr Tapscott.

Nil Reports

10 Staff Reports

–Economic Development and Business Growth (Enterprising)

In accordance with Council’s Code of Meeting

Practice, this section of the agenda will be chaired by Cr McBain.

Nil Reports

11 Staff Reports – Infrastructure Waste and

Water (Accessibility)

In accordance with Council’s Code of Meeting

Practice, this section of the agenda will be chaired by Cr Taylor.

Nil Reports

12 Staff Reports –

Governance and Strategy (Leading Organisation)

In accordance with Council’s Code of Meeting

Practice, this section of the agenda will be chaired by Cr Mawhinney

12.1 2013

-14 Annual Report for publishing.................................................................................... 10 .

13 Staff Reports – Finance (Leading

Organisation)

In accordance with Council’s Code of Meeting

Practice, this section of the agenda will be chaired by Cr Hughes

13.1 Presentation

of Audited Financial Statements for the year ended 30 June 2014.............. 15

13.2 Quarterly

Budget Review Statement (QBRS) at 30 June 2014................................................ 23

13.3 Quarterly

Review Budget Statement (QBRS) at September 2014........................................ 33.

14 Adoption of Reports from Standing Committees

Recommendation

That all motions recorded in the

Standing Committees, including votes for and against, and acknowledging

declarations of interest already made, be adopted in by the Ordinary Council

meeting.

15 Delegates Reports

16 Rescission/alteration Motions

17 Notices of Motion

18 Urgent Business

19 Questions On Notice

20 Questions for the Next Meeting

21 Items of Interest Relating to Council Business

22 Confidential Business

23 Adoption of reports from Closed Session

24 Resolutions to declassify reports considered in

closed session

Staff Reports – Governance And Strategy (Leading

Organisation)

26 November 2014

In accordance with Council’s Code of Meeting

Practice (2011), this section of the agenda will be chaired by Cr Mawhinney.

12.1 2013

-14 Annual Report for publishing............................................................... 10

|

Council 26 November 2014

|

Item 12.1

|

12.1. 2013 -14 Annual Report for

publishing

Council’s

2013-14 Annual Report is presented for the information of Councillors. The

report is required to be lodged with the Office of Local Government by 30

November 2014

General Manager

Background

Each year Council is required to produce a comprehensive

annual report that provides details on the organisation’s activities and

finances over the period of the previous financial year. The Annual Report is

one of the key points of accountability between Council and our community.

Under the Integrated Planning and Reporting framework, the Annual Report

focuses on Council’s achievements towards the Community Strategic Planning

framework, and also includes some information that is prescribed by the Local

Government (General) Regulation 2005. Council’s Audited

Financial Report and itemised update against the Operational Plan are provided

as attachments to the Annual Report. The NSW Office of Local Government

provides guidelines for the development of the Annual Report and requires a

copy of the report for its records

Issues

Legal

For the purposes of section 428 (4) (b) of the Act, an annual report of a council is to include the

following information:

§ Details (including the purpose) of

overseas visits undertaken during the year by councillors, council staff or

other persons while representing the council (including visits sponsored by

other organisations).

§ Details of the total cost during

the year of the payment of the expenses of, and the provision of facilities to,

councillors in relation to their civic functions (as paid by the council,

reimbursed to the councillor or reconciled with the councillor), including

separate details on the total cost of each of the following:

§ the provision during the year of

dedicated office equipment allocated to councillors on a personal basis, such

as laptop computers, mobile telephones and landline telephones and facsimile

machines installed in councillors’ homes (including equipment and line

rental costs and internet access costs but not including call costs),

§ telephone calls made by

councillors, including calls made from mobile telephones provided by the

council and from landline telephones and facsimile services installed in

councillors’ homes,

§ the attendance of councillors at

conferences and seminars,

§ the training of councillors and the

provision of skill development for councillors,

§ interstate visits undertaken during

the year by councillors while representing the council, including the cost of

transport, the cost of accommodation and other out-of-pocket travelling

expenses,

§ overseas visits undertaken during

the year by councillors while representing the council, including the cost of

transport, the cost of accommodation and other out-of-pocket travelling

expenses,

§ the expenses of any spouse, partner

(whether of the same or the opposite sex) or other person who accompanied a

councillor in the performance of his or her civic functions, being expenses

payable in accordance with the Guidelines for the payment of expenses and the

provision of facilities for Mayors and Councillors for Local Councils in NSW

prepared by the Director-General from time to time,

§ expenses involved in the provision

of care for a child of, or an immediate family member of, a councillor, to

allow the councillor to undertake his or her civic functions.

§ Details of each contract awarded by

the council during that year (whether as a result of tender or otherwise) other

than:

§ employment contracts (that is,

contracts of service but not contracts for services), and

§ contracts for less than $150,000 or

such other amount as may be prescribed by the regulations, including the name

of the contractor, the nature of the goods or services supplied by the

contractor and the total amount payable to the contractor under the contract.

§ A summary of the amounts incurred

by the council during the year in relation to legal proceedings taken by or

against the council (including amounts, costs and expenses paid or received by

way of out of court settlements, other than those the terms of which are not to

be disclosed) and a summary of the state of progress of each legal proceeding

and (if it has been finalised) the result.

§ Details or a summary (as required

by section 67 (3) of the Act) of resolutions

made during that year under section 67 of the Act concerning work

carried out on private land and details or a summary of such work if the cost

of the work has been fully or partly subsidised by the council, together with a

statement of the total amount by which the council has subsidised any such work

during that year.

§ The total amount contributed or

otherwise granted under section 356 of the Act.

§ A statement of all external bodies

that during that year exercised functions delegated by the council,

§ A statement of all corporations,

partnerships, trusts, joint ventures, syndicates or other bodies (whether or

not incorporated) in which the council (whether alone or in conjunction with

other councils) held a controlling interest during that year,

§ A statement of all corporations,

partnerships, trusts, joint ventures, syndicates or other bodies (whether or

not incorporated) in which the council participated during that year,

§ A statement of the activities

undertaken by the council during that year to implement its equal employment

opportunity management plan.

§ A statement of the total

remuneration comprised in the remuneration package of the general manager

during the year that is to include the total of the following:

§ the total value of the salary

component of the package,

§ the total amount of any bonus

payments, performance payments or other payments made to the general manager

that do not form part of the salary component of the general manager,

§ the total amount payable by the

council by way of the employer’s contribution or salary sacrifice to any

superannuation scheme to which the general manager may be a contributor,

§ the total value of any non-cash

benefits for which the general manager may elect under the package,

§ the total amount payable by the

council by way of fringe benefits tax for any such non-cash benefits.

§ A statement of the total

remuneration comprised in the remuneration packages of all senior staff members

(other than the general manager) employed during the year, expressed as the

total remuneration of all the senior staff members concerned (not of the

individual senior staff members) and including totals of each of the following:

§ the total of the values of the

salary components of their packages,

§ the total amount of any bonus

payments, performance payments or other payments made to them that do not form

part of the salary components of their packages,

§ the total amount payable by the

council by way of the employer’s contribution or salary sacrifice to any

superannuation scheme to which any of them may be a contributor,

§ the total value of any non-cash

benefits for which any of them may elect under the package,

§ the total amount payable by the

council by way of fringe benefits tax for any such non-cash benefits.

§ If the council has levied an annual

charge for stormwater management services-a statement detailing the stormwater

management services provided by the council during that year,

§ If the council has levied an annual

charge for coastal protection services-a statement detailing the coastal

protection services provided by the council during that year,

§ A detailed statement, prepared in

accordance with such guidelines as may be issued by the Director-General from

time to time, of the council’s activities during the year in relation to

enforcing, and ensuring compliance with, the provisions of the Companion Animals Act 1998 and the regulations

under that Act.

Resources (including staff)

Development, design and printing of 2013-14 Annual

Report has utilised in house resources only.

Conclusion

2013-14 Annual Report has been prepared to comply with

the legislative requirements and to overview the achievements against the

2013-14 operational plan. The annual report is to be provided to the Office of

the Local Government by 30 November 2014. It will also be published on the

Council’s website.

Attachments

Nil

Recommendation

That the 2013-14 Annual Report be

endorsed for publishing on Council website, provision of hard copies to

library branches and lodged with the Office of Local Government.

|

Staff Reports – Finance (Leading Organisation)

26 November 2014

In accordance with Council’s Code of Meeting

Practice (2011), this section of the agenda will be chaired by Cr Hughes.

13.1 Presentation

of Audited Financial Statements for the year ended 30 June 2014 15

13.2 Quarterly

Budget Review Statement (QBRS) at 30 June 2014........................... 23

13.3 Quarterly

Review Budget Statement (QBRS) at September 2014...................... 33

|

Council 26 November 2014

|

Item 13.1

|

13.1. Presentation of Audited Financial Statements for the year ended

30 June 2014

This report presents the

draft financial statements to Council to be confirmed by the presentation of

the audited financial statements to Council on 26th November 2014.

Group Manager Strategy and Business

Services

Issues

Financial

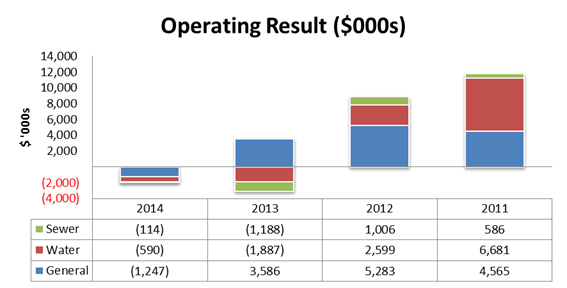

Council has achieved an operating result

of ($1,951k) across all Funds (General, Water, and Sewer).

|

Fund

|

2014

|

2013

|

%

|

|

General

|

-$1,247

|

$3,586

|

-135%

|

|

Water

|

-$590

|

-$1,887

|

-69%

|

|

Sewer

|

-$114

|

-$1,188

|

-90%

|

|

Total

|

-$1,951

|

$511

|

-482%

|

This

operating deficit is attributable to the return of Financial Assistance Grant

(‘FAG’) to annual payment. This reversion consequently decreased

the FAG revenue by $3,238k compared to last financial year. To be clear, the

result is an operating deficit, not a cash deficit. Cash position of Council is

sound as the prior year extra instalments were held in internal restriction and

have now decreased to nil.

There

was advance payment of FAG for $3.454M that was recognised as revenue in the

prior year. Had this amount been recognised as revenue in 2014 FY, the result

would have been a surplus of $1.503M.

Operating

Revenues:

Council’s operating revenues have decreased by

9% in 2014. Council had forecast a reduction in operating revenues in its

budget and this decrease was less than expected. The decrease can be largely

attributed to the Operating Grants and Contributions. The main contributors

being FAG and other grants associated with flood restoration works. Council is

forecasting a general reduction in operating and capital grants over the short

to midterm with the change in Government and the longer term effects of the

Global Financial Crisis.

Council’s revenues detailed as follows:

|

Item

|

2014

|

2013

|

$ Mvmt

|

%

|

|

Rates & Annual

Charges

|

$43,310

|

$41,281

|

$2,029

|

5%

|

|

Operating Grants &

Contributions

|

$11,026

|

$23,289

|

-$12,263

|

-53%

|

|

User Charges

|

$14,213

|

$12,111

|

$2,102

|

17%

|

|

Investment Returns

|

$2,318

|

$2,665

|

-$347

|

-13%

|

|

Sale of Assets &

Other

|

$739

|

$644

|

$95

|

15%

|

|

Capital Grants

|

$4,550

|

$3,627

|

$923

|

25%

|

|

|

$76,156

|

$83,617

|

-$7,461

|

-9%

|

Operating

Expenditure:

Operating Expenses decreased by 6% in

the 2014 financial year.

The major contributor to the decrease is

completion of flood restoration works.

Balance

Sheet:

Overall Council saw an improvement to

its balance sheet of $7.7M. This was mainly attributable to net increase in

Infrastructure, Property, Plant and Equipment of $16.3M with a decrease in Cash

and Cash Equivalents of $6M

There were no asset revaluations in

2014.

Financial

Ratios:

Council is required to report the following ratios to

the Office of Local Government:

Operating Performance Ratio | Benchmark > 0%

This ratio measures Council’s

achievement of containing operating expenditure within operating revenue.

Councils Operating Performance Ratio

has been severely impacted in 2014 due to the Federal Government not advancing

the Financial Assistance Grant in 2014. This has reduced councils operating

revenue.

Own Source Operating Revenue Ratio | Benchmark > 60%

This ratio measures fiscal flexibility.

It is the degree of reliance on external funding sources such as operating

grants & contributions.

Council is well above the benchmark

for own source revenue. The 2014 result was improved by the lower reported

Financial Assistance Grant revenue in 2014. An integral part of Council’s

adopted Long Term Financial Plan is to attempt to increase own source revenues.

Unfortunately as the State and Federal Government reduce the number and value

of grants available to Local Government this ratio starts to show Councils

having to rely on own source revenue to fund their works programs.

Unrestricted

Current Ratio | Benchmark >1.5X

The ratio measures the adequacy of

working capital and its ability to satisfy obligations in the short term for

the unrestricted activities of Council.

Council is well above the industry

benchmark of 1.5 X. This indicates a strong capacity to pay its debts as and

when they fall due. The decline in the ratio is direct result of Councils

strategic planning and the work put into the reduction of Councils

infrastructure backlog over time. We anticipate this ratio continuing to

decline as reserves are drawn down to fund capital works programs.

Debt

Service Cover Ratio | Benchmark > 2.0X

The ratio measures the availability of

operating cash to service debt including interest, principal and lease

payments.

Council's debt service ratio is in

strong position. Council has sufficient fund to meet its debt obligation.

Council holds approximately $35.7M in debt across all three funds. Councils

Long Term Financial Plan outlines that Council will see draw down more debt to

enable Council to reduce infrastructure backlog and construct some community

priority projects while still remaining below the benchmark.

Rates,

Annual Charges, Interest & Extra Charges Outstanding Percentage | Benchmark

< 5%

This ratio assesses the impact of

uncollected rates and annual charges on Council’s liquidity and the

adequacy of recovery efforts.

Outstanding Rates, Charges and fees

are 4.14% which is within industry benchmark of 5%. Council has strong debt

collection procedures in place to collect its rates and charges.

Council has managed to maintain an

outstanding collection percentage close to the Office of Local Government

benchmark for a number of years now. It is critical that Council keep this

ratio as low as possible to aid with Councils cash flow. For example, allowing

this ratio to increase by 1% will result in more than $500,000 that Council

will not collect and by extension would not be able to utilise to resource

works in the community. This could either lead to the work not being performed

or alternate funding arrangement being made, such as borrowings, increased

fees, etc. It is worth noting that Council has seen its recovery costs increase

from approximately $40,000 in 2009 to approximately $290,000 in 2014. These

costs are passed onto the ratepayers that Councils has had to instigate

collection on. No costs are passed onto the general rate base.

Cash

Expense Cover Ratio

This liquidity ratio indicates the

number of months a council can continue paying for its immediate expenses

without additional cash inflow.

Council again has a very strong liquidity ratio and is

well above the benchmark.

Services:

While the financial statements

provide a high level view of Council as an entity, it is worth noting that

while a large portion of Councils finances go to maintain the infrastructure

that we use on a daily basis, there is a significant portion of Councils

revenues that provide many services back to the community such as:

§ $9.6M

on Environmental Management projects.

§ $4.9M

on Community Support projects.

§ $1.6M

on Economic Development projects.

Out of total expense of $100M

(including capital), $26M was spent in maintenance and operation of community

assets, $31M in capital projects, $5M in repayment of borrowings and $38M in

provision of services to community.

The chart below illustrates 2015 operating expenditure

$ per function with comparative.

Council’s financial results for

the 2014 financial year are indicative of the approach Council has taken over

the past few years. The adoption of the Community Strategic Plan, the Asset

Management Plans, and the Long Term Financial Plan has allowed Council to set

out a pathway for the short to mid-term horizon. The results as reported for

2014 illustrate that Council is progressing well. All indicators are

satisfactory and Councils finances remain in a healthy position.

Council has also undergone several internal

and external audits during the 2014 financial year. All of these reviews have

indicated Council is in a stable and sound financial position.

Click here to view the Financial

Statements for the year ended 30 June 2014

Attachments

Nil

|

Recommendation

1. That Council accept the Auditors

presentation and report provided to Council on November 26, 2014 relating to

the audited Financial Statements of Bega Valley Shire Council for the 2014

financial year.

2. That Council

note the contents of the Financial Statements for the 2014 financial year.

|

|

Council 26 November 2014

|

Item 13.2

|

13.2. Quarterly

Budget Review Statement (QBRS) at 30 June 2014

Budget review statements are

prepared and presented to Council quarterly in accordance with Section 203 of

the Local Government (General) Regulations 2005.

Group Manager Strategy and Business

Services

Background

Under the Integrated Planning and

Reporting (IPR) guidelines, it is not mandatory to present a Quarterly Budget

Review Statement (QBRS) for the June quarter. However, it is considered a QBRS

offers more detailed and direct information that can assist the community in

understanding Councils financial position. The QBRS will be published on

Councils website for the community once adopted:

Click here to access the Quarterly

Review Budget Statement

Issues

Strategic

In order to make it clearer for

Councillors and the public, the following graphic depicts the flow of financial

information in any given financial year and how the various financial documents

interact.

This chart illustrates that:

1. The

financial statements are true audited records for the financial year. These

results are used to “reset” the Long Term Financial plan (LTFP).

2. The

“reset” LTFP plan is then remapped with moving works schedules and

is confirmed to still be in a sustainable position. The LTFP is presented to

Councillors at this time for adoption. At this time Councillors can request

changes in direction of staff. The LTFP is adopted in January/February.

3. The

adopted LTFP plan then is expanded into the relevant years’ operating

budget. It is adopted by Council in March/April.

4. The

Quarterly Budget Review Statement process occurs throughout the financial year at

the end of each quarter. Variances are noted and adopted by Councils.

5. The

cycle then draws to a close as the financial year figures are closed, audited

and presented to Council

6. Then

cycle starts again…

Each stage feeds information into

the next until we have a very tight strategic finance frame work. There are a

range of other statutory documents that Council adopts each year, this diagram

only reflects the financial documents.

Legal

Clause 203 of the Local Government (General)

Regulations 2005 states:

Budget review statements and revision of estimates

1. Not

later than 2 months after the end of each quarter (except the June quarter),

the responsible accounting officer of a council must prepare and submit to the

council a budget review statement that shows, by reference to the estimate of

income and expenditure set out in the statement of the council’s revenue

policy included in the operational plan for the relevant year, a revised

estimate of the income and expenditure for that year.

2. A

budget review statement must include or be accompanied by:

a) A

report as to whether or not the responsible accounting officer believes that

the statement indicates that the financial position of the council is

satisfactory, having regard to the original estimate of income and expenditure,

and

b) If that

position is unsatisfactory, recommendations for remedial action.

c) A

budget review statement must also include any information required by the Code

to be included in such a statement.

Financial

As noted above, a June QBRS is not

mandatory, most of the information is already prepared and presented within

Council’s annual financial statements. As such, this report does not

contain information that is reported within the financial statements, but instead

focuses on the non-operating items that are not covered in the Financial

Statement.

Council’s budget result for the

2014 financial year is positive. While there are specific issues that need to

be addressed which will be covered in more detail below, the overall picture

for Council is positive.

§ Council’s achieved $1.98M less in operating

revenue compared to original budget. This is good result considering Financial

Assistance Grant (‘FAG’) revenue decreased by $3.24M. If FAG was

taken out of the equation, it would mean Council’s operating revenue

increased by $1.26M.

§ Council expended $712K more in operating costs than it

predicted at the start of the financial year (excluding depreciation and other

non-cash expenses). Most of which can be attributable to prior period revotes

of $3.3M out of which $2.2M was fully spent.

§ Operating grants compared to original budget was less

by $3.19M which is mainly attributable to decrease in FAG revenue, while

capital grants received were $435K more than predicted.

§ There was a net reduction of $5.6M in the reserves

which compares to $6.1M in the original budget. Major reserve movements were:

§ FAG Advance Payment – $3,454K

§ Waste Management – $1,754K

§ Plant Replacement – $926K

§ Infrastructure Replacement – $905K

§ Property Development (Eden Port & Littleton

Gardens) – $903K

§ Airport – $531K

§ There was a 8% ($2.065M) increase in employment cost

which can be attributable to

§ Take-up of Sapphire Aquatic Centre with employment

cost of around $700K

§ Overtime cost of $865K ($700K in Operating | 165K in

Capital) *noting that in cash terms these costs were incorporated into the

works budgets for the particular projects affected.

§ Rollout of Cadets and Trainee program of worth around

$500K

Council still holds a healthy working capital balance.

The table below shows the working capital balances for each of Councils funds

at the 30th June 2014.

|

General Fund

|

$4.13M

|

|

Water Fund

|

$2.37M

|

|

Sewer Fund

|

$2.51M

|

|

Total

|

$9.01M

|

Council’s

restrictions (reserves) totalled $51.8M at the conclusion of the 2014 financial

year. The following chart illustrates the current value of Councils

restrictions. Councils LTFP outline how those restrictions will be utilised

over time.

Operationally Council performed

reasonably well in its individual functions. Council’s operating budget

is broken into functions which are managed by Council staff. Council has 23

designated functions across its five community strategic plan themes. Of those

23, 19 were deemed to have performed better than budgeted. The remaining four

were deemed to have performed less than expected. Council’s senior

management has met on these functions to discuss why the results have occurred

and more importantly how to avoid them happening into the future.

The following charts Councils budget performance

against actuals over the course of the financial year.

The following charts show the Council functions and

their performance. The functions marked red have explanations included in this

report for Councils consideration.

Community

Relations and Leisure

|

Function

outside of budget

|

Reason

|

|

Leisure

|

Leisure

includes service areas of Swimming Pools, Sportsgrounds, Park and Beaches.

The

issue in this function relating to Sportsgrounds were overruns in Maintenance

and Operations of $200K as well as non-completion of planned capital projects

at the same time take-up of unplanned capital projects.

Issues

relating to swimming pools were over-estimation of fees by $300K and

unbudgeted operational costs of around $300K in order to have the 6 pools

made ready for opening.

There

were similar overrun issues in parks with Maintenance and Operations being

overestimated budget by $150K.

The reason of these overrun can be

attributed to a lack of robust AMP and LTFP funding applied. These issues

will be rectified in future years with the revised plans and resourcing

strategy.

|

Planning

and Environment

Strategy

and Business Services

|

Function outside of budget

|

Reason

|

|

Strategy and Business Services

|

Strategy and

Business Services includes the General Purpose funding for Council that

includes the Rates Revenue and Untied Grants. The budgeted revenue for FAG

was not met; this was due to FAG reverting to annual payments in 2014

financial year.

This did not

result in a cash deficit. Cash position of Council is sound as the prior year

extra instalments were held in internal restriction and have now decreased to

nil.

|

Transport

and Utilities

|

Function outside of budget

|

Reason

|

|

Transport Services

|

Service areas under Transport

Services are Roads and Bridges.

There were overruns in capital

expenses for Bridges to a value of $170K. This was largely due to the

heritage works undertaken on Beauty Point Bridge.

Whereas for Roads, maintenance

expenses was $200K over the budgeted value.

|

|

Emergency Services

|

The overrun in Emergency Services

is in relation to council related Hazard Reduction works which was unbudgeted

by $80K.

In addition, there was also

recognition of loss in regards to donated asset to SES of a value of around

$65K.

|

Organisation

Development and Governance

Council has limited revotes for the 2014

financial year. Rather than revoting the works from one year to the next, under

the Long Term Financial planning framework Council has begun adopted, we place

the funds back into reserve and we reset the AMP and LTFP to account for the

unfinished work. This then results in the reserves being called upon to fund

that work in the relevant year that the job is scheduled for.

The only amounts revoted relate to

Unspent Grants and Council Contribution towards those projects. The total

amount

|

Project

|

Cost - $

|

|

Bus Shelters

|

109K

|

|

Community Programs

|

193K

|

|

Cycleways

|

34K

|

|

Environmental Management

|

416K

|

|

Health

|

12K

|

|

Library

|

308K

|

|

LPMA Crown Projects

|

123K

|

|

Planning

|

63K

|

|

Sports

|

50K

|

|

Weeds

|

29K

|

Conclusion

Council’s 2014 end of year

position has concluded favourably compared to budget. All surplus funds have

been moved to Council’s reserves. All revoted projects have been noted

and will be tracked through the 2014 financial year QBRS reports.

In order to maintain a sound financial

performance for future years, we need to put processes in place to rectify

issues identified in this report. Some of the proposed action items are:

§ Procedures around budgeting and monitoring of

employment costs including subsidiary budgeting and tracking against actuals

quarterly along with mechanism to report on overtimes.

§ Refining of Asset Management Plans (AMPs) and having

processes in place to report on its progress.

Attachments

Nil

|

Recommendation

1. That

the Quarterly Budget Review Statement (QBRS) for June 2014 be adopted and the

votes adjusted by those values as reported in the variance column

2. That

Council adopt the Reserve schedule for 2014. Council note that the updated

reserve balances will be incorporated into the September QBRS due to Council

in November.

3. That

Council adopt the Revote schedule for 2014. Council note that the updated

revotes will be incorporated into the September QBRS also reported to this

meeting.

|

|

Council 26 November 2014

|

Item 13.3

|

13.3. Quarterly

Review Budget Statement (QBRS) at September 2014

Budget review

statements are prepared and presented to Council quarterly in

accordance with Section

203 of the Local Government (General) Regulations 2005.

Group Manager Strategy and Business

Services

Background

Under the Integrated Planning and Reporting (IPR)

guidelines, a quarterly budget review statement (QBRS) must be presented to

Council for each financial quarter.

The QBRS, due to its size has been distributed to

Councillors electronically and if requested, in hardcopy. The electronic

version has been placed on Councils website for public access at:

Click here to view the Quarterly

Budget Review Statement for September 2014

The QBRS is presented in a summary format which

reflects the Long Term Financial Plan. Each function of Council is presented

individually as is a summary page for each theme. The report also shows a range

of management information for each Function, such as:

§ Income Progress graphs: These graphs illustrate how

each function is progressing with their revenue estimates. The overall graph

illustrates the cumulative progress of the function, while the monthly graph

shows progress month by month.

§ Reserves table: This table outlines cash reserves that

are linked to that particular function and their movements throughout the

financial year.

§ Expense Progress Graphs: These graphs illustrate how

each function is progressing with their expenditure estimates. The overall

graph illustrates the cumulative progress of the function, while the monthly

graph shows progress month by month.

§ Revotes Table: This table tracks the progress of the

revotes from the 2014 financial year.

It is the intent of this report to provide information

to the users of the QBRS report in order to illustrate the financial

performance of each particular function of Council.

Council staff retain the ability to enquire, transact,

and report on the detailed General Ledger, which includes budgets. If there are

specific questions relating to detailed transactional information, staff can

provide answers to those questions.

Issues

Legal

Clause 203 of the Local Government (General)

Regulations 2005 states:

Budget review statements and revision of estimates

1. Not later than 2 months after the

end of each quarter (except the June quarter), the responsible accounting

officer of a council must prepare and submit to the council a budget review

statement that shows, by reference to the estimate of income and expenditure

set out in the statement of the council’s revenue policy included in the

operational plan for the relevant year, a revised estimate of the income and

expenditure for that year.

2. A budget review statement must

include or be accompanied by:

a. A

report as to whether or not the responsible accounting officer believes that

the statement indicates that the financial position of the council is

satisfactory, having regard to the original estimate of income and expenditure,

and

b. If

that position is unsatisfactory, recommendations for remedial action.

c. A

budget review statement must also include any information required by the Code

to be included in such a statement.

Financial

The QBRS reports the detailed variances for the

September 2014 quarter. The September QBRS generally only includes the revotes

from the preceding year as variances. Revotes are those works committed to in

the preceding year that were not completed. The works are shifted into the current

year with an increase in the relevant expenditure lines and a corresponding

increase in funding from the preceding year.

The value of revotes brought forward from the 2014

financial year equal $1.4M. There are a number of other commitments transferred

from reserves, but the net impact is nil. These transfers relate to unspent

grants and related commitments from 2014 being brought forward into 2015.

There are no major or significant variances to report

to Council. A more detailed analysis is located within the QBRS attachment.

A number of variances relate to Council undertaking an

organisational restructure which commenced on July 1, 2014. These movements

relate to functions moving among groups. Not net impacts have occurred.

As at the end of September 2014, Council held $59M in cash and investments

– the bulk of which remain restricted for use with planned infrastructure

or projects preconditioned by loans, grants or development contributions.

As per Council’s policy, the QBRS reflects the

budget in a balanced position and maintains working capital at adopted levels.

All net movements are factored through the movement to and from reserves,

including anticipated transfers to asset, ELE and property reserves at year

end.

Conclusion

Council’s September 2014 QBRS has been presented

to Council. Council financial performance is healthy and within the operating

budget set by Council in June 2014.

Attachments

Nil

|

Recommendation

1. That

Council note and endorse the September 2014 Quarterly Budget Review Statement.

2. That

Council adopt the variances, in this instance being revotes from the 2014

financial year, to its operating budget as outlined in the QBRS.

3. That

Council place the QBRS for September 2014 on its website for public

information.

|