|

OrdinaryMeeting Notice and Agenda

An Ordinary Meeting of the Bega Valley Shire Council will be held remotely via Zoom on

|

|

OrdinaryMeeting Notice and Agenda

An Ordinary Meeting of the Bega Valley Shire Council will be held remotely via Zoom on

|

Council meetings are recorded and live streamed to the Internet for public viewing. By entering the Chambers during an open session of Council, you consent to your attendance and participation being recorded.

The recording will be archived and made available on Council’s website www.begavalley.nsw.gov.au. All care is taken to maintain your privacy; however as a visitor of the public gallery, your presence may be recorded.

The Agendas for Council Meetings and Council Reports for each meeting will be available to the public on Council’s website as close as possible to 5.00 pm on the Thursday prior to each Ordinary Meeting. A hard copy is also made available at the Bega Administration Building reception desk and on the day of the meeting, in the Council Chambers.

The Minutes of Council Meetings are available on Council's Website as close as possible to 5.00 pm on the Monday after the Meeting.

1. Please be aware that the recommendations in the Council Meeting Agenda are recommendations to the Council for consideration. They are not the resolutions (decisions) of Council.

2. Background for reports is provided by staff to the General Manager for presentation to Council.

3. The Council may adopt these recommendations, amend the recommendations, determine a completely different course of action, or it may decline to pursue any course of action.

4. The decision of the Council becomes the resolution of the Council, and is recorded in the Minutes of that meeting.

5. The Minutes of each Council meeting are published in draft format, and are confirmed by Councillors, with amendments if necessary, at the next available Council Meeting.

If you require any further information or clarification regarding a report to Counci, please contact Council’s Executive Assistant who can provide you with the appropriate contact details

Phone (6499 2104) or email execassist@begavalley.nsw.gov.au.

· Is the decision or conduct legal?

· Is it consistent with Government policy, Council’s objectives and Code of Conduct?

· What will the outcome be for you, your colleagues, the Council, anyone else?

· Does it raise a conflict of interest?

· Do you stand to gain personally at public expense?

· Can the decision be justified in terms of public interest?

· Would it withstand public scrutiny?

A conflict of interest is a clash between private interest and public duty. There are two types of conflict:

· Pecuniary – regulated by the Local Government Act 1993 and Office of Local Government

· Non-pecuniary – regulated by Codes of Conduct and policy. ICAC, Ombudsman, Office of Local Government (advice only). If declaring a Non-Pecuniary Conflict of Interest, Councillors can choose to either disclose and vote, disclose and not vote or leave the Chamber.

· Is it likely I could be influenced by personal interest in carrying out my public duty?

· Would a fair and reasonable person believe I could be so influenced?

· Conflict of interest is closely tied to the layperson’s definition of ‘corruption’ – using public office for private gain.

· Important to consider public perceptions of whether you have a conflict of interest.

1st Do I have private interests affected by a matter I am officially involved in?

2nd Is my official role one of influence or perceived influence over the matter?

3rd Do my private interests conflict with my official role?

For more detailed definitions refer to Sections 442, 448 and 459 or the Local Government Act 1993 and Bega Valley Shire Council (and Model) Code of Conduct, Part 4 – conflictions of interest.

Whilst seeking advice is generally useful, the ultimate decision rests with the person concerned.Officers of the following agencies are available during office hours to discuss the obligations placed on Councillors, officers and community committee members by various pieces of legislation, regulation and codes.

|

Contact |

Phone |

|

Website |

|

Bega Valley Shire Council |

(02) 6499 2222 |

council@begavalley.nsw.gov.au |

www.begavalley.nsw.gov.au |

|

ICAC |

8281 5999 Toll Free 1800 463 909 |

icac@icac.nsw.gov.au |

www.icac.nsw.gov.au |

|

Office of Local Government |

(02) 4428 4100 |

olg@olg.nsw.gov.au |

http://www.olg.nsw.gov.au/ |

|

NSW Ombudsman |

(02) 8286 1000 Toll Free 1800 451 524 |

nswombo@ombo.nsw.gov.au |

Under the provisions of Section 451(1) of the Local Government Act 1993 (pecuniary interests) and Part 4 of the Model Code of Conduct prescribed by the Local Government (Discipline) Regulation (conflict of interests) it is necessary for you to disclose the nature of the interest when making a disclosure of a pecuniary interest or a non-pecuniary conflict of interest at a meeting.

The following form should be completed and handed to the General Manager as soon as practible once the interest is identified. Declarations are made at Item 3 of the Agenda: Declarations - Pecuniary, Non-Pecuniary and Political Donation Disclosures, and prior to each Item being discussed:

Council meeting held on __________(day) / ___________(month) /____________(year)

|

Item no & subject |

|

|

Pecuniary Interest

|

In my opinion, my interest is pecuniary and I am therefore required to take the action specified in section 451(2) of the Local Government Act 1993 and or any other action required by the Chief Executive Officer. |

|

Significant Non-pecuniary conflict of interest |

– In my opinion, my interest is non-pecuniary but significant. I am unable to remove the source of conflict. I am therefore required to treat the interest as if it were pecuniary and take the action specified in section 451(2) of the Local Government Act 1993. |

|

Non-pecuniary conflict of interest |

In my opinion, my interest is non-pecuniary and less than significant. I therefore make this declaration as I am required to do pursuant to clause 5.11 of Council’s Code of Conduct. However, I intend to continue to be involved with the matter. |

|

Nature of interest |

Be specific and include information such as : · The names of any person or organization with which you have a relationship · The nature of your relationship with the person or organization · The reason(s) why you consider the situation may (or may be perceived to) give rise to a conflict between your personal interests and your public duty as a Councillor. |

|

If Pecuniary |

Leave chamber |

|

If Non-pecuniary (tick one) |

Disclose & vote Disclose & not vote Leave chamber |

|

Reason for action proposed |

Clause 5.11 of Council’s Code of Conduct provides that if you determine that a non-pecuniary conflict of interest is less than significant and does not require further action, you must provide an explanation of why you consider that conflict does not require further action in the circumstances |

|

Print Name |

I disclose the above interest and acknowledge that I will take appropriate action as I have indicated above. |

|

Signed |

|

NB: Please complete a separate form for each Item on the Council Agenda on which you are declaring an interest.

|

Council |

27 May 2020 |

Recommendation

That the Minutes of the Ordinary Meeting held on 20 May 2020 as circulated, be taken as read and confirmed.

Pecuniary, Non-Pecuniary and Political Donation Disclosures to be declared and tabled. Declarations also to be prior to discussion on each item.

Nil Reports

Nil Reports

Nil Reports

Nil Reports

12.1 Review of Long Term Financial Plan.............................................................................................. 8

13.1 Quarterly Budget Review Statement - 31 March 2020........................................................... 12

Representations by members of the public regarding closure of part of meeting

Adjournment Into Closed Session, exclusion of the media and public............................ 38

Council |

27 May 2020 |

12.1 Review of Long Term Financial Plan...................................................................... 8

|

Council 27 May 2020 |

Item 12.1 |

12.1. Review of Long Term Financial Plan

The Long Term Financial Plan is presented to Council for consideration and public exhibition.

Director Business & Governance

That the Long Term Financial Plan be placed on public exhibition from 28 May 2020 as a supporting document for the 2021 Operational Plan and Budget.

Executive Summary

Council adopted the Resourcing Strategy, which included its Financial Strategy and Long Term Financial Plan (LTFP) in 2017. At that time Council considered a range of options and resolved its position, for the adopted plans, with the major focus on asset management and outlining a range of projects and actions to progress over the period 2017 to 2020.

At its meeting on 11 December 2019, Council resolved to place the Draft Revised Bega Valley Shire Delivery Program 2017 – 2021 and Operational Plan 2020-2021 including the budget, Financial Strategy and LTFP on an extended public exhibition in accordance with Sections 404 and 405 of the Local Government Act 1993.

Council was seeking amendments to its Financial Strategy and LTFP because of the proposed Special Rate Variation application. Due to the 2020 Black Summer Bushfires Council resolved to revoke its proposal to consider an SRV which lead Officers to review and refocus these key documents. The LTFP was amended and updated and presented to the Council meeting on 20 May 2020 for exhibition. Councillors raised several issues relating to line items in the plan, specifically forward projections for depreciation, loans and interest. Council resolved to have these items further addressed by staff and to consider the LTFP at this meeting.

Background

Council’s Resourcing Strategy, adopted in 2017, outlines the planned way forward for Council in relation to the critical areas of workforce, financial strategy, asset management, technology and plant. Council has considered several reports since the Council elections in September 2016, outlining the approach to enacting the adopted LTFP. The LTFP outlined two potential increases to general rates above rate pegging through applications for special rate variations. At that time, the financial challenges of continuing to provide the level of infrastructure and services required by the community without an increase of revenue in to the General Fund were articulated.

Throughout 2017, Council undertook a full review of its financial position, particularly in relation to the considerable assets Council owns, operates, and manages. Council adopted its Community Strategic Plan, Resourcing Strategy and Delivery Program with a specific focus, resolved at its meeting on 28 June 2017, to continue to strategically address financial sustainability in all asset classes and moving to ensure that the Council consider potential disposal, rationalisation, efficiencies and improved management and operations of assets into the future. Work on this has been continuing however it has been difficult and impacted further by Council being successful at leveraging considerable external funding for capital works further impacting our financial projections.

Council resolved on the Financial Strategy and LTFP utilising an Asset Management approach and adopted aspects of models presented, framed as the “Asset Management Model”. This included several proposed SRVs moving forward. These were described as providing an alternative model for tourism marketing and promotions funding; provision of new, or upgraded, recreation assets such as swimming pools; and critical transport and community asset improvements including those aimed to build resilience against storm damage.

Over the period July to December 2017 a further, more detailed, review of all asset classes was undertaken with direction moving forward to focus on being able to maintain and renew current assets and identify efficiencies, and potential asset rationalisation. Workshops were held on each asset class and a full, detailed report presented to Council on 13 December 2017.

Over this period Council has also:

· reviewed its services

· restructured the organisation on two occasions to achieve operational savings

· responded to several significant disaster events with two fires in 2018

· received in excess of $75m additional grant income for assets

· considered reports on land divestment

· divested itself of buildings through sale

· improved its works programs to gain efficiencies and extend works undertaken

· developed a Network Operations Centre to improve planning and delivery of works

· resolved to hand back assets to the State Government

· reviewed its six pool strategy; and

· undertaken more detailed discussions relating to pools and public amenities.

At the meeting on 20 May 2020 it was recommended to place the revised LTFP Strategy on public exhibition. Councillors had several queries not raised in previous iterations of the draft which were considered necessary to review and rework prior to placing on public exhibition with the 2021 Operational Plan, Budget, Fees and Charges and Revenue Policy.

The items raised relate to:

· depreciation modelling moving forward particularly including the impact of large capital expenditure across all funds

· loan repayments moving forward; and

· interest modelling.

The Long Term Financial Plan presented on 20 May 2020 has continued the methodology for these items endorsed since 2017. Currently:

· The deprecation calculation is consolidated across all asset funds, based on previous year’s actuals. This is why projected depreciation calculations do not see a significant increase as a result of expected additional capital assets. The current method uses asset revaluations to inform future depreciation projections.

· Loan repayments. It is noted that a number of loans will be repaid during this LTFP period. It is recommended that in accordance with the Financial Strategy, future borrowings are considered as an option to fund capital projects that are identified in the asset management strategy and support intergenerational equity. This is an assumption that should be explored in future LTFPs. The asset valuation (transport infrastructure) due to be completed this financial year will give us better information to support a more robust funding model for renewals over future years.

· The current model of interest calculations is based on historical performance and influenced by external markets as documented in the body of the plan. It is noted that the Operational Plan includes a project to review Council’s Investment policy which will inform future LTFPs.

The Council resolution to introduce a finance working group session monthly as part of the Councillor briefing sessions will be a key instrument in working through various options to re-model the underlying assumptions for depreciation, borrowings and interest.

Another item raised by Councillors was consideration of a future special rate variation which is outlined in the document. It is recommended that the document presented be supported which includes a special rate variation of 5% for the General Fund, commencing in 2023. This will be needed if assets are not significantly reduced and current modelling sees continued growth.

It should be noted that the LTFP is reviewed annually. Over the coming twelve months if Council resolves to reduce assets and services over the LTFP and make other decisions linked to the approach adopted in 2017 of asset management then over the next year this can be considered and modelled appropriately. Again this is an item that the Councillors and staff should focus on in relation to ensuring a sustainable position into the longer term.

Community Engagement

Consultation Planned

The Revised Long Term Financial Plan will placed on public exhibition with the other IPR documents from Thursday 28 May 2020.

Public notices will be placed online via Council’s website, local media. A 'Have Your Say' page will be created on Councils website along with posts on Councils Facebook page. Content will also appear in Council News, our regular newsletter.

Attachments

Nil

|

Council |

27 May 2020 |

13.1 Quarterly Budget Review Statement - 31 March 2020....................................... 12

|

Item 13.1 |

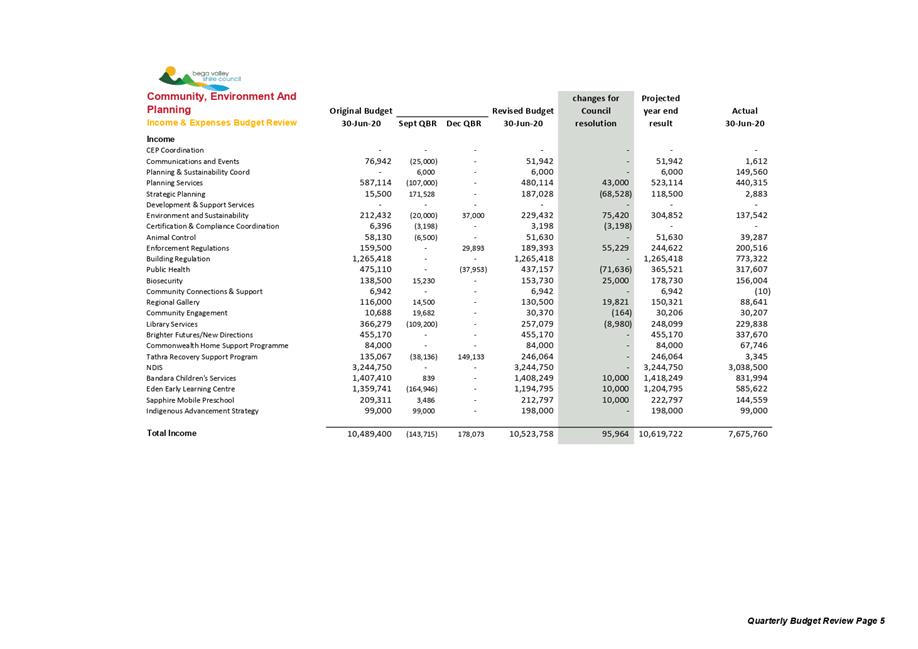

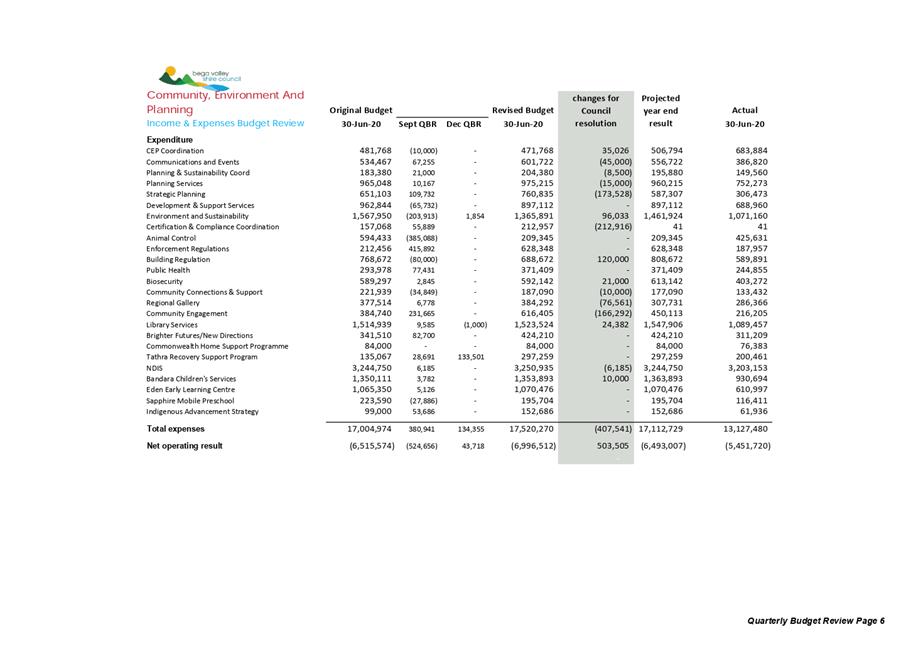

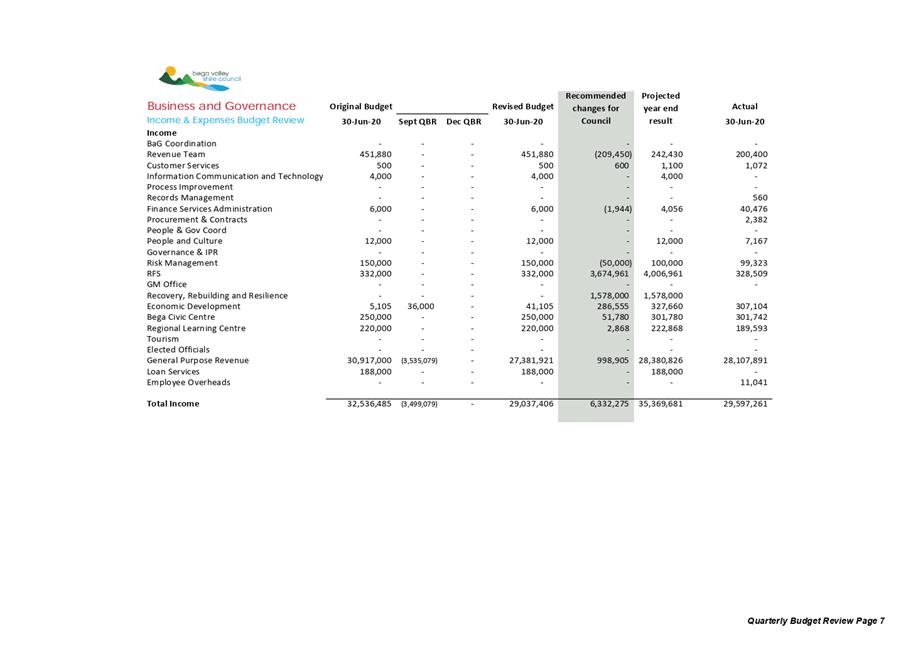

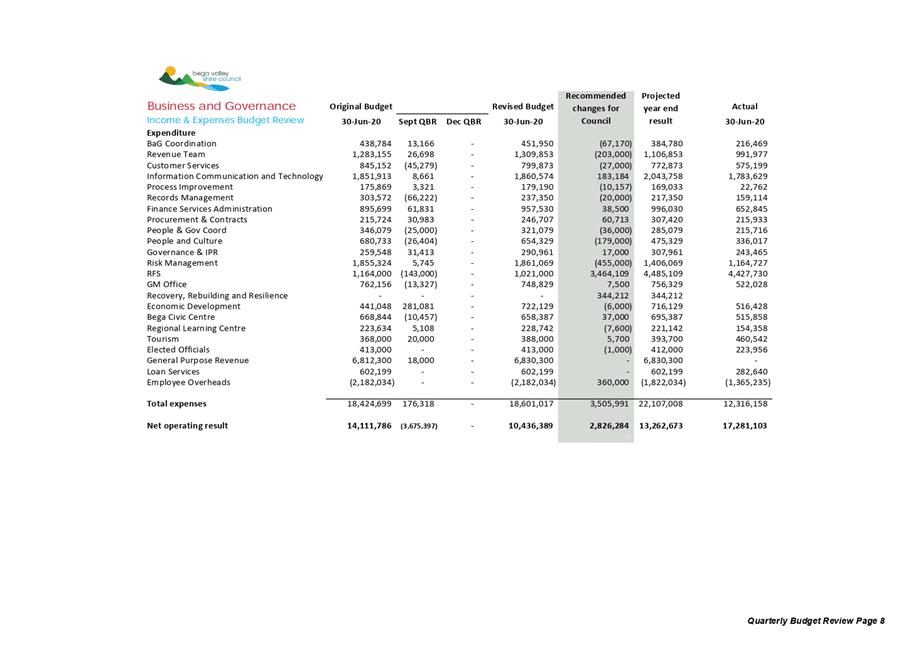

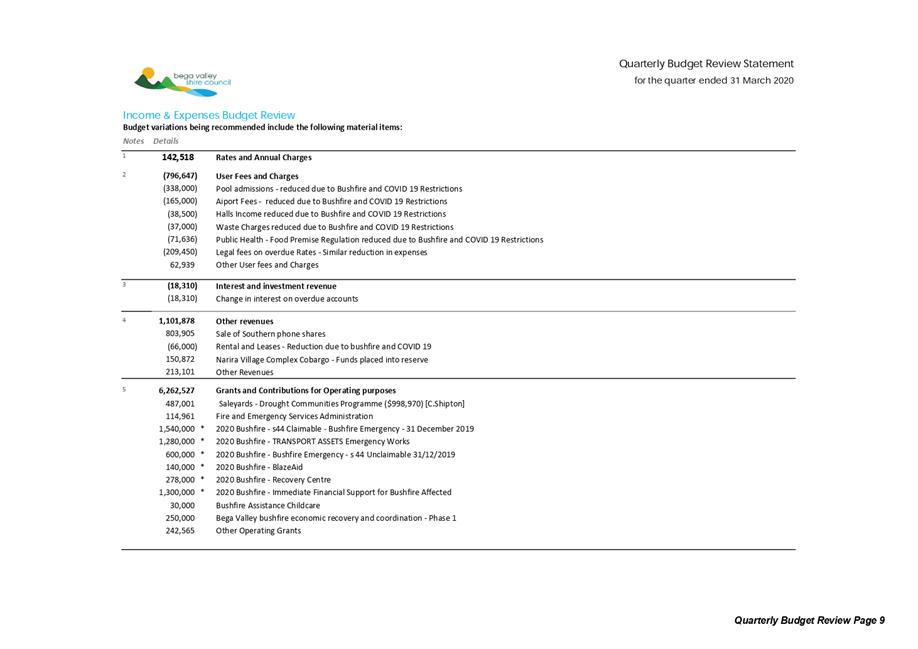

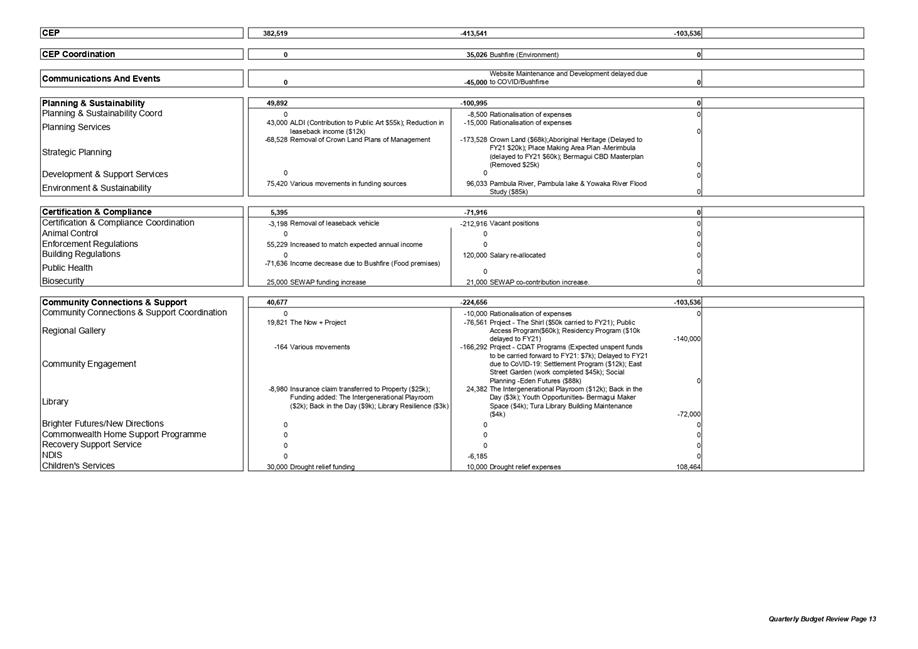

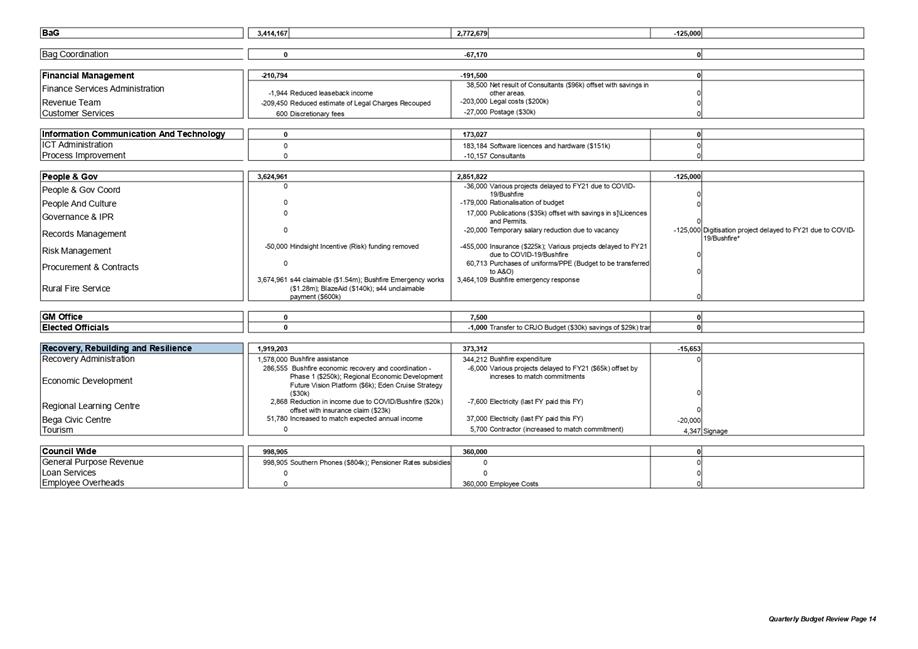

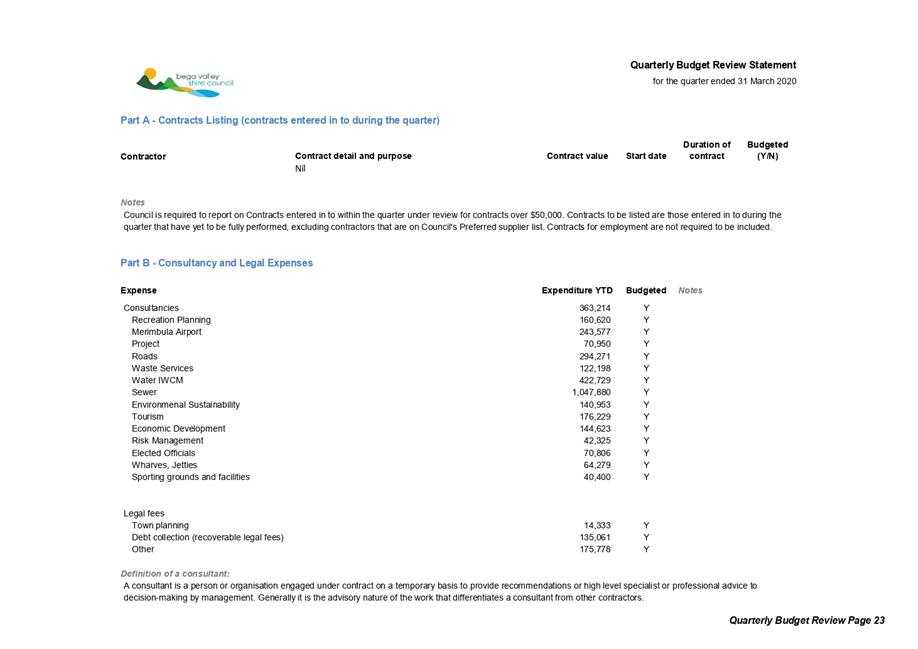

Quarterly Budget Review Statements (QBRS) are prepared and presented to Council in accordance with Section 203 of the Local Government (General) Regulation 2005.

Director Business & Governance

1. That Council receive and note the March 2020 Quarterly Budget Review Statement.

2. That the budget recommendations detailed in the March 2020 quarterly budget review statement be adopted.

Executive Summary

Under the Integrated Planning and Reporting (IPR) Guidelines, a Quarterly Budget Review Statement (QBRS) must be presented to Council for each financial quarter.

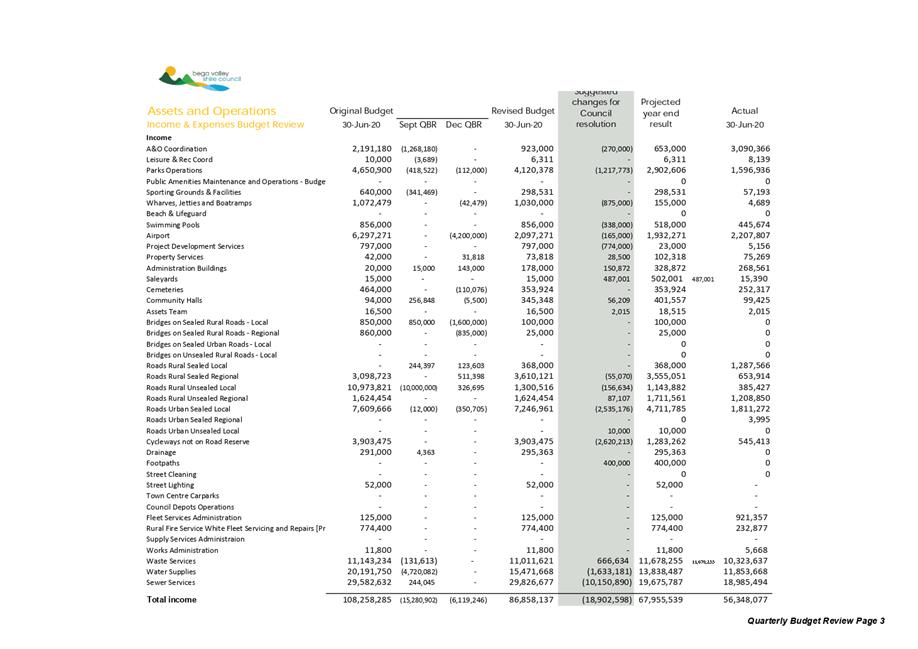

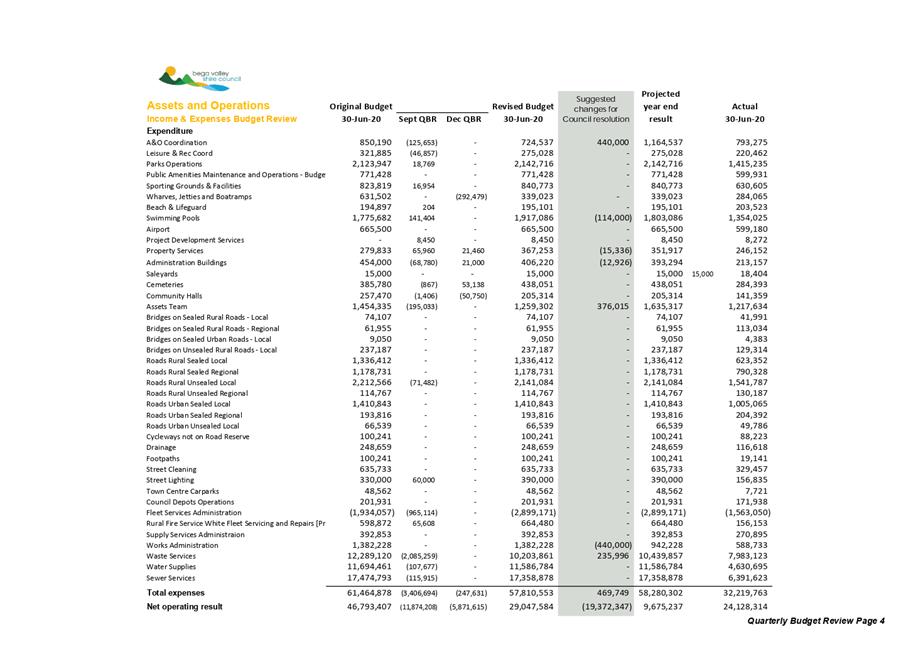

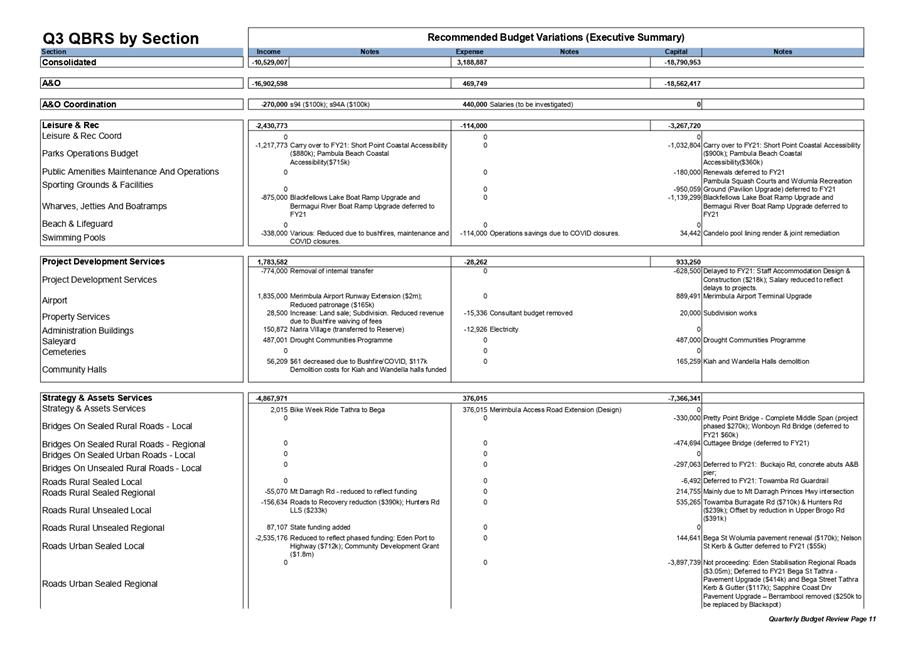

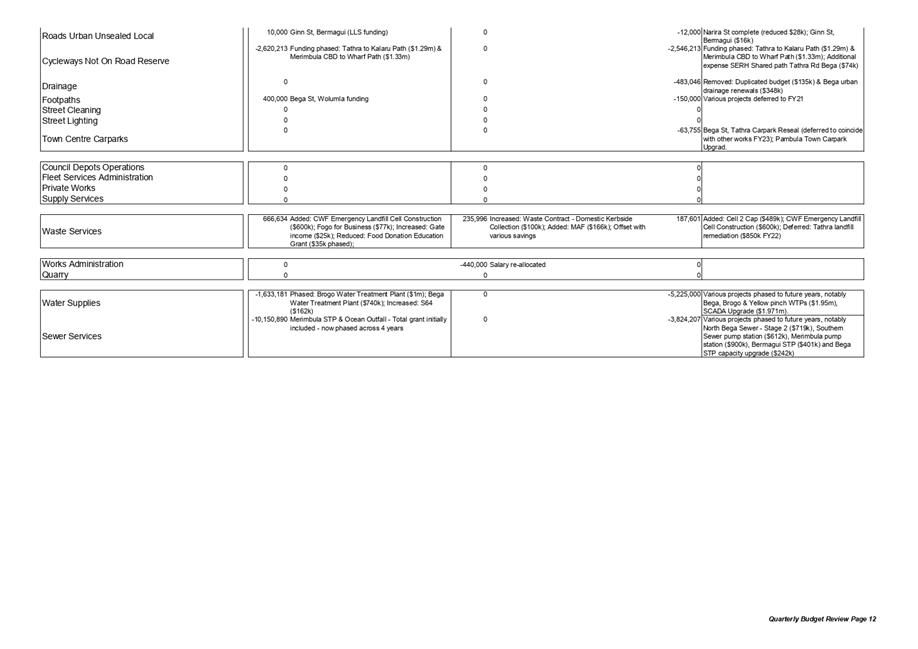

The QBRS is presented in a summary format which shows Council’s income and expenses by type and by activity. The Capital Budget Review Statement (CBRS) is also prepared by type followed by variance details. It is the intent of this report to provide information and illustrate the financial performance of Council as a whole and for each activity of Council.

Council officers retain the ability to enquire, transact, and report on the detailed general ledger, which includes budgets. If there are specific questions relating to detailed transactional information, officers can provide answers to those questions.

Financial and resource considerations

Operating Result

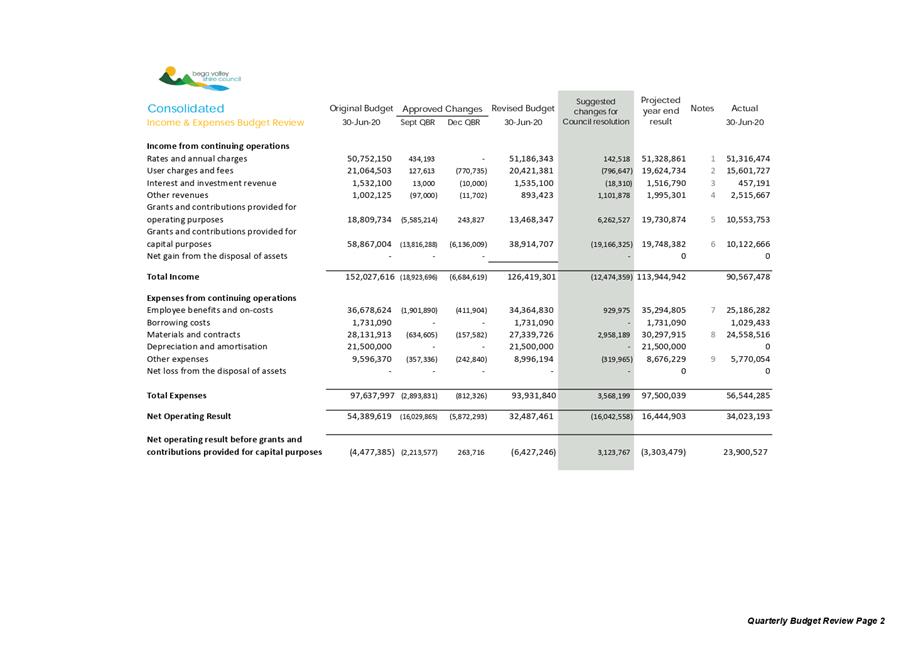

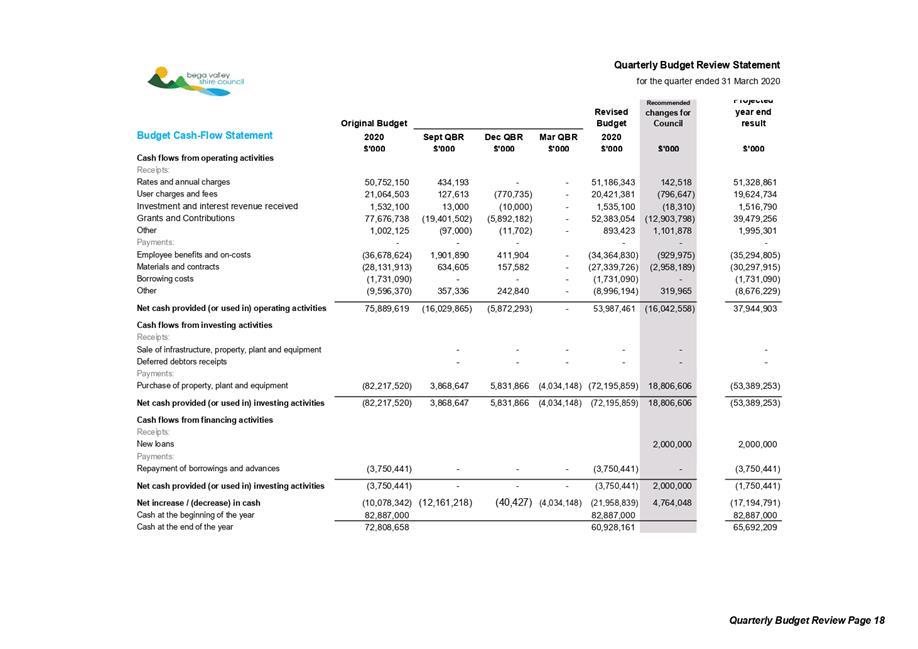

Council’s budgeted surplus has decreased by $16,042K from $32,487K in December 2019 to $16,445K in March 2020. The net operating result before Capital items has improved by $3,124K with the expected 30 June 2020 deficit result of $3,303K.

Within Councils income streams there have been some improvement in rates income of $145K as a result of growth in the Bega Valley. We also have a decrease in fees and charges ($741K) and investment income ($18K) following the both natural disasters and COVID 19 restrictions and support provided by Council.

Operational Grants have increased by $6.2 million dollars, included in this amount is $5.2 million of grants allocated in this quarter.

· $1,300,000 dollars Immediate Financial Support for Bushfire Affected

· $1,500,000 Sec 44 claimable costs

· $1,280,000 DFRA Million Make safe costs

· $300,000 Recovery Centre costs currently

· $250,000 Bushfire Economic Recovery

· $487,001 Drought Communities funding

· $114,961 Emergency Levy payment from OLG

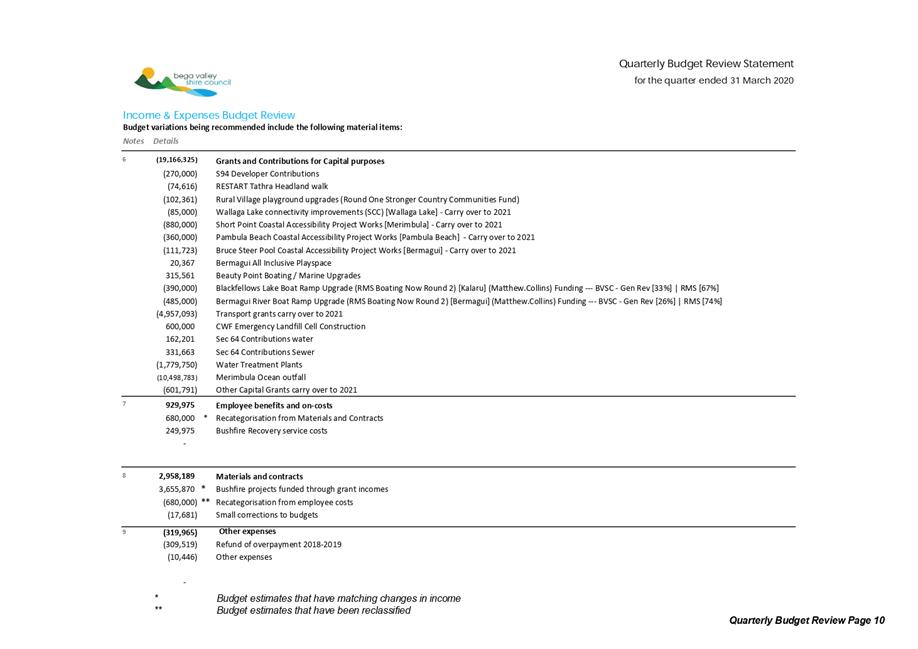

Capital Grants decreased by $19.1 million. Included in this amount are

· $270,00 decrease in Section 94 capital contributions from development fees

· $10,498,783 decrease Merimbula ocean outfall – correct phasing now included in Long Term Financial Plan

· $9,349,223 decrease due to projects not expected to be completed by June and carried forward into the advertised Operational Plan

Expenses increased by $3.56 million. Increases in employee costs $930K. Materials and contracts of $2,958K can be attributed to the operational grant increases. A decrease in other expenses is reimbursement of an overpayment in the 2018/2019 year.

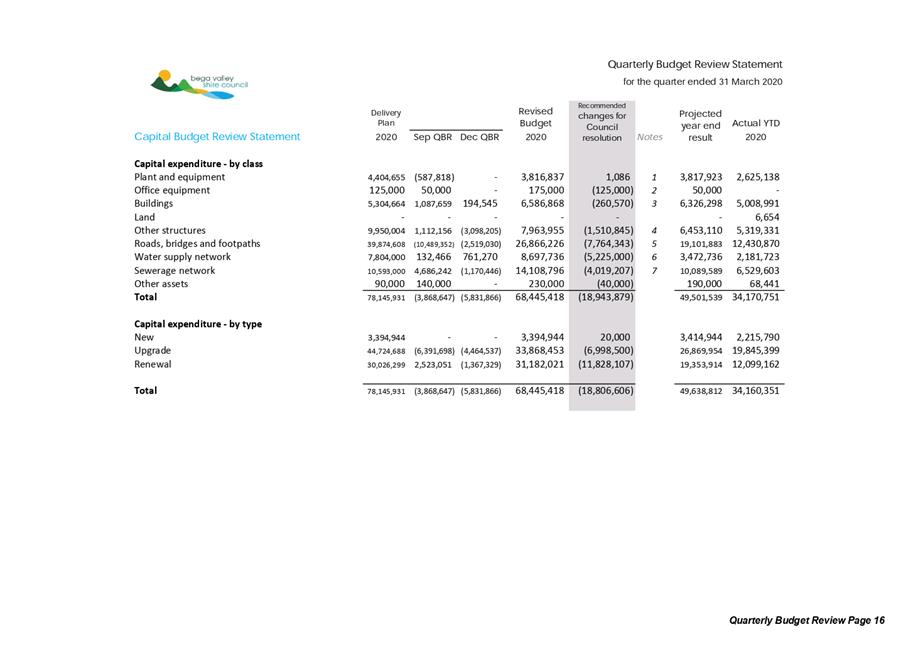

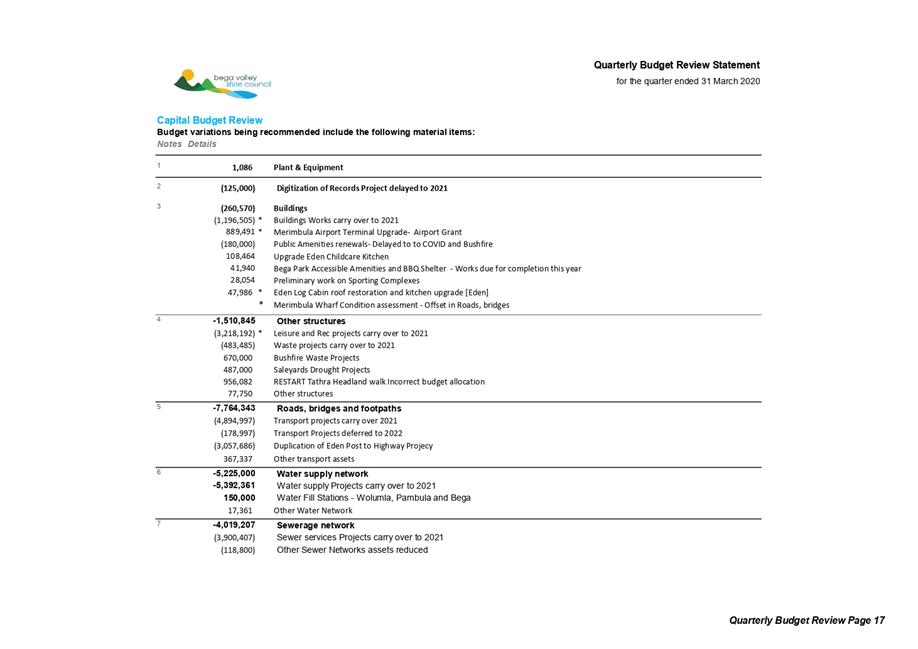

Capital

Capital expenditure is estimated to reduce by $18.9 million dollars in the March QBRS to $49.5 million. A review of the capital program was conducted and several projects were identified that wouldn’t be completed in the current year. These have been carried over to be completed in the 2021 Operational Plan.

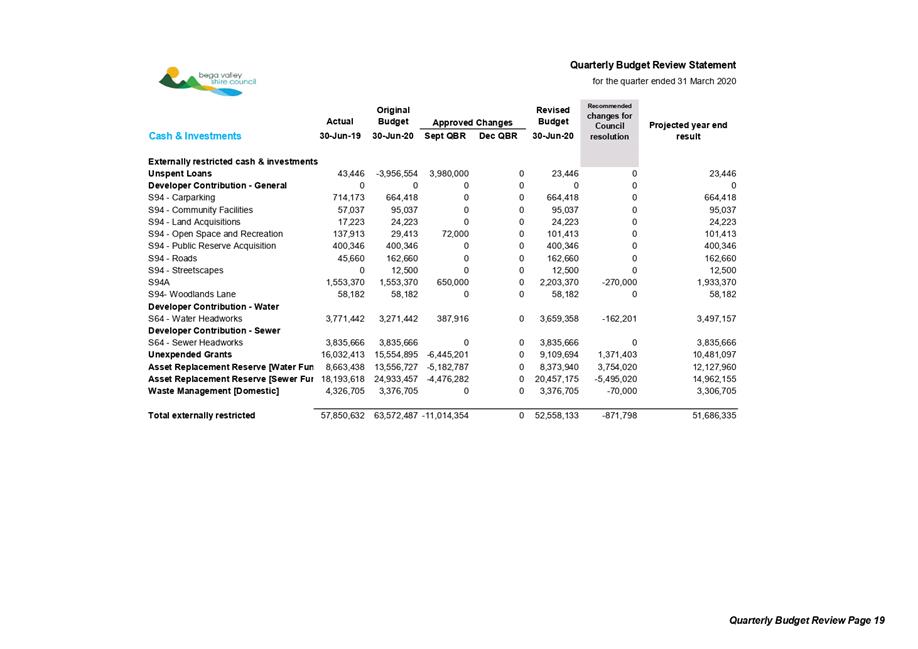

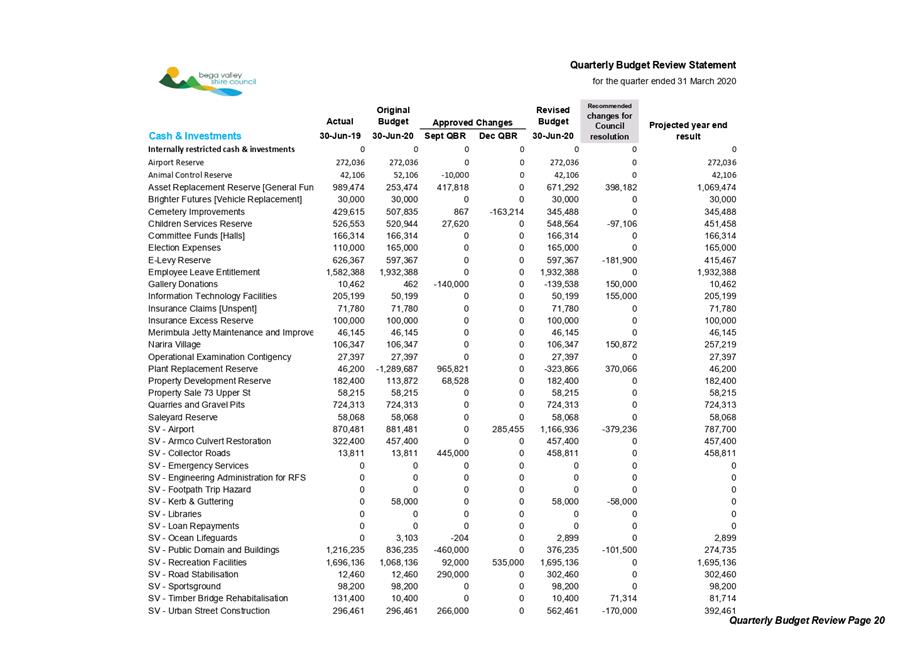

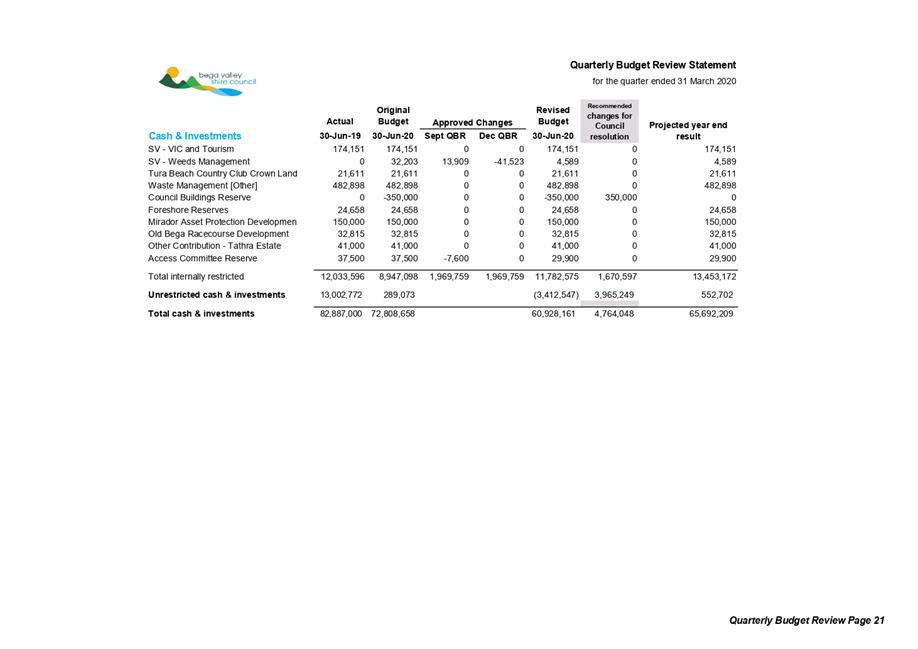

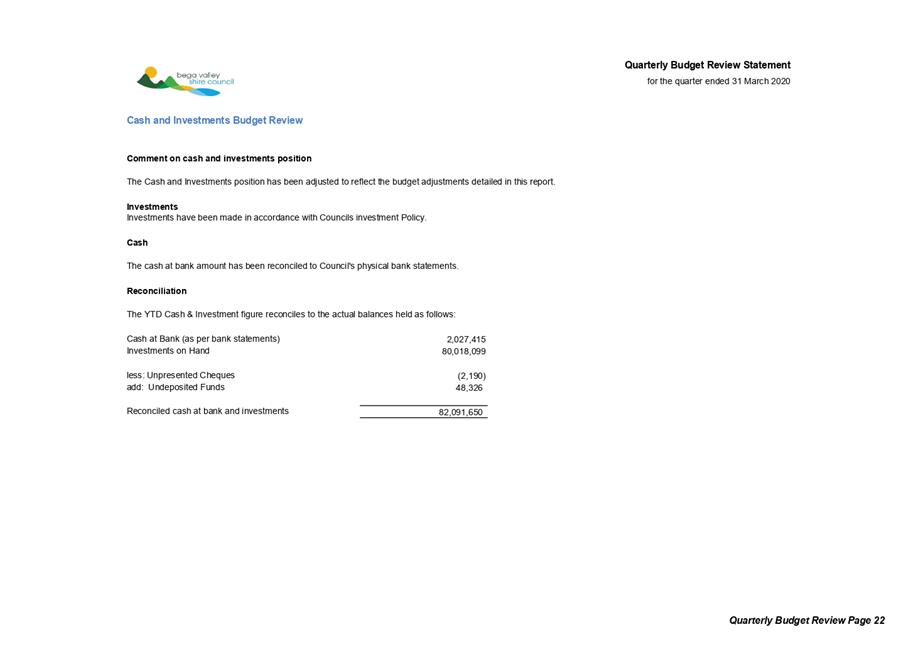

Cash and Investments

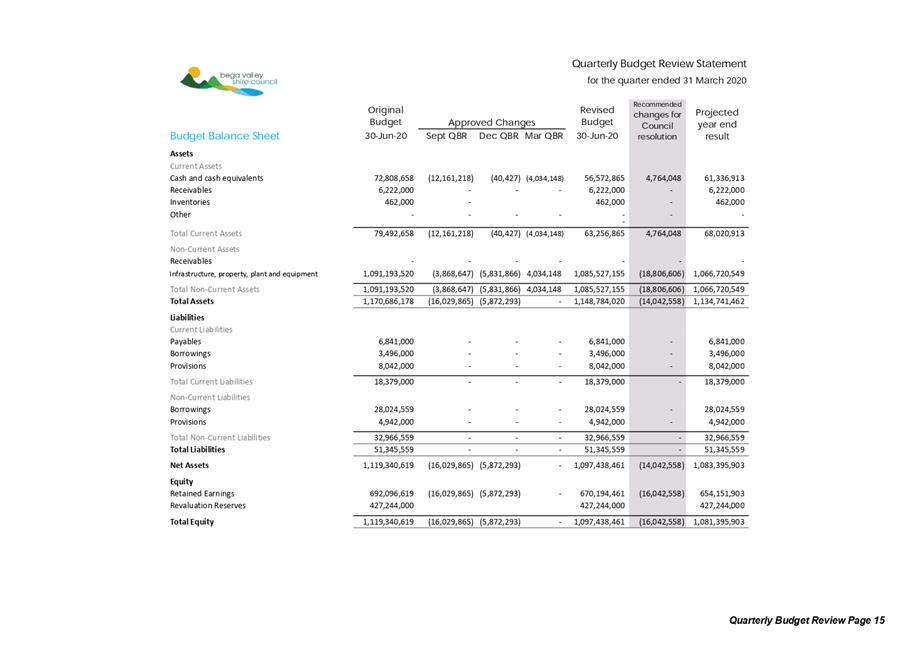

Council had cash and investments of $88,887K at 30 June 2019, the revised projected cash figure at the 30 June 2020 is expected to be $65,692k. Our investments have been impacted by the economic downturn due to COVID-19 pandemic.

Legal /Policy

In accordance with Regulation 203(1) of the Local Government (General) Regulation 2005, the Responsible Accounting Officer must prepare and submit to the Council a Budget Review Statement after the end of each quarter.

Clause 203 of the Local Government (General) Regulations 2005 states:

Budget Review Statements and revision of estimates

1. Not later than two months after the end of each quarter (except the June quarter), the responsible accounting officer of a council must prepare and submit to the council a budget review statement that shows, by reference to the estimate of income and expenditure set out in the statement of the council’s revenue policy included in the operational plan for the relevant year, a revised estimate of the income and expenditure for that year.

2. A budget review statement must include or be accompanied by:

a. A report as to whether or not the responsible accounting officer believes that the statement indicates that the financial position of the council is satisfactory, having regard to the original estimate of income and expenditure, and

b. If that position is unsatisfactory, recommendations for remedial action.

c. A budget review statement must also include any information required by the Code to be included in such a statement.

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

Council’s 2017–2021 Delivery Program and 2019-2020 Operational Plan provides the Financial Estimates 2017–2021 which includes the Budget for 2019-20.

Council will need to be mindful in reviewing the Long-Term Financial Plan, that it is not likely to have the same level of external grant funding into the future, and that an expansion of the current asset base will put pressure on future budgets through increased operation, maintenance and depreciation costs.

Given the issues highlighted by Council in achieving its Asset Management model, future gains or surpluses need to be placed into appropriate reserves to provide coverage for future liabilities.

1⇩. Long Term Financial (QBRS Q3)