|

Urgent ExtraordinaryMeeting Notice and Agenda

An Urgent Extraordinary Meeting of the Bega Valley

Shire Council will be held at Council Chambers, Biamanga Room Bega Valley Commemorative

Civic Centre Bega on

|

|

Urgent ExtraordinaryMeeting Notice and Agenda

An Urgent Extraordinary Meeting of the Bega Valley

Shire Council will be held at Council Chambers, Biamanga Room Bega Valley Commemorative

Civic Centre Bega on

|

Council meetings are recorded and live streamed to the Internet for public viewing. By entering the Chambers during an open session of Council, you consent to your attendance and participation being recorded.

The recording will be archived and made available on Council’s website www.begavalley.nsw.gov.au. All care is taken to maintain your privacy; however as a visitor of the public gallery, your presence may be recorded.

The Agendas for Council Meetings and Council Reports for each meeting will be available to the public on Council’s website as close as possible to 5.00 pm on the Thursday prior to each Ordinary Meeting. A hard copy is also made available at the Bega Administration Building reception desk and on the day of the meeting, in the Council Chambers.

The Minutes of Council Meetings are available on Council's Website as close as possible to 5.00 pm on the Monday after the Meeting.

1. Please be aware that the recommendations in the Council Meeting Agenda are recommendations to the Council for consideration. They are not the resolutions (decisions) of Council.

2. Background for reports is provided by staff to the General Manager for presentation to Council.

3. The Council may adopt these recommendations, amend the recommendations, determine a completely different course of action, or it may decline to pursue any course of action.

4. The decision of the Council becomes the resolution of the Council, and is recorded in the Minutes of that meeting.

5. The Minutes of each Council meeting are published in draft format, and are confirmed by Councillors, with amendments if necessary, at the next available Council Meeting.

If you require any further information or clarification regarding a report to Counci, please contact Council’s Executive Assistant who can provide you with the appropriate contact details

Phone (6499 2104) or email execassist@begavalley.nsw.gov.au.

· Is the decision or conduct legal?

· Is it consistent with Government policy, Council’s objectives and Code of Conduct?

· What will the outcome be for you, your colleagues, the Council, anyone else?

· Does it raise a conflict of interest?

· Do you stand to gain personally at public expense?

· Can the decision be justified in terms of public interest?

· Would it withstand public scrutiny?

A conflict of interest is a clash between private interest and public duty. There are two types of conflict:

· Pecuniary – regulated by the Local Government Act 1993 and Office of Local Government

· Non-pecuniary – regulated by Codes of Conduct and policy. ICAC, Ombudsman, Office of Local Government (advice only). If declaring a Non-Pecuniary Conflict of Interest, Councillors can choose to either disclose and vote, disclose and not vote or leave the Chamber.

· Is it likely I could be influenced by personal interest in carrying out my public duty?

· Would a fair and reasonable person believe I could be so influenced?

· Conflict of interest is closely tied to the layperson’s definition of ‘corruption’ – using public office for private gain.

· Important to consider public perceptions of whether you have a conflict of interest.

1st Do I have private interests affected by a matter I am officially involved in?

2nd Is my official role one of influence or perceived influence over the matter?

3rd Do my private interests conflict with my official role?

For more detailed definitions refer to Sections 442, 448 and 459 or the Local Government Act 1993 and Model Code of Conduct, Part 4 – conflictions of interest.

Whilst seeking advice is generally useful, the ultimate decision rests with the person concerned.Officers of the following agencies are available during office hours to discuss the obligations placed on Councillors, officers and community committee members by various pieces of legislation, regulation and codes.

|

Contact |

Phone |

|

Website |

|

Bega Valley Shire Council |

(02) 6499 2222 |

council@begavalley.nsw.gov.au |

www.begavalley.nsw.gov.au |

|

ICAC |

8281 5999 Toll Free 1800 463 909 |

icac@icac.nsw.gov.au |

www.icac.nsw.gov.au |

|

Office of Local Government |

(02) 4428 4100 |

olg@olg.nsw.gov.au |

http://www.olg.nsw.gov.au/ |

|

NSW Ombudsman |

(02) 8286 1000 Toll Free 1800 451 524 |

nswombo@ombo.nsw.gov.au |

Under the provisions of Section 451(1) of the Local Government Act 1993 (pecuniary interests) and Part 4 of the Model Code of Conduct prescribed by the Local Government (Discipline) Regulation (conflict of interests) it is necessary for you to disclose the nature of the interest when making a disclosure of a pecuniary interest or a non-pecuniary conflict of interest at a meeting.

The following form should be completed and handed to the General Manager as soon as practible once the interest is identified. Declarations are made at Item 3 of the Agenda: Declarations - Pecuniary, Non-Pecuniary and Political Donation Disclosures, and prior to each Item being discussed:

Council meeting held on __________(day) / ___________(month) /____________(year)

|

Item no & subject |

|

|

Pecuniary Interest

|

In my opinion, my interest is pecuniary and I am therefore required to take the action specified in section 451(2) of the Local Government Act 1993 and or any other action required by the Chief Executive Officer. |

|

Significant Non-pecuniary conflict of interest |

– In my opinion, my interest is non-pecuniary but significant. I am unable to remove the source of conflict. I am therefore required to treat the interest as if it were pecuniary and take the action specified in section 451(2) of the Local Government Act 1993. |

|

Non-pecuniary conflict of interest |

In my opinion, my interest is non-pecuniary and less than significant. I therefore make this declaration as I am required to do pursuant to clause 4.17 of Council’s Code of Conduct. However, I intend to continue to be involved with the matter. |

|

Nature of interest |

Be specific and include information such as : · The names of any person or organization with which you have a relationship · The nature of your relationship with the person or organization · The reason(s) why you consider the situation may (or may be perceived to) give rise to a conflict between your personal interests and your public duty as a Councillor. |

|

If Pecuniary |

Leave chamber |

|

If Non-pecuniary (tick one) |

Disclose & vote Disclose & not vote Leave chamber |

|

Reason for action proposed |

Clause 4.17 of Council’s Code of Conduct provides that if you determine that a non-pecuniary conflict of interest is less than significant and does not require further action, you must provide an explanation of why you consider that conflict does not require further action in the circumstances |

|

Print Name |

I disclose the above interest and acknowledge that I will take appropriate action as I have indicated above. |

|

Signed |

|

NB: Please complete a separate form for each Item on the Council Agenda on which you are declaring an interest.

|

Extraordinary Council |

27 February 2019 |

Pecuniary, Non-Pecuniary and Political Donation Disclosures to be declared and tabled.

3.1 Calling of an Urgent Extraordinary Meeting........................................................ 8

4.1 Quarterly Budget review statement - 31 December 2018............................... 10

Extraordinary Council |

27 February 2019 |

3.1 Calling of an Urgent Extraordinary Meeting.............................................. 8

|

Extraordinary Council 27 February 2019 |

Item 3.1 |

Report to note calling of an Urgent Extraordinary meeting.

General Manager

Executive Summary

Following deputations to Council at the Extraordinary Meeting held at 10.00 am on 27 February 2019, Council resolved:

1. That as per Clause 10.2.1 due to the need to abandon the meeting called for 10.00am due to there being no calling for such a meeting signed by two Councillors.

2. That an Urgent Extraordinary Meeting be reconvened for 27 February 2019 at 11:00am.

Nil

|

Extraordinary Council |

27 February 2019 |

4.1 Quarterly Budget review statement - 31 December 2018....................... 10

|

Extraordinary Council 27 February 2019 |

Item 4.1 |

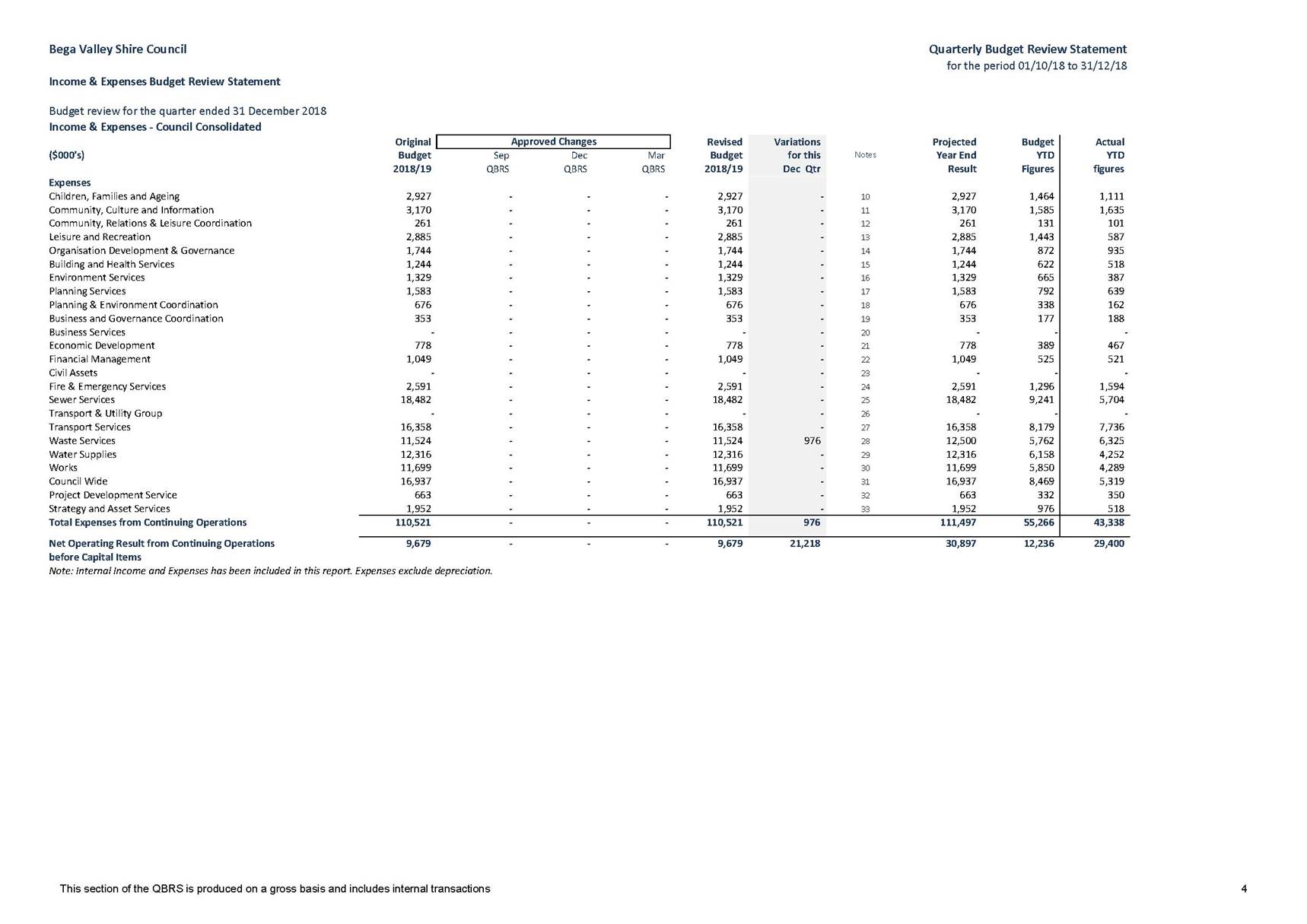

4.1. Quarterly Budget review statement - 31 December 2018

Budget review statements are prepared and presented to Council quarterly in accordance with Section 203 of the Local Government (General) Regulation 2005.

Director Business and Governance

|

1. That Council note the Chief Finance Officer’s position relating to the September quarterly review and consider this report to cover both statements. 2. That Council adopt the December 2018 Quarterly Budget Review. 3. That Council note movements outlined in the Quarterly Budget Review Statement. 4. That Council does not commit to any further additional expenditure, unless it is in conjunction with a Quarterly Budget Review and an alternate funding source can be identified. 5. That Council identify any of the items previously considered for funding to be included in the current budget review. 6. That Council note the items revoted to the 2018/19 year from the 2017/18 year. |

Executive Summary

Under the Integrated Planning and Reporting (IPR) Guidelines, a Quarterly Budget Review Statement must be presented to Council for each financial quarter.

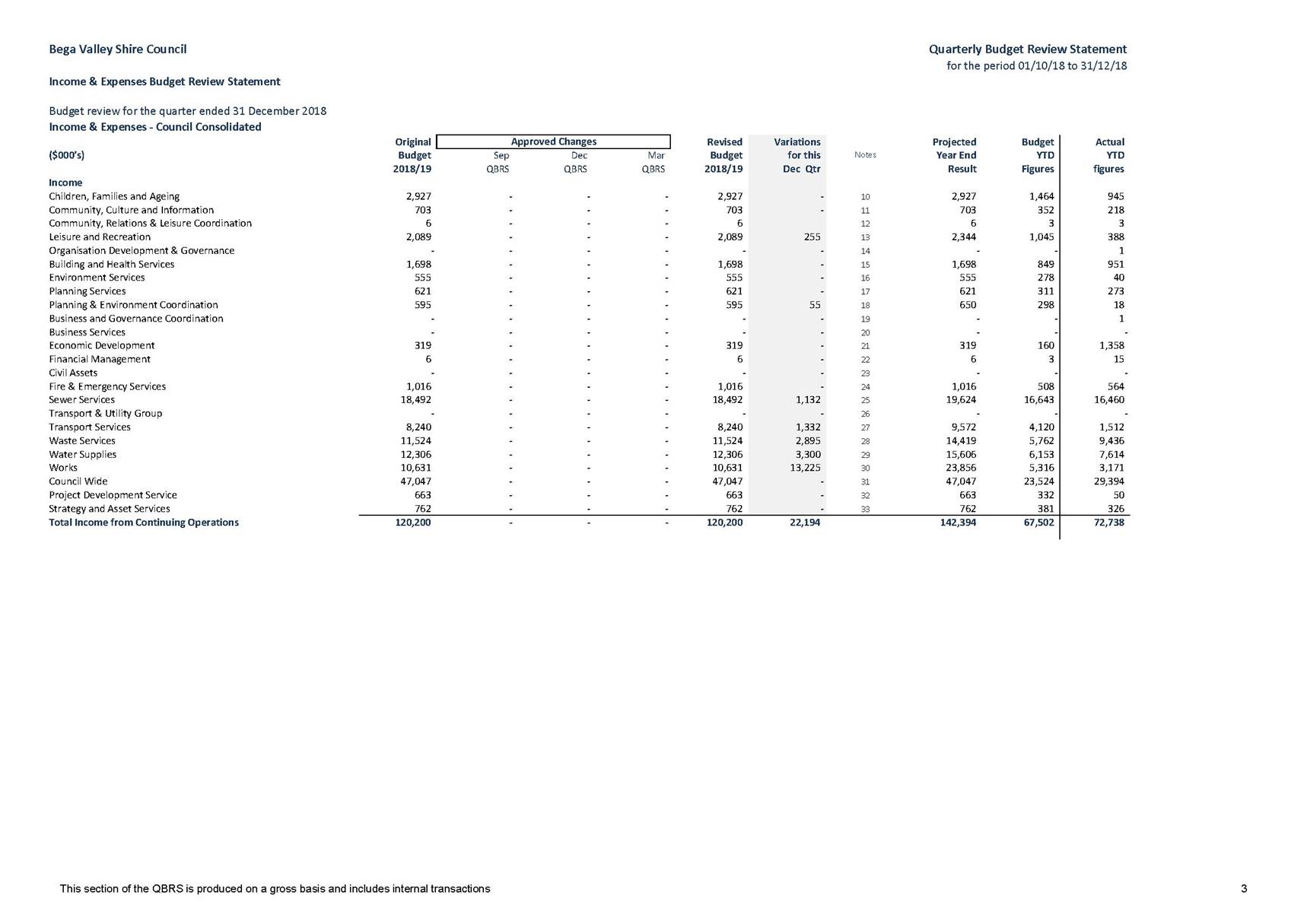

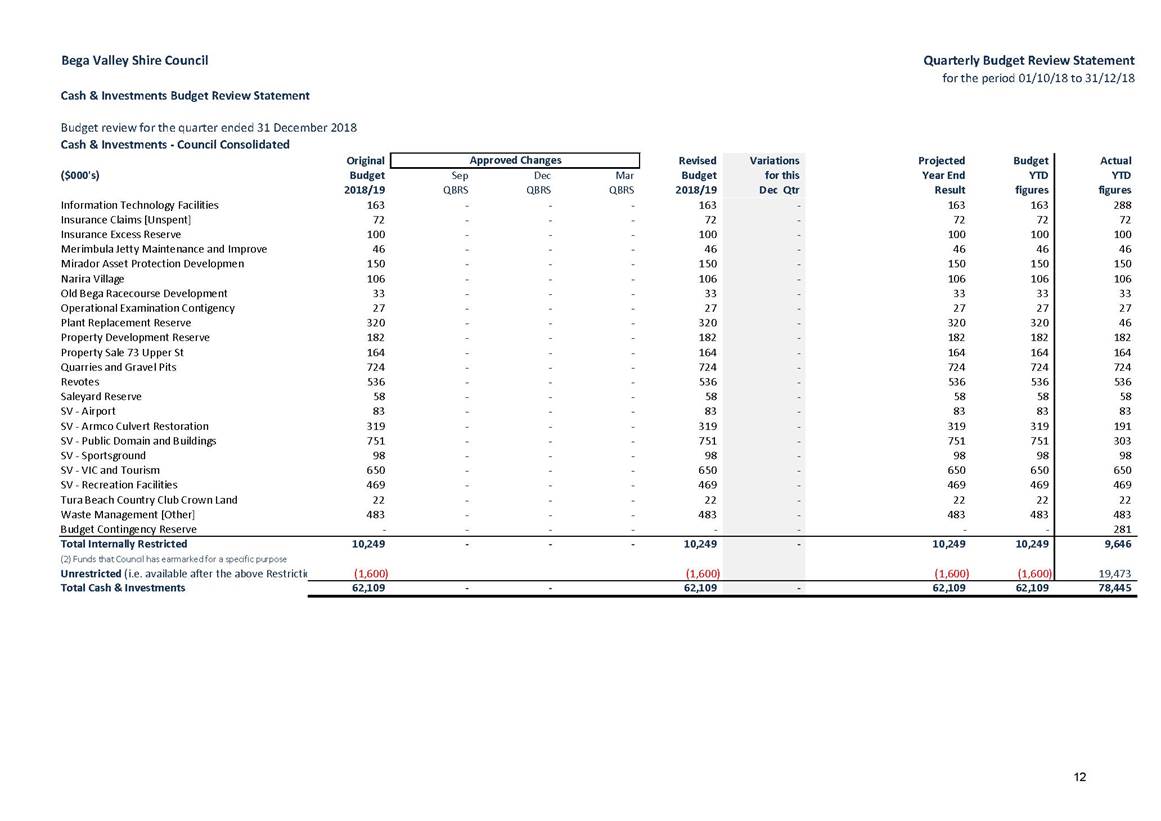

The Quarterly Budget Review Statement (QBRS) is presented in a summary format which shows Council’s income and expenses by type and by activity. The Capital Budget Review Statement (CBRS) is also prepared by type followed by variance details. It is the intent of this report to provide information to the users of the QBRS report, in order to illustrate the financial performance of Council as a whole and for each activity of Council.

Council officers retain the ability to enquire, transact, and report on the detailed general ledger, which includes budgets. If there are specific questions relating to detailed transactional information, officers can provide answers to those questions.

At the adoption of the Operational Plan and Budget on 27 June 2018 Council identified a number of projects that should be considered for funding following the end of year result. As some of these projects require certainty and planning, it is outlined here how this can now be considered prior to the end of financial year (EOFY) and first QBRS.

Due to an increased yield in the Financial Assistance Grant which was not known at the time of the adoption of the Operational Plan and Budget, funds are available to potentially support these projects to varying degrees.

Due to organisational impacts from two significant emergency events in the 2018 year and significant staff losses in the Finance Department of Council, negotiations were undertaken with the Office of Local Government, and the Auditor General’s Officer to extend the deadline for Annual Reporting of the 2017-2018 Financial Year. The Office of Local Government acknowledged the difficulty that Council staff had been placed under due to organisational impacts and advised that the end of year reporting should be the highest priority for Finance staff. Unfortunately this has meant that staff were unable to meet the end of year reporting requirements and the QBRS requirements for the September quarter concurrently. Now that the end of year reporting has been completed, staff are working to catch up on all tasks that were delayed due to the extra workload being undertaken by a reduced number of staff.

Background

At its meeting on 27 June 2018 Council as part of the adoption Resolution for the 2018/19 Operational Plan and Budget resolved:

· That the funding model proposed to identify some allocation for events and community support [following reduction of the Southern Phones dividend funding] not be applied. Instead, staff prepare a report to Council with the first quarterly budget review, following reconciliation of the end of year financial results, outlining potential avenues of funding to support the restoration of a community events funding allocation of $40,000, potential allocation to also be identified for the Merimbula VIC relocation and fit out, Bermagui charrette, and the sealing of the Plumb Motors Auckland Street Car park.

At the meeting on 19 September 2018 Council resolved to fund:

· $25,000 towards the Merimbula Visitors Information Centre (VIC) relocation

· $8,000 for WiFi connection to the Emergency Operations Centre

And: That the following items be deferred for consideration to a workshop and report following the presentation of the end of financial year and first quarterly budget review.

a. Community and events funding $40,000

c. Bermagui Charrette $10,000

d. Sealing of Plumb Motors Auckland Street car park (estimate) $35,000

f. General Manager’s support allocation for community groups $15,000

g. Allocation Merimbula Netball/Basketball project proposal $10,000

h. Allocation Cobargo skate park as per project proposal $10,000

i. Allocation to Reserve $72,000

j. Outdoor Sculpture acquisition and installation annual award $10,000

k. Allocation to the proposed Eden Skate Park

Funding for the Merimbula Netball/Basketball project proposal was also identified through the sports and recreation asset management area.

Options

Council has the option to allocate all or part of the unexpended additional income from the FAG at this time or defer the treatment of this additional income to a future quarterly budget review or consideration as part of the 2019/20 budget discussions.

1. ITEMS FROM COUNCIL RESOLUTION:

a. Community and events funding $40,000

b. Merimbula VIC relocation $25,000 FUNDED

c. Bermagui Charrette $10,000

d. Sealing of Plumb Motors Auckland

Street car park $35,000

2. CRITICAL REQUESTS:

a. WiFi connection for the EOC (requested by NSW Police, RFS) $8,000 FUNDED

b. General Manager’s support allocation for community groups $15,000

c. Allocation Merimbula Netball/Basketball project proposal $10,000

d. Allocation to Cobargo skate park

project proposal $10,000

3. ALLOCATION TO RESERVE $72,000

Financial and resource considerations

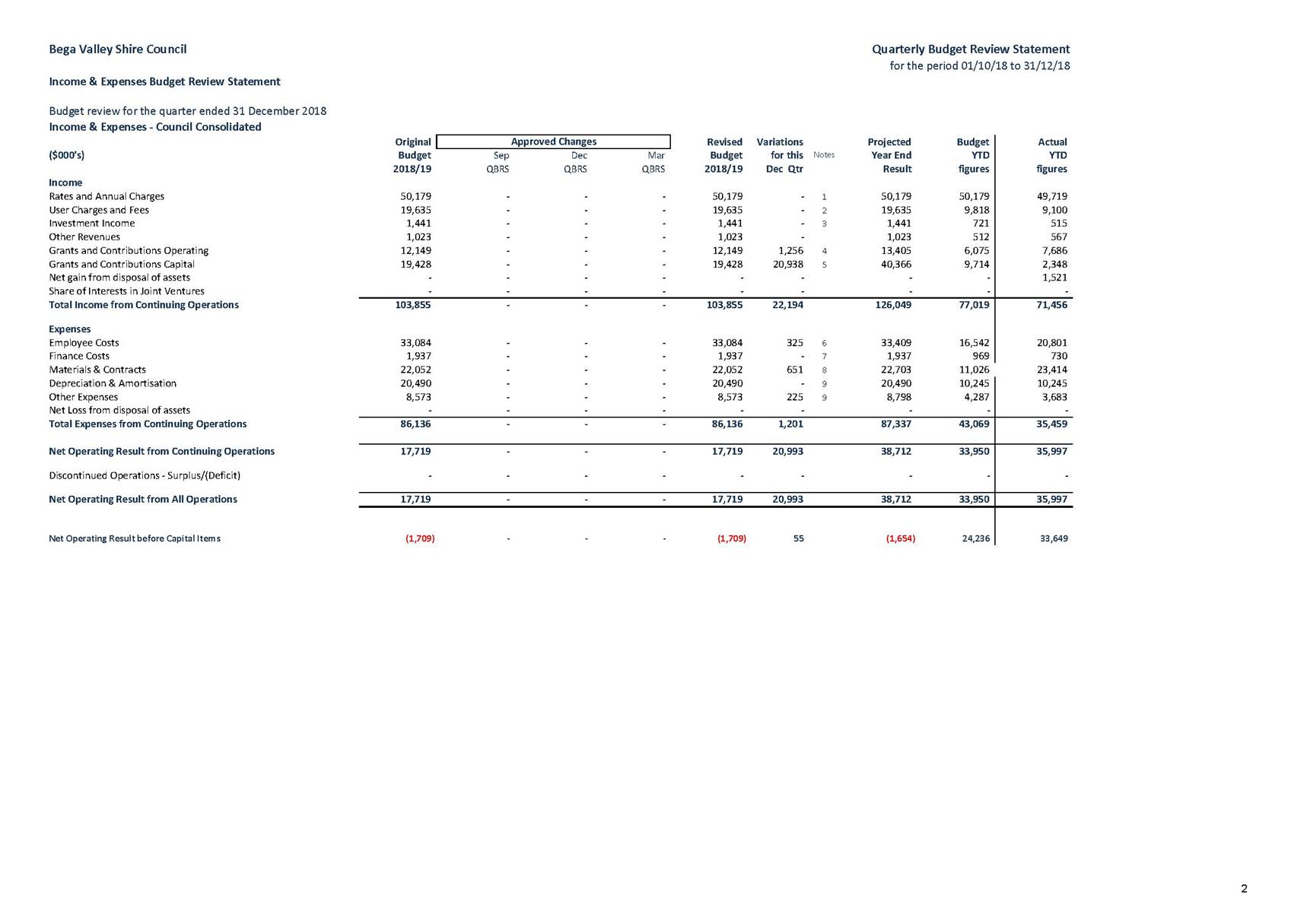

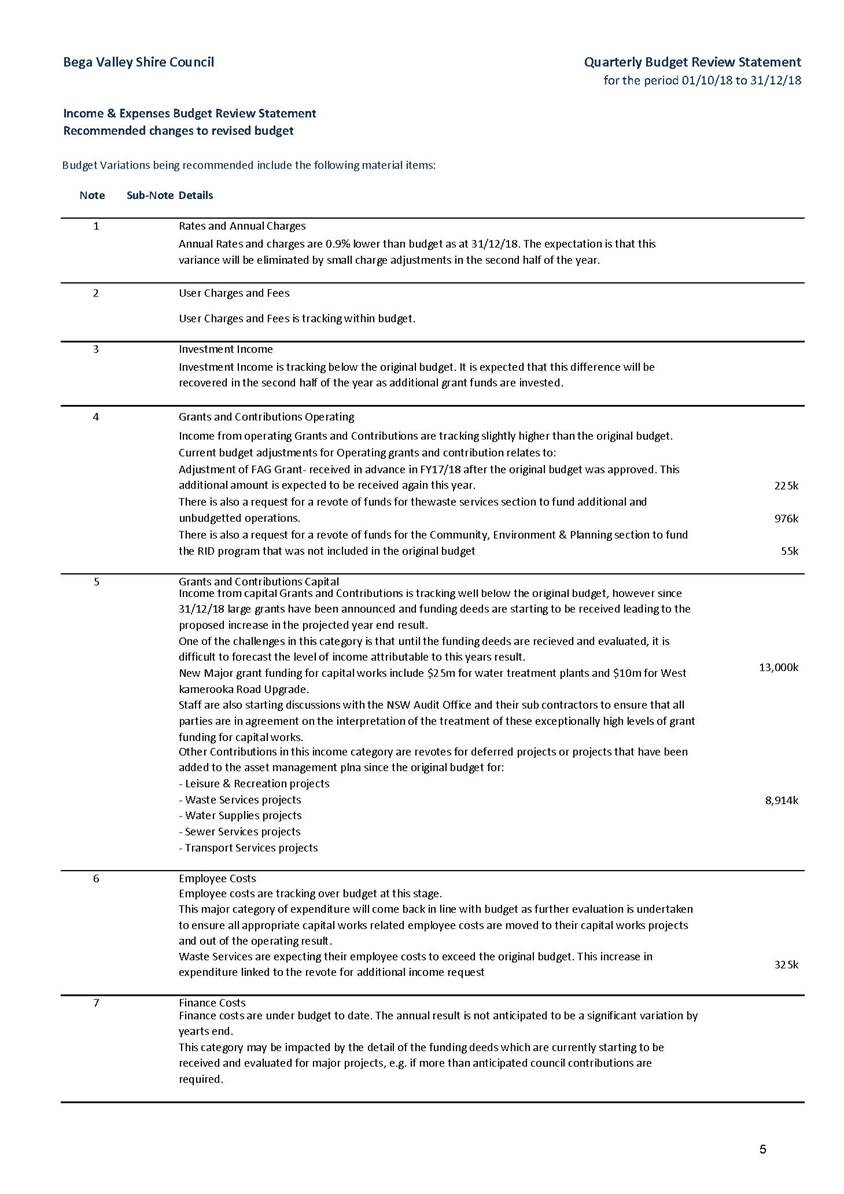

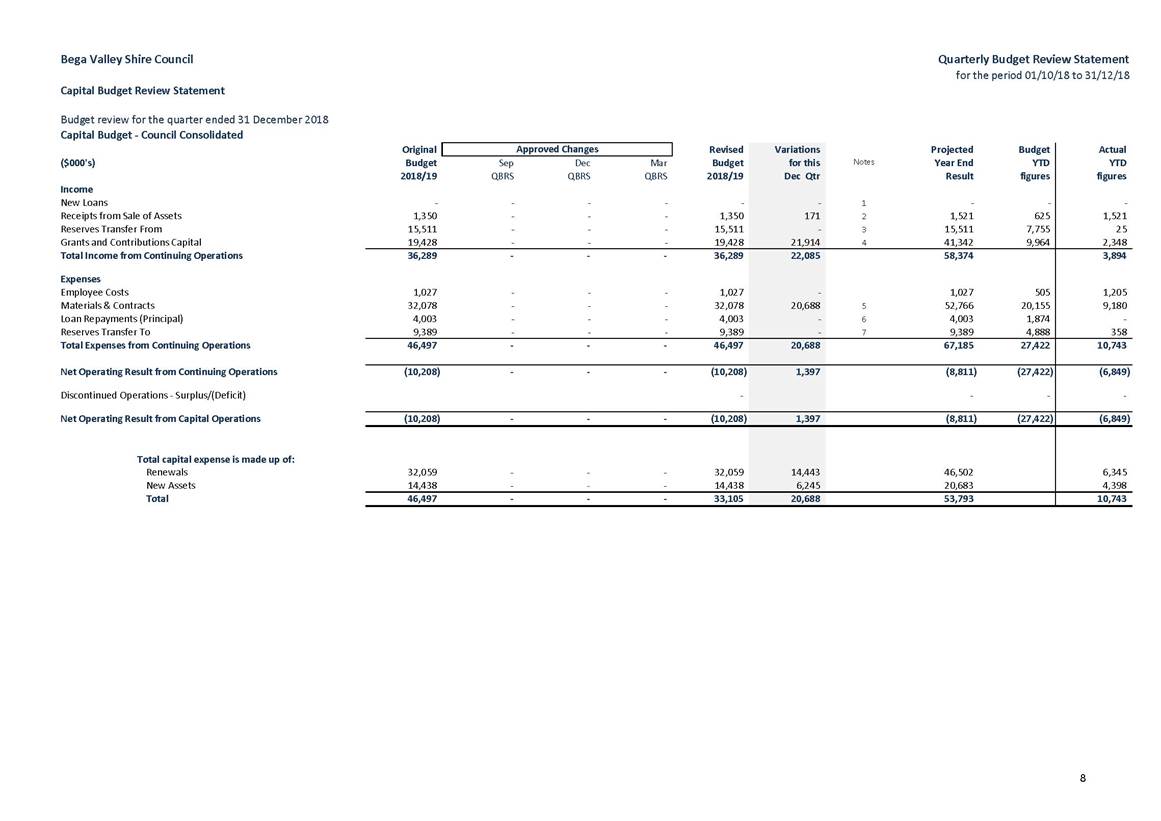

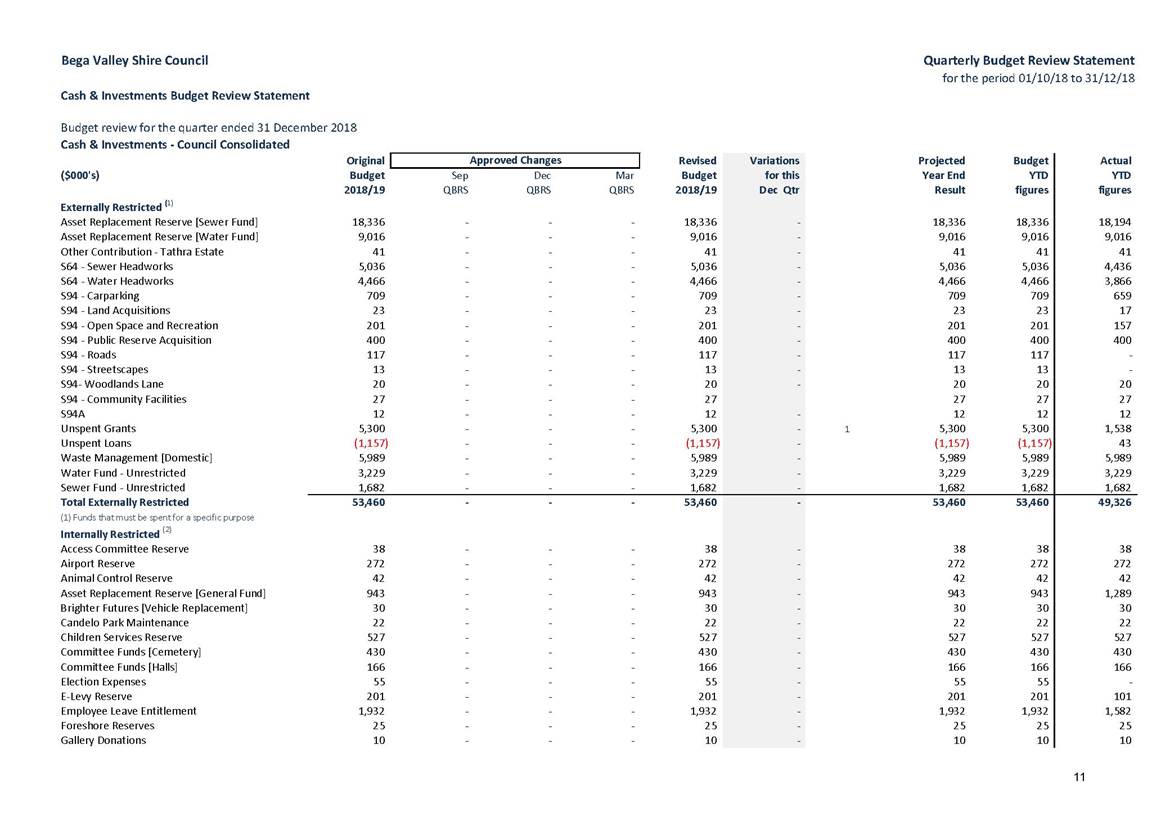

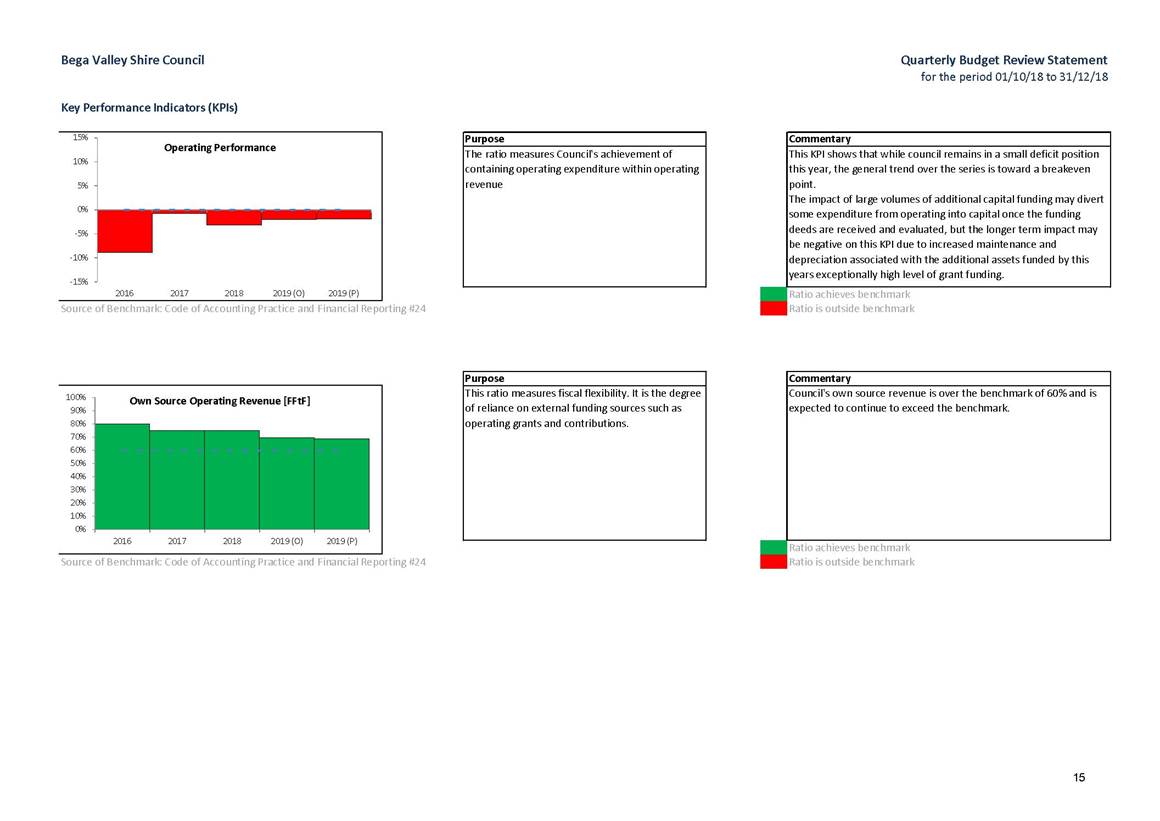

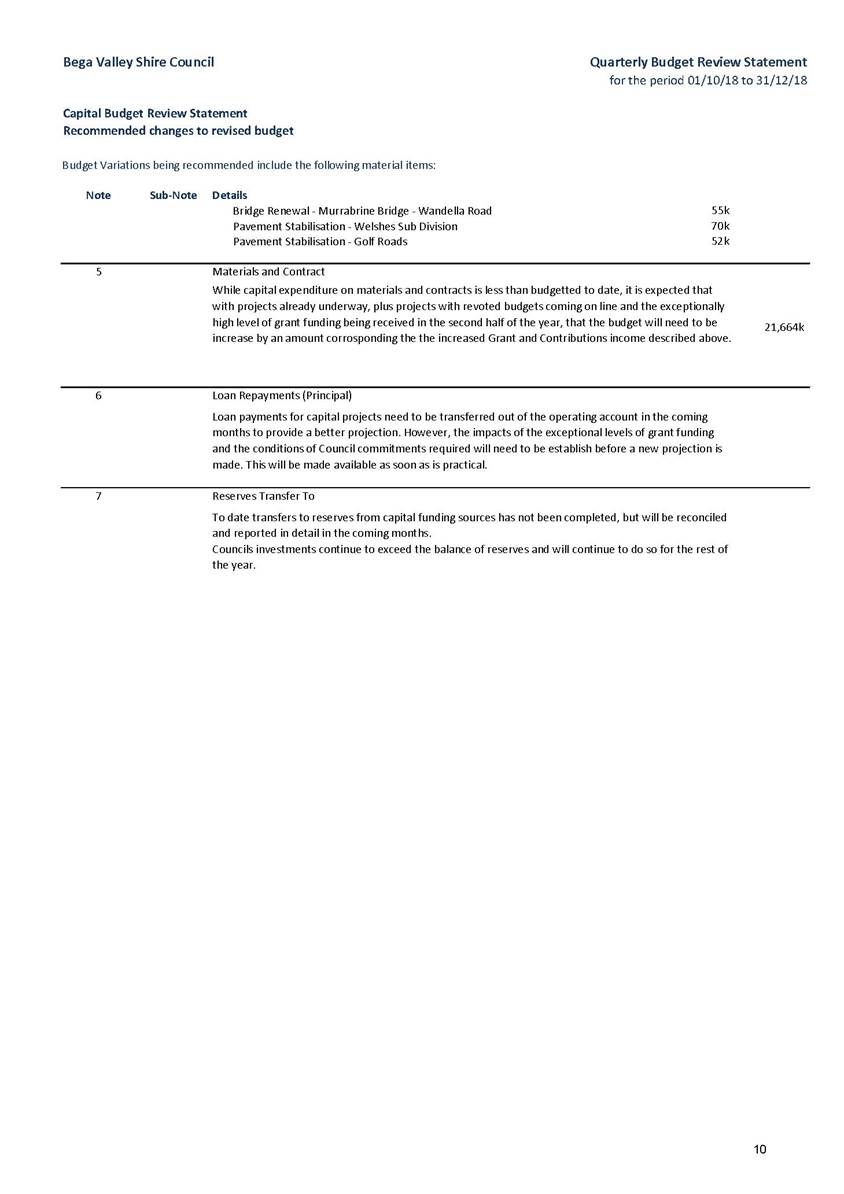

Council’s budgeted surplus has increased by $21,969,000. This is due mainly to additional grants and contributions for Capital projects, including revotes of $8,969,000 which results in a projected a surplus of $38,712,000 for the full year. However the Net operating result Before Capital Items has improved from a budgeted deficit of $1,709,000 to a projected deficit of $1,654,000, i.e. a movement of $55,000.

The main impact on Council’s projected year-end result relates to Council receiving additional grant funds from the Federal Government via the Financial Assistance Grant (FAG) which is expected to be maintained at the current level into the future and continue to have 50% paid in advance as was the case last year. Grants for Capital projects are also expected to be increased significantly since the original budget was prepared and adopted. However, the majority of this additional funding that can be recognised this financial year will be expended. Much of the additional funding will be recognised in subsequent years when the projects are likely to incur the majority of their expenditure. The receipt of these funds is likely to bring Investment Income back in line with the Original Budget.

Council continues to develop plans to better account for its assets, ensuring that when works are completed they are capitalised and depreciated appropriately. Work is underway to mature Council’s Asset Management Systems to provide for more accurate capturing and monitoring of assets, particularly in the area of Council staff costs being appropriately captured against capital projects. As a result, it is anticipated Council will be in a better position in the future to have more real time information to accurately forecast its maintenance and renewal costs.

Council has made some savings but continues to struggle under the current rate pegging in 2018-19 of 2.3%. Pleasingly this amount is set at 2.7% for the 2019-20 year.

While our projected result is approximately $0.250 million above the original budget, Council's normal operations are predominantly expected to be in line with the original expectations. The main areas of uncertainty are aligned with grant funding for capital works that continues to become available, but which is yet to be fully scoped to provide certainty in relation to the timing of expenditure and outcomes. This increase in capital funding will have negative impacts on future year’s maintenance and depreciation budgets. These are still to be fully assessed. Where funding is received for renewal works this is not as impacting.

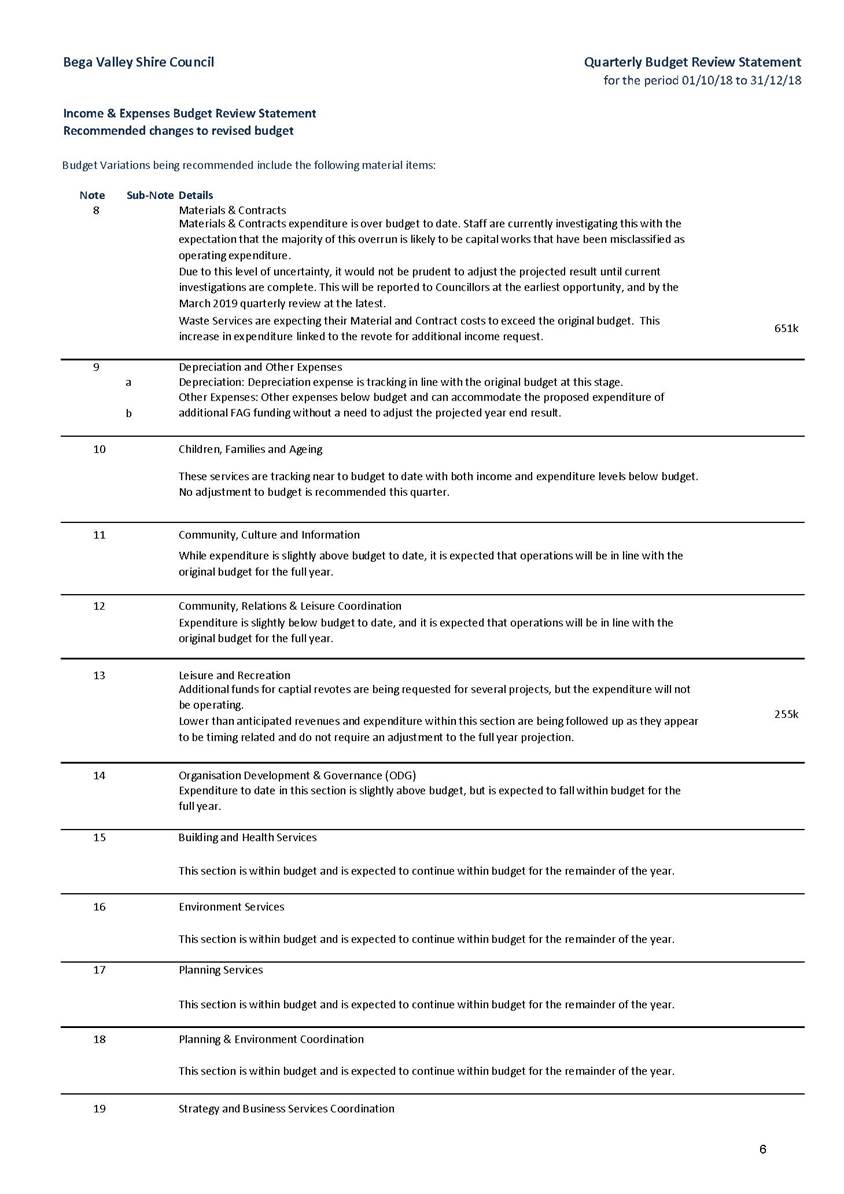

Council is currently in the process of working through the development of its draft Operational Plan and Budget for the 2019/20 financial year. Officers have identified the following items which will not be fully compete or which were funded in 2017/18 which will require funding allocations to be carried forward (revoted) to the current 2018/19 year.

|

Leisure & Recreation projects |

$ 255,000 |

|

Waste Services projects |

$2,895,000 |

|

Water Supplies projects |

$3,300,000 |

|

Sewer Services projects |

$1,132,000 |

|

Transport Services projects |

$1,332,000 |

|

Community Environment and Planning program |

$ 55,000 |

|

Total Revotes |

$8,969,000 |

The 31 March 2019 Quarterly Budget Review will include a list of projects that will be expected to require revotes for the 2019/20 year.

Legal /Policy

In accordance with Regulation 203(1) of the Local Government (General) Regulation 2005, the Responsible Accounting Officer must prepare and submit to the Council a Budget Review Statement after the end of each quarter.

As noted above, this requirement was not met for the September 2018 quarter due mainly to the focus on the end of year financial work where an extension due to extenuating circumstances was granted and exacerbated due to loss of key staff and delays in recruitment. The Office of Local Government is aware of this situation and staff are currently working to provide the outstanding information as soon as is practical.

Clause 203 of the Local Government (General) Regulations 2005 states:

Budget Review Statements and revision of estimates

1. Not later than two months after the end of each quarter (except the June quarter), the responsible accounting officer of a council must prepare and submit to the council a budget review statement that shows, by reference to the estimate of income and expenditure set out in the statement of the council’s revenue policy included in the operational plan for the relevant year, a revised estimate of the income and expenditure for that year.

2. A budget review statement must include or be accompanied by:

a. A report as to whether or not the responsible accounting officer believes that the statement indicates that the financial position of the council is satisfactory, having regard to the original estimate of income and expenditure, and

b. If that position is unsatisfactory, recommendations for remedial action.

c. A budget review statement must also include any information required by the Code to be included in such a statement.

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

Council’s 2017–2021 Delivery Program and 2018 -2019 Operational Plan provides the Financial Estimates 2017–2021 which includes the Budget for 2018-19.

Council will need to be mindful that the Long Term Financial Plan, is not likely to have the same level of external grant funding, and an expansion of the current asset base will put pressure on future budgets through increased maintenance and depreciation costs.

Given the issues highlighted by Council in achieving its Asset Management model, future gains or surpluses need to be placed into appropriate reserves in order to provide coverage for future liabilities.

Attachments

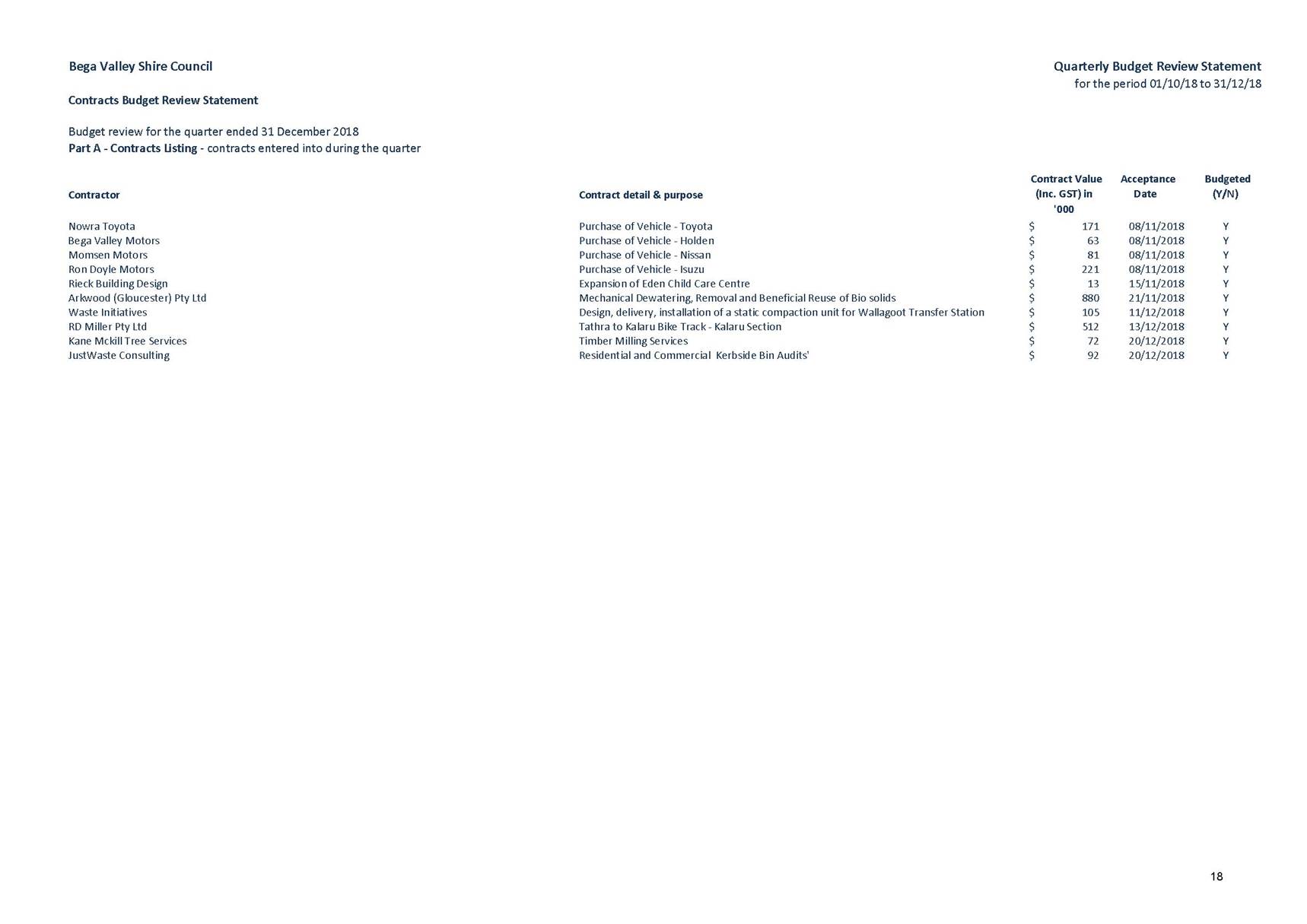

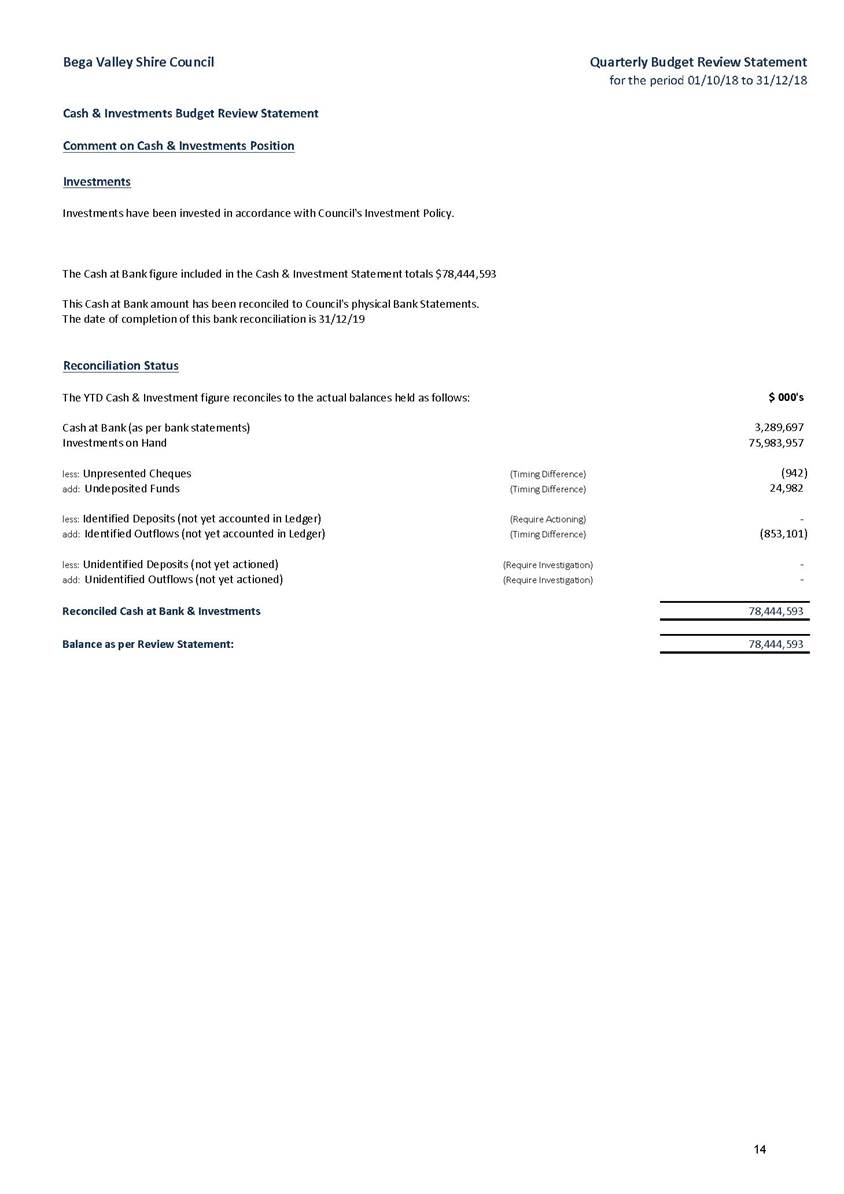

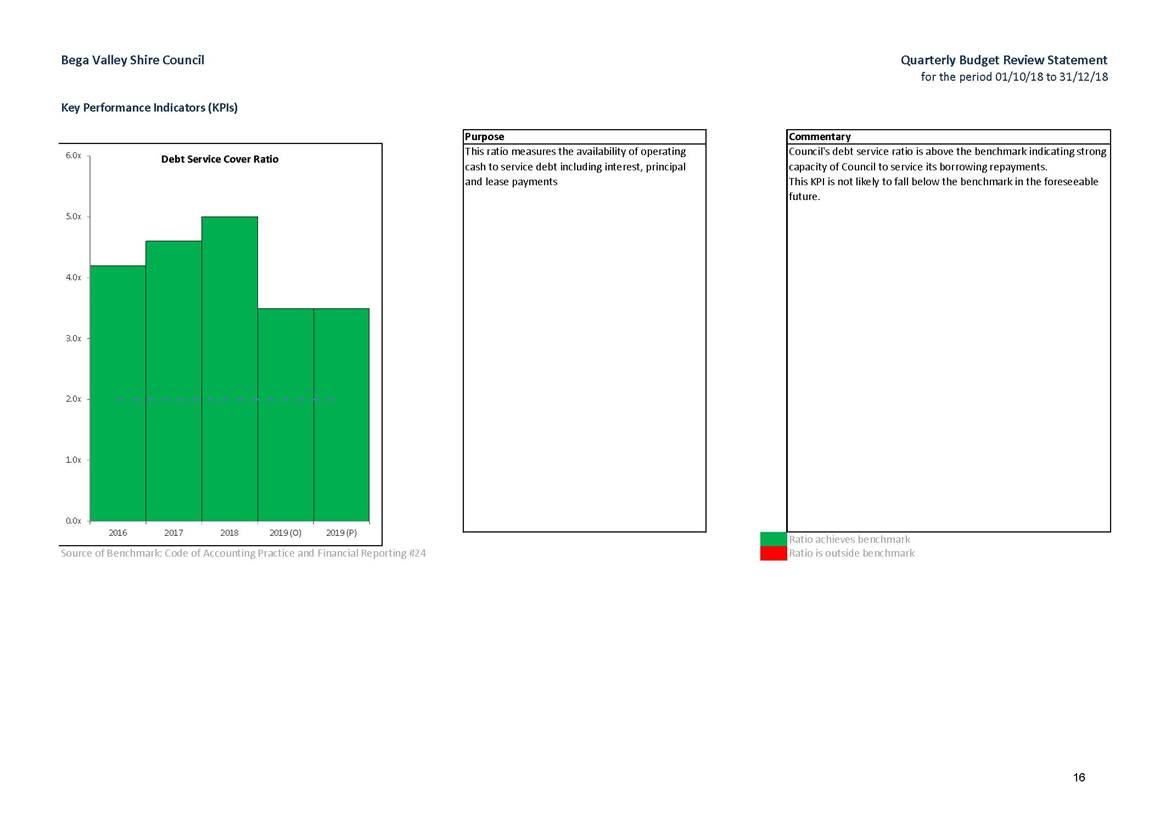

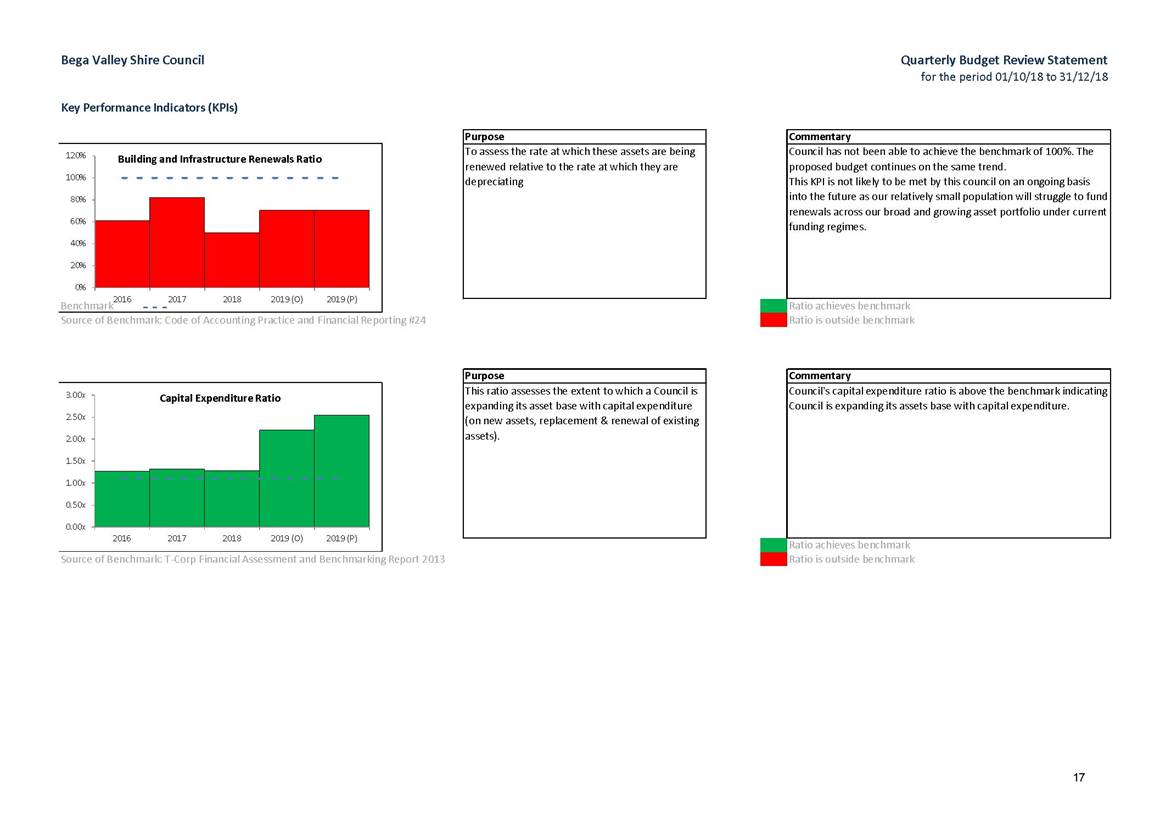

1⇩. Quarterly Budget Review Statement December 2018 2018-19 Financial Year

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |

|

Extraordinary Council |

27 February 2019 |

|

Item 4.1 - Attachment 1 |

Quarterly Budget Review Statement December 2018 2018-19 Financial Year |