|

ExtraordinaryMeeting Notice and Agenda

An Extraordinary Meeting of the Bega Valley Shire

Council will be held at Via Zoom on

|

|

ExtraordinaryMeeting Notice and Agenda

An Extraordinary Meeting of the Bega Valley Shire

Council will be held at Via Zoom on

|

Council meetings are recorded and live streamed to the Internet for public viewing. By entering the Chambers during an open session of Council, you consent to your attendance and participation being recorded.

The recording will be archived and made available on Council’s website www.begavalley.nsw.gov.au. All care is taken to maintain your privacy; however as a visitor of the public gallery, your presence may be recorded.

The Agendas for Council Meetings and Council Reports for each meeting will be available to the public on Council’s website as close as possible to 5.00 pm on the Thursday prior to each Ordinary Meeting. A hard copy is also made available at the Bega Administration Building reception desk and on the day of the meeting, in the Council Chambers.

The Minutes of Council Meetings are available on Council's Website as close as possible to 5.00 pm on the Monday after the Meeting.

1. Please be aware that the recommendations in the Council Meeting Agenda are recommendations to the Council for consideration. They are not the resolutions (decisions) of Council.

2. Background for reports is provided by staff to the General Manager for presentation to Council.

3. The Council may adopt these recommendations, amend the recommendations, determine a completely different course of action, or it may decline to pursue any course of action.

4. The decision of the Council becomes the resolution of the Council, and is recorded in the Minutes of that meeting.

5. The Minutes of each Council meeting are published in draft format, and are confirmed by Councillors, with amendments if necessary, at the next available Council Meeting.

If you require any further information or clarification regarding a report to Counci, please contact Council’s Executive Assistant who can provide you with the appropriate contact details

Phone (6499 2104) or email execassist@begavalley.nsw.gov.au.

· Is the decision or conduct legal?

· Is it consistent with Government policy, Council’s objectives and Code of Conduct?

· What will the outcome be for you, your colleagues, the Council, anyone else?

· Does it raise a conflict of interest?

· Do you stand to gain personally at public expense?

· Can the decision be justified in terms of public interest?

· Would it withstand public scrutiny?

A conflict of interest is a clash between private interest and public duty. There are two types of conflict:

· Pecuniary – regulated by the Local Government Act 1993 and Office of Local Government

· Non-pecuniary – regulated by Codes of Conduct and policy. ICAC, Ombudsman, Office of Local Government (advice only). If declaring a Non-Pecuniary Conflict of Interest, Councillors can choose to either disclose and vote, disclose and not vote or leave the Chamber.

· Is it likely I could be influenced by personal interest in carrying out my public duty?

· Would a fair and reasonable person believe I could be so influenced?

· Conflict of interest is closely tied to the layperson’s definition of ‘corruption’ – using public office for private gain.

· Important to consider public perceptions of whether you have a conflict of interest.

1st Do I have private interests affected by a matter I am officially involved in?

2nd Is my official role one of influence or perceived influence over the matter?

3rd Do my private interests conflict with my official role?

For more detailed definitions refer to Sections 442, 448 and 459 or the Local Government Act 1993 and Bega Valley Shire Council (and Model) Code of Conduct, Part 4 – conflictions of interest.

Whilst seeking advice is generally useful, the ultimate decision rests with the person concerned.Officers of the following agencies are available during office hours to discuss the obligations placed on Councillors, officers and community committee members by various pieces of legislation, regulation and codes.

|

Contact |

Phone |

|

Website |

|

Bega Valley Shire Council |

(02) 6499 2222 |

council@begavalley.nsw.gov.au |

www.begavalley.nsw.gov.au |

|

ICAC |

8281 5999 Toll Free 1800 463 909 |

icac@icac.nsw.gov.au |

www.icac.nsw.gov.au |

|

Office of Local Government |

(02) 4428 4100 |

olg@olg.nsw.gov.au |

http://www.olg.nsw.gov.au/ |

|

NSW Ombudsman |

(02) 8286 1000 Toll Free 1800 451 524 |

nswombo@ombo.nsw.gov.au |

Under the provisions of Section 451(1) of the Local Government Act 1993 (pecuniary interests) and Part 4 of the Model Code of Conduct prescribed by the Local Government (Discipline) Regulation (conflict of interests) it is necessary for you to disclose the nature of the interest when making a disclosure of a pecuniary interest or a non-pecuniary conflict of interest at a meeting.

The following form should be completed and handed to the General Manager as soon as practible once the interest is identified. Declarations are made at Item 3 of the Agenda: Declarations - Pecuniary, Non-Pecuniary and Political Donation Disclosures, and prior to each Item being discussed:

Council meeting held on __________(day) / ___________(month) /____________(year)

|

Item no & subject |

|

|

Pecuniary Interest

|

In my opinion, my interest is pecuniary and I am therefore required to take the action specified in section 451(2) of the Local Government Act 1993 and or any other action required by the Chief Executive Officer. |

|

Significant Non-pecuniary conflict of interest |

– In my opinion, my interest is non-pecuniary but significant. I am unable to remove the source of conflict. I am therefore required to treat the interest as if it were pecuniary and take the action specified in section 451(2) of the Local Government Act 1993. |

|

Non-pecuniary conflict of interest |

In my opinion, my interest is non-pecuniary and less than significant. I therefore make this declaration as I am required to do pursuant to clause 5.11 of Council’s Code of Conduct. However, I intend to continue to be involved with the matter. |

|

Nature of interest |

Be specific and include information such as : · The names of any person or organization with which you have a relationship · The nature of your relationship with the person or organization · The reason(s) why you consider the situation may (or may be perceived to) give rise to a conflict between your personal interests and your public duty as a Councillor. |

|

If Pecuniary |

Leave chamber |

|

If Non-pecuniary (tick one) |

Disclose & vote Disclose & not vote Leave chamber |

|

Reason for action proposed |

Clause 5.11 of Council’s Code of Conduct provides that if you determine that a non-pecuniary conflict of interest is less than significant and does not require further action, you must provide an explanation of why you consider that conflict does not require further action in the circumstances |

|

Print Name |

I disclose the above interest and acknowledge that I will take appropriate action as I have indicated above. |

|

Signed |

|

NB: Please complete a separate form for each Item on the Council Agenda on which you are declaring an interest.

|

Extraordinary Council |

13 July 2020 |

Pecuniary, Non-Pecuniary and Political Donation Disclosures to be declared and tabled.

3.1 Extraordinary Council Meeting 13 July 2020............................................................................... 8

4.1 Update on Quarterly Budget Review Statement - 31 March 2020....................................... 11

5.1 Independent review of financial statements............................................................................ 18

6.1 2019 Audited Financial Statements and 2020 March Quarterly Budget Review............... 22

6.2 March QBR Forecast - Unrestricted Cash.................................................................................. 24

Extraordinary Council |

13 July 2020 |

3.1 Extraordinary Council Meeting 13 July 2020........................................................ 8

|

Extraordinary Council 13 July 2020 |

Item 3.1 |

3.1. Extraordinary Council Meeting 13 July 2020

A formal request was received under clause 3.3 of the Code of Meeting Practice for an Extraordinary Council Meeting

General Manager

That Council note the request for an Extraordinary Meeting and the notification and scheduling of this meeting meet the requirements of the Code of Meeting Practice.

Executive Summary

On Tuesday 30 June 2020 the Mayor received a request, in line with the requirements of the Council’s Code of Meeting Practice, for an Extraordinary Meeting. This meeting was then scheduled in line with available resourcing and the requirements of clause 3.3 of the Code of Meeting Practice.

Background

Crs Nadin and Bain submitted a request for an Extraordinary Meeting on 30 June 2020:

Pursuant with section 3.3 in Bega Valley Shire Council’s Code of Meeting Practice, Councillor Robyn Bain and I request council hold an extra ordinary meeting “as soon as is practicable”, but ideally on Wednesday July 8, 2020, to urgently consider the following business:

“That Council obtain, as a matter of urgency, an independent assessment of Council’s present financial position (as at 30/6/20) prior to final annual audit so as to ground-truth a sound future financial commitment in its Long Term Financial Plan, Resourcing Strategy, Delivery and Operational plan for 20/21 financial year (now commenced).

That the assessment include expenditure of all restricted and unrestricted funds and involve where necessary, a forensic audit for financial years 2017, 2018, 2019 and 2020.”

Madam Mayor, it has become clear the figures in council’s financial statement appear to show inconsistencies to the cash flow of externally restricted funds, internally restricted funds and unrestricted funds, resulting from a comparison between the 2018/ 19 audit and the budget predictions and expenditure in the quarterly reports for the 19/20 financial year.

Given the fact that council’s draft budget is currently on public exhibition, with expected continuing deficits in coming years and proposals to apply for a special rate increase, it is in the public interest to ground-truth Council’s actual current financial position in all funds and investment accounts as a matter of urgency.

It is important the public and councillors can have confidence in Council’s handling of public finances, and we believe the only way for this to occur is to conduct an independent investigation into Council’s finances.

We trust you see the urgency of this issue and will act quickly to ensure this matter is brought to a head as soon as possible.”

Processes were immediately put in place to establish a date and put in place the process to meet requirements of the Code of Meeting Practice. The date nominated by the two Councillors was unable to be achieved due to support staffing availability with school holiday plans already approved and in place. The closest date to the date requested was identified.

The Councillors were then asked to specifically outline the resolution to be considered. Staff also brought forward the answers to Questions Without Notice asked at the last meeting by Crs Nadin and Bain to inform the consideration.

Legal /Policy

The Council’s adopted Code of Meeting Practice is based on the NSW Model Code of Meeting Practice for Local Councils in NSW made under section 360 of the Local Government Act 1993.

Clause 3.3 of the Code of Meeting Practice cover this request. Two Councillors are required to request an Extraordinary Meeting, and the meeting should be held as soon as is practicable, nut in any event, no more than 14 days after receipt of the request.

Attachments

Nil

|

Extraordinary Council |

13 July 2020 |

4.1 Update on Quarterly Budget Review Statement - 31 March 2020..................... 11

|

Item 4.1 |

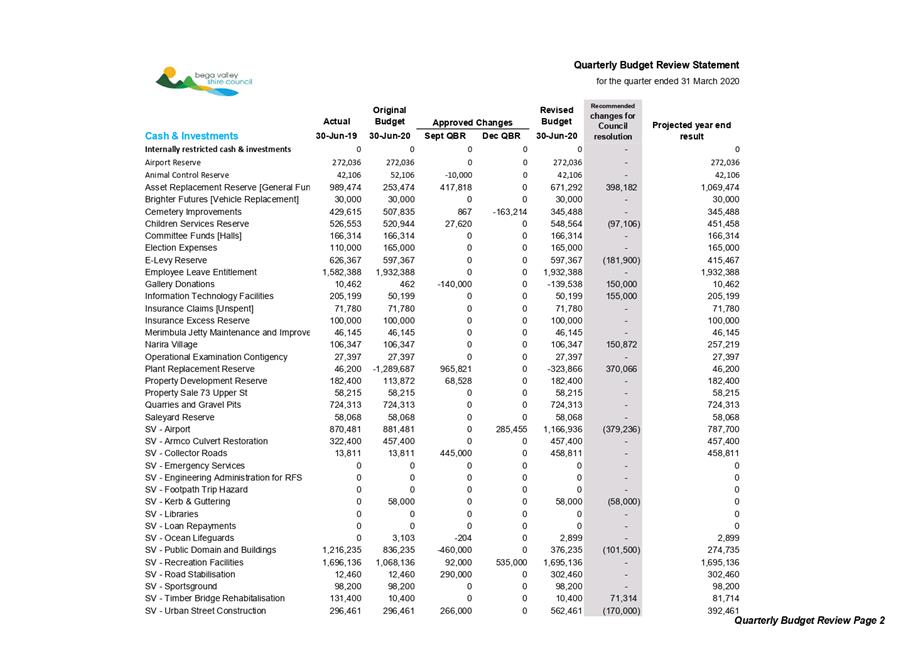

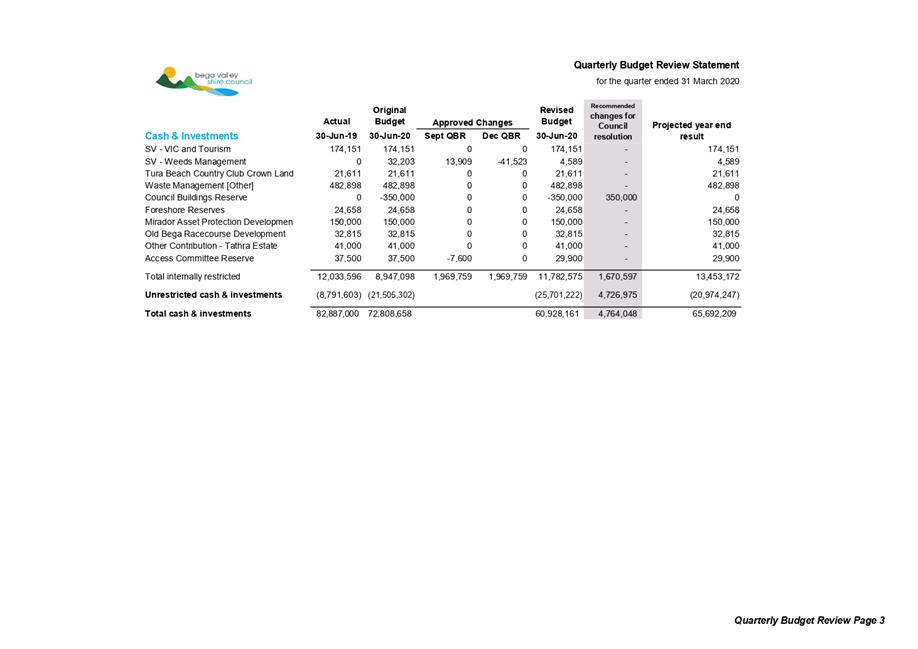

Quarterly Budget Review Statements (QBRS) are prepared and presented to Council in accordance with Section 203 of the Local Government (General) Regulation 2005.

Director Business & Governance

1. That Council receive and note the updated pages for the March 2020 Quarterly Budget Review Statement (QBRS) attached and;

2. That Council note the administrative correction relates to the information contained in the ‘Actual 30-Jun-19’ column of the Cash and Investments sheet included in the March QBRS and;

3. That the correction be adopted as presented and included in future reporting for FY2020

Executive Summary

Under the Integrated Planning and Reporting (IPR) Guidelines, a Quarterly Budget Review Statement (QBRS) must be presented to Council for each financial quarter.

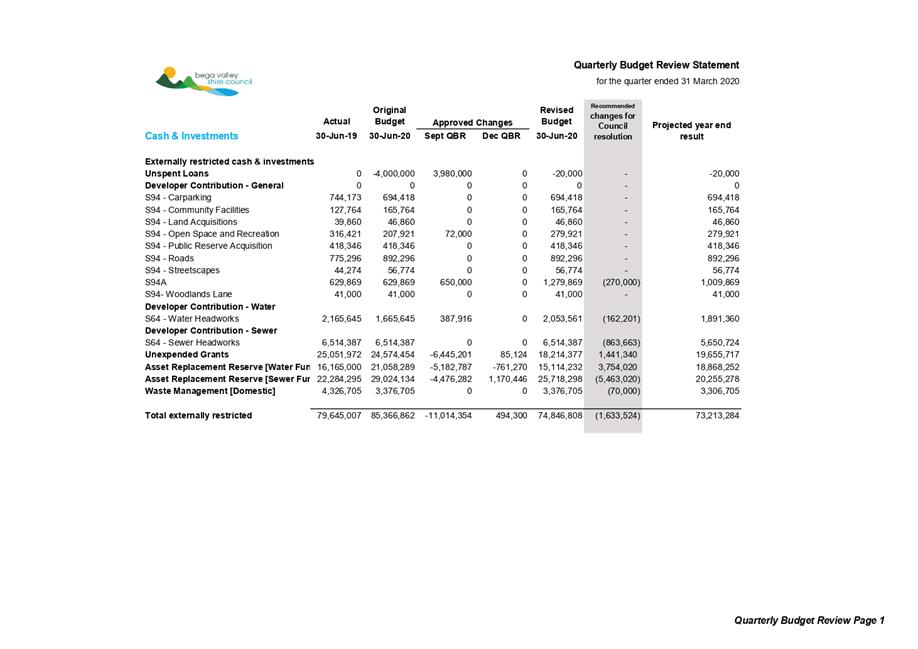

The QBRS is presented in a summary format. During the month of June, it was found that there was an administrative error in the ‘Actual 30-Jun-19’ column of the Cash and Investment Sheet contained in QBRS. This report seeks to correct the record and update the March QBRS Cash and Investment sheet to reflect the externally audited 2019 Financial Statement results.

Financial and resource considerations

Cash and Investments

Council had cash and investments of $82,887k at 30 June 2019, the revised projected cash figure at the 30 June 2020 is expected to be $65,692k. The impact of this report does not see these figures change.

It is noted that this correction will not see an alignment between the reported ending balances in FY2019 Financial Statements for internal restricted reserves. As part of the finalisation of the FY2019 Financial Statements Council were required to reduce its internal restrictions with insufficient cash to support the level of documented restrictions. These internal restrictions are still recorded in the cash and investment sheet prepared for the March QBRS which provides the current information; the intent is for council to formally review its internal restrictions to inform the FY2020 Financial Statements.

Legal /Policy

In accordance with Regulation 203(1) of the Local Government (General) Regulation 2005, the Responsible Accounting Officer must prepare and submit to the Council a Budget Review Statement after the end of each quarter.

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

Council’s 2017–2021 Delivery Program and 2019-2020 Operational Plan provides the Financial Estimates 2017–2021 which includes the Budget for FY2020.

1⇩. Updated March QBRS - Cash and Investments

|

Extraordinary Council |

13 July 2020 |

|

Item 4.1 - Attachment 1 |

Updated March QBRS - Cash and Investments |

|

Extraordinary Council |

13 July 2020 |

Notices of Motion

13 July 2020

5.1 Independent review of financial statements...................................................... 18

|

Extraordinary Council 13 July 2020 |

Item 5.1 |

1. That Council commission, as a matter of urgency, a contractor to provide an independent forensic audit of Council’s present financial position (as at 30/6/20) prior to the final annual audit 31/10/2020 but as soon as possible so as to ground-truth a sound future financial commitment in its Long Term Financial Plan, Resourcing Strategy, Delivery and Operational plan for 20/21 financial year (now commenced).

2. That the audit identify expenditure from all restricted and unrestricted funds and include the financial years 2017, 2018, 2019 and 2020.

3 That Council call for tenders for the appointment of the external contractor and that a subsequent report be presented to Council to appoint the firm to carry out the work.

4. That council exclude tenders from companies outside NSW, companies in the Bega Valley Shire or the accounting firm Deloittes and the NSW Audit Office/Auditor General that audited Council’s financial statements and therefore has a conflict of interest.

5. That the independent investigation and audit of Council's present financial position be funded by an initial contribution of $50,000 from General Manager’s legal allocation noting that additional allocation may need to be identified following the tender process.

Staff have now confirmed that a large number of figures in Council’s recent March quarterly budget review are incorrect. This includes figures from the externally restricted account and also the unrestricted account, many of which staff now recommend Councillors change. It’s worth noting the recommended changes in and of themselves are alarming.

These recommended changes follow questions without notice from Crs Nadin and Bain, who identified inconsistencies to the cash flow of externally restricted funds, internally restricted funds and unrestricted funds, resulting from a comparison between the 2019 Audited Financial Statements and the March QBR.

Given the fact that Council’s draft budget is currently on public exhibition, with expected continuing deficits in coming years and proposals to apply for a special rate increase, it is in the public interest to ground-truth Council’s actual current financial position in all funds and investment accounts as a matter of urgency.

It is important the public and councillors have confidence in Council’s handling of public finances, and we believe the only way for this to occur is to conduct an independent investigation into Council’s finances.

As this is work is needed prior to the annual audit for the 2019/20 year due to be considered by Council in November 2020 external parties need to be engaged to cover both aspects of this work. This work should be funded by allocating funds currently directed to investigations in the 2020/21 draft budget to engage the external contractor. A tender process should be undertaken and a report presented to Council as soon as possible so Councillors can appoint the independent audit company.

Cr Mitchell Nadin

Councillors are referred to the answers to Questions Without Notice:

Recording the Financial Statements, externally and internally restricted reserves results, is a process usually undertaken in the Quarterly Budget Review templates when they are finalised; however this was missed when preparing the March 2020 QBRS.

The inconsistency is an administration error in preparing the QBRS report.

The March QBRS Cash and Investment sheet has been updated to reflect the 2019 Financial Statement results and will be presented to Council for formal adoption to correct the administrative error. This will not see an alignment between the reported ending balances in FY2019 Financial Statements for internal restricted reserves for the reason stated below.

As part of the finalisation of the FY2019 Financial Statements Council were required to reduce its internal restrictions as there was insufficient cash to support the level of documented restrictions. These internal restrictions are still recorded in the cash and investment sheet prepared for the March QBRS which provides the current information; the intent is for Council to formally review its internal restrictions to inform the FY2020 Financial Statements.

Cr Bain question response:

The question from Cr Bain relates to cash balances at 30 June 2019 and the reported performance expected at 30 June 2020 recorded in the March Quarterly Budget Review Statement (QBRS).

A review of the QBRS presented on 27 May 2020 has found an administrative error in the QBRS report, which staff are recommending be corrected.

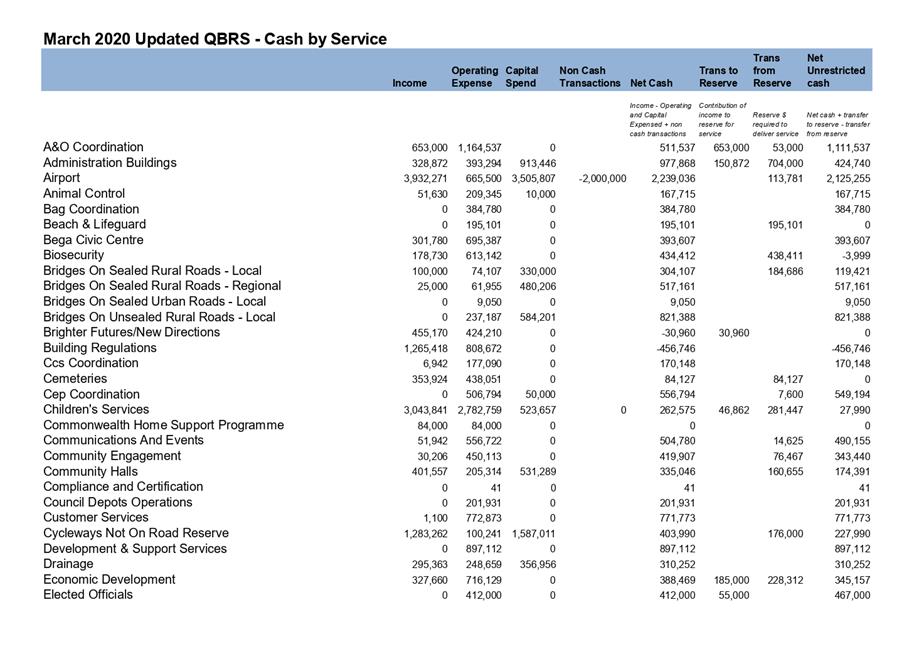

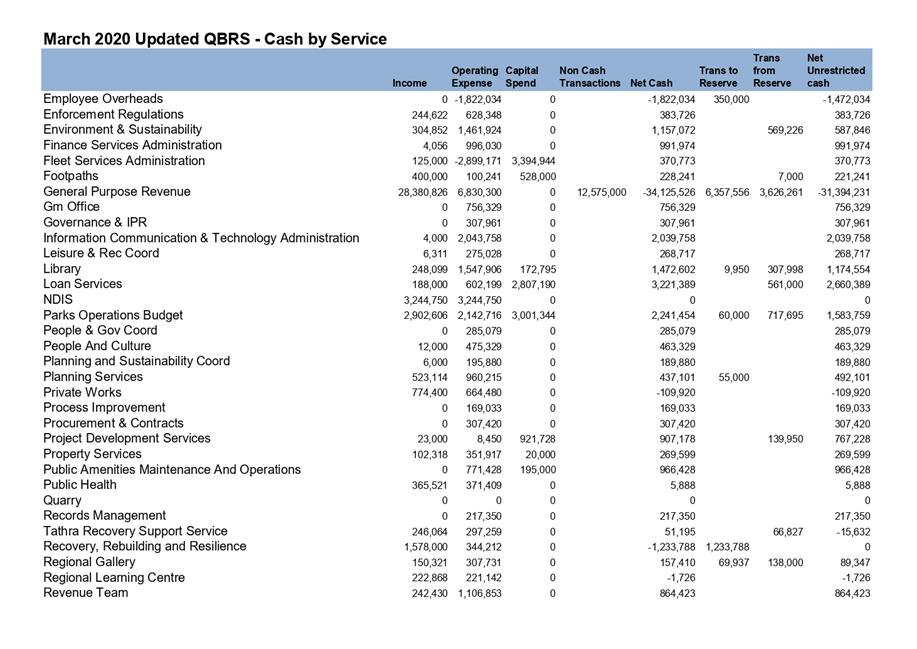

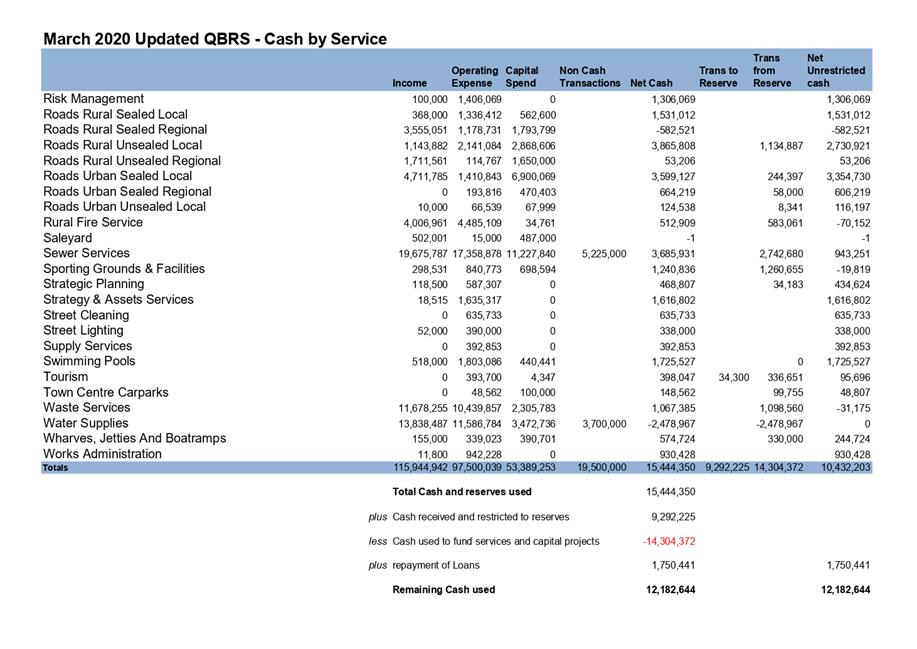

The interpretation by staff of the Question Without Notice from Cr Bain is for us to provide clarity on the amount of unrestricted cash and investments allocated to deliver services during FY2020. Therefore, the attached report is similar to the table included in the Draft 2021 Operational Plan with additional columns of data showing the projected cash resources required by all services. The attachment is for FY2020 and reflects the expected income, expenses and capital costs at 30 June 2020.

It is noted that in the corrected March QBRS, the actual performance of Cash and Investments at 30 June 2019 in the unrestricted reserve is $(8,791,603), meaning, for accounting purposes, the unrestricted cash held has been allocated to fund services and projects identified in the internally restricted reserve for financial year 2020. The expected unrestricted cash used to deliver all services for FY2020 is $12,182,644.

When recording total cash, cash equivalents and investments, as part of the finalisation of the 2019 Financial Statements* Council were required to reduce its internal restrictions as there was insufficient cash to support the level of restrictions. These internal restrictions are still recorded in the cash and investment sheet prepared for the March QBRS to provide the current information; the intent is for Council to formally review its internal restrictions before preparing the FY2020 Financial Statements.

*Note 6(c) of the Financial Statements

Nil

|

Extraordinary Council |

13 July 2020 |

Questions with Notice

13 July 2020

6.1 2019 Audited Financial Statements and 2020 March Quarterly Budget Review 22

6.2 March QBR Forecast - Unrestricted Cash............................................................ 24

|

Extraordinary Council 13 July 2020 |

Item 6.1 |

6.1. 2019 Audited Financial Statements and 2020 March Quarterly Budget Review

On 24 June 2020 Councillor Nadin asked: “on page 18 of Council’s recently adopted March quarterly budget review, it states Council started this current financial year on July 1, 2019 with a cash position of $82,887,000 broken into three areas: $57,850,632 in externally restricted funds, $12,033,596 in internally restricted funds, and $13,002,772 in unrestricted cash. However, these figures from the QBR are apparently at odds with the 2019 financial statements (adopted in April), which on page 27 states that as of June 30, 2019 Council had the same gross cash amount of $82,887,000, but reported $79,644,000 in externally restricted cash, $3,243,000 in internally restricted cash, and zero unrestricted cash. Can you explain this apparent discrepancy and confirm which of these figures is correct; and can you confirm if any externally restricted cash has been transferred into Council’s internally restricted or unrestricted cash holdings.

Cr Nadin

Staff Response

Cr Nadin Statement: On page 18 of Council’s recently adopted March quarterly budget review, it states Council started this current financial year on July 1, 2019 with a cash position of $82,887,000 broken into three areas: $57,850,632 in externally restricted funds, $12,033,596 in internally restricted funds, and $13,002,772 in unrestricted cash.

However, these figures from the QBR are apparently at odds with the 2019 financial statements (adopted in April), which on page 27 states that as of June 30, 2019 Council had the same gross cash amount of $82,887,000, but reported $79,644,000 in externally restricted cash, $3,243,000 in internally restricted cash, and zero unrestricted cash.

Question: Can you explain this apparent discrepancy and confirm which of these figures is correct; and can you confirm if any externally restricted cash has been transferred into Council’s internally restricted or unrestricted cash holdings.

Council staff have reviewed its March QBRS and are aware that there are discrepancies between the 2019 Financial Statements the figures in the cash and investments sheet provided in the March QBRS on 27 May 2020. Council’s cash position remains unchanged.

Recording the Financial Statements, externally and internally restricted reserves results, is a process usually undertaken in the Quarterly Budget Review templates when they are finalised; however this was missed when preparing the March 2020 QBRS.

Council confirms that no transfer has occurred within its financial ledgers. The inconsistency is an administration error in preparing the QBRS report.

The March QBRS Cash and Investment sheet has been updated to reflect the 2019 Financial Statement results and will be presented to Council for formal adoption to correct the administrative error. This will not see an alignment between the reported ending balances in FY2019 Financial Statements for internal restricted reserves for the reason stated below.

As part of the finalisation of the FY2019 Financial Statements Council were required to reduce its internal restrictions as there was insufficient cash to support the level of documented restrictions. These internal restrictions are still recorded in the cash and investment sheet prepared for the March QBRS which provides the current information; the intent is for Council to formally review its internal restrictions to inform the FY2020 Financial Statements.

Attachments

Nil

|

Extraordinary Council 13 July 2020 |

Item 6.2 |

6.2. March QBR Forecast - Unrestricted Cash

On 24 June 2020 Councillor Bain asked ”the March QBR forecast will have $552,702.00 in its unrestricted cash reserve by next Tuesday. That means Council will have spent more than $12 million from the $13,002,772, Council reportedly had in its unrestricted reserve at the beginning of this financial year. Can you please provide detail or a statement of all income and expenditure of Councils unrestricted cash reserve. “

Cr Bain

Staff Response

Question: “Can you please provide detail or a statement of all income and expenditure of Councils unrestricted cash reserve”.

The question from Cr Bain relates to cash balances at 30 June 2019 and the reported performance expected at 30 June 2020 recorded in the March Quarterly Budget Review Statement (QBRS). A review of the QBRS presented on 27 May 2020 has found an administrative error in the QBRS report, which staff are recommending be corrected.

The interpretation by staff of the Question Without Notice from Cr Bain is for us to provide clarity on the amount of unrestricted cash and investments allocated to deliver services during FY2020. Therefore, the attached report is similar to the table included in the Draft 2021 Operational Plan with additional columns of data showing the projected cash resources required by all services. The attachment is for FY2020 and reflects the expected income, expenses and capital costs at 30 June 2020.

It is noted that in the corrected March QBRS, the actual performance of Cash and Investments at 30 June 2019 in the unrestricted reserve is $(8,791,603), meaning, for accounting purposes, the unrestricted cash held has been allocated to fund services and projects identified in the internally restricted reserve for financial year 2020. The expected unrestricted cash used to deliver all services for FY2020 is $12,182,644.

When recording total cash, cash equivalents and investments, as part of the finalisation of the 2019 Financial Statements* Council were required to reduce its internal restrictions as there was insufficient cash to support the level of restrictions. These internal restrictions are still recorded in the cash and investment sheet prepared for the March QBRS to provide the current information; the intent is for Council to formally review its internal restrictions before preparing the FY2020 Financial Statements.

*Note 6(c) of the Financial Statements

Attachments 1⇩. QBRS March 2020 - Cash by Service