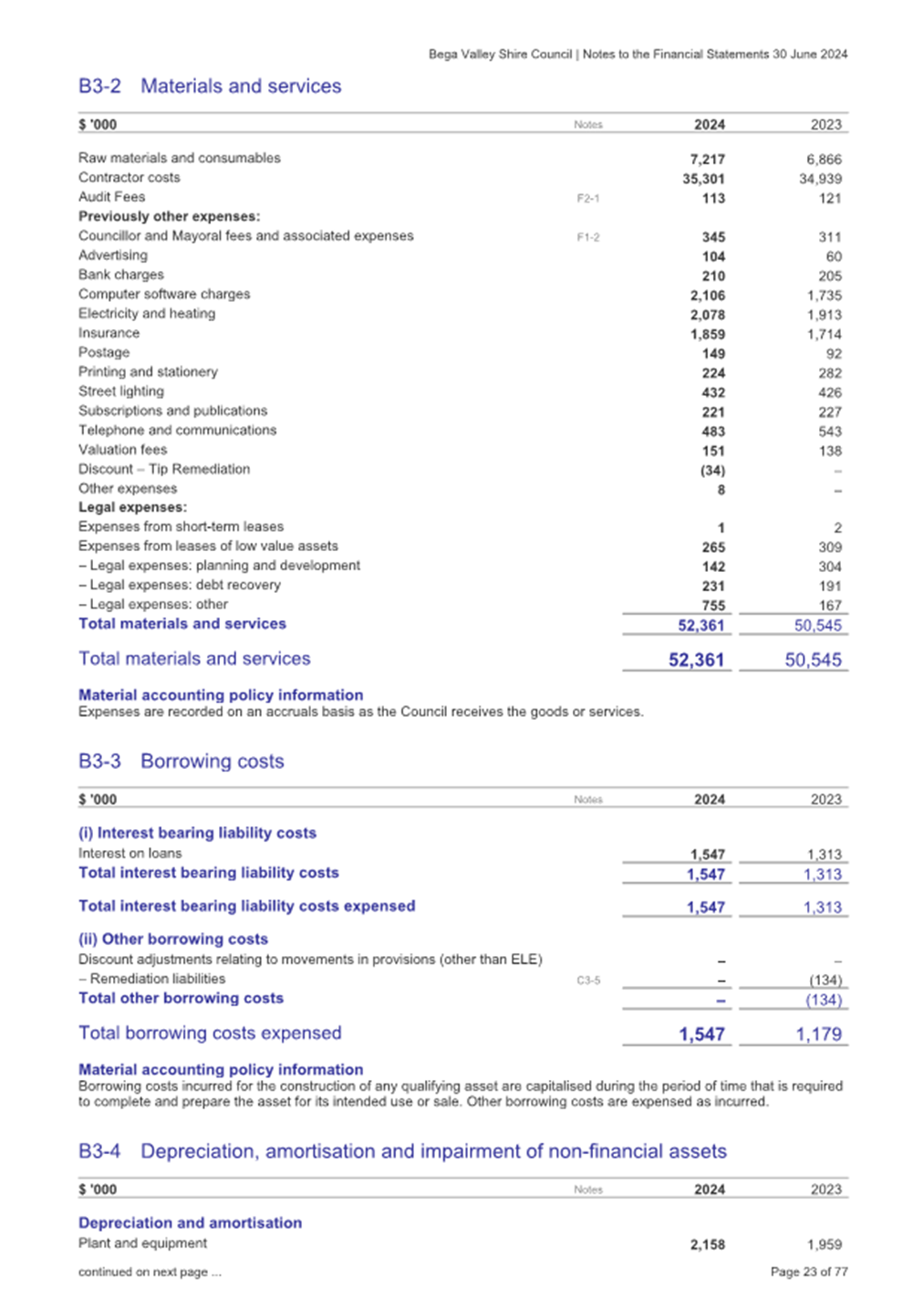

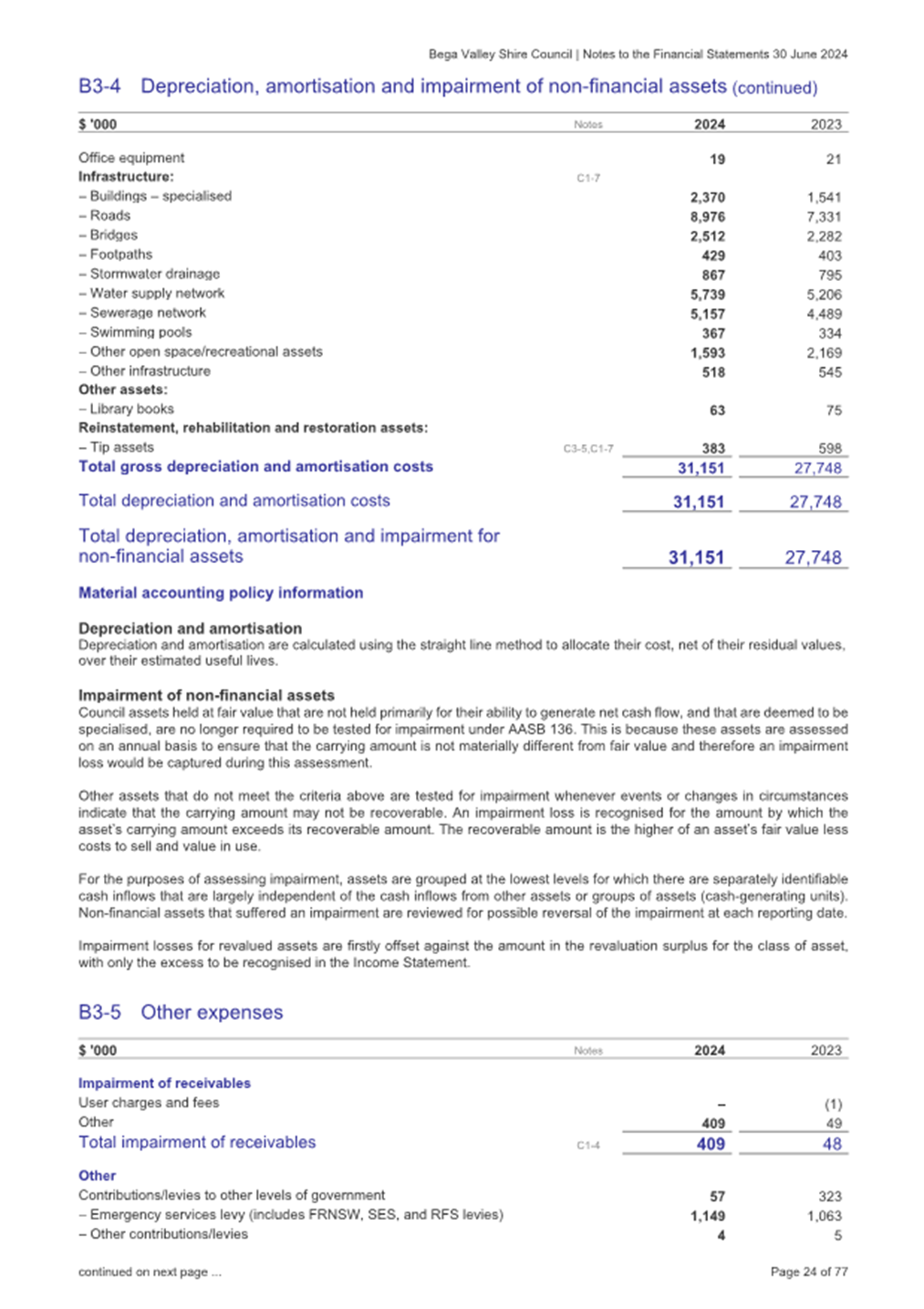

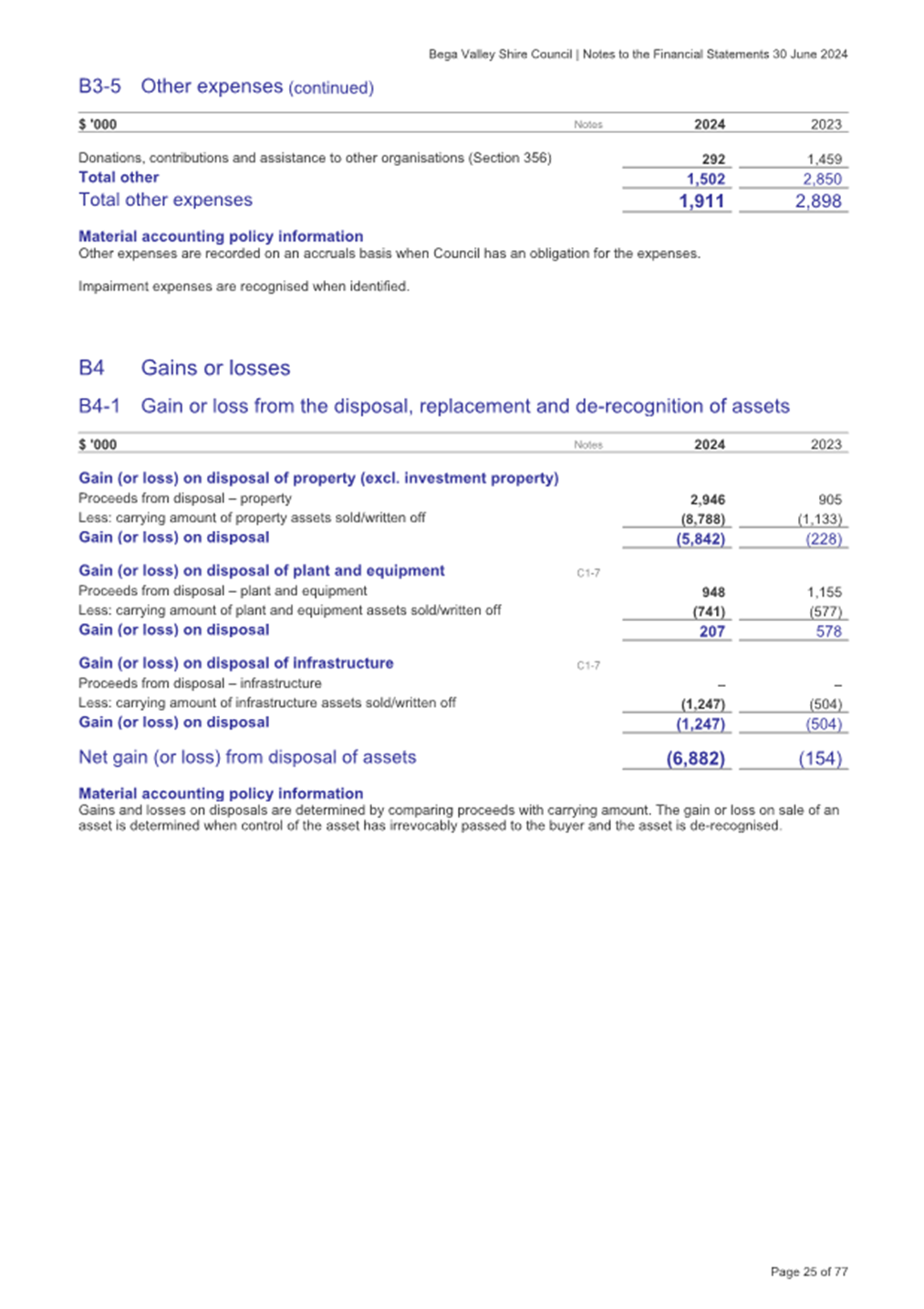

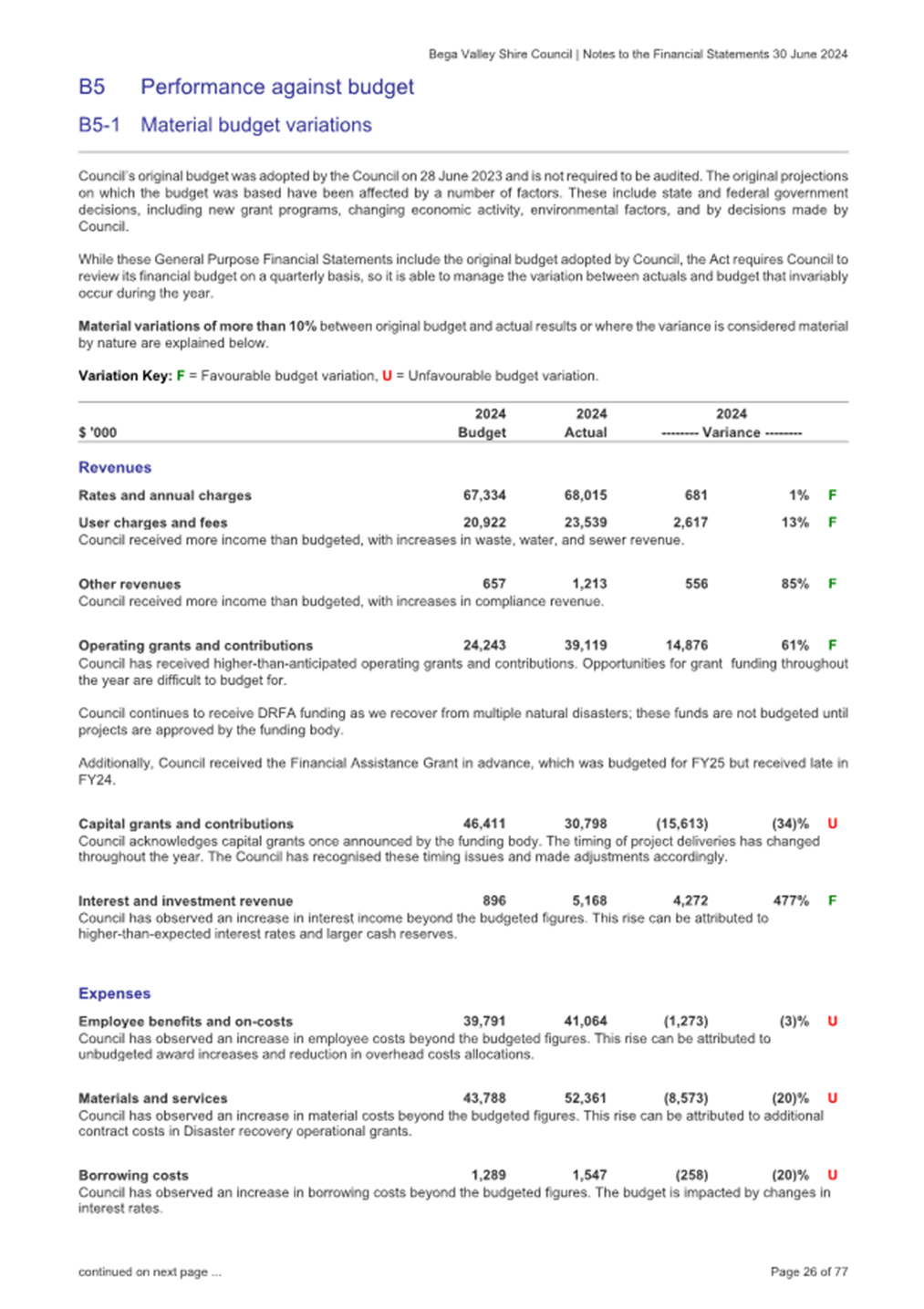

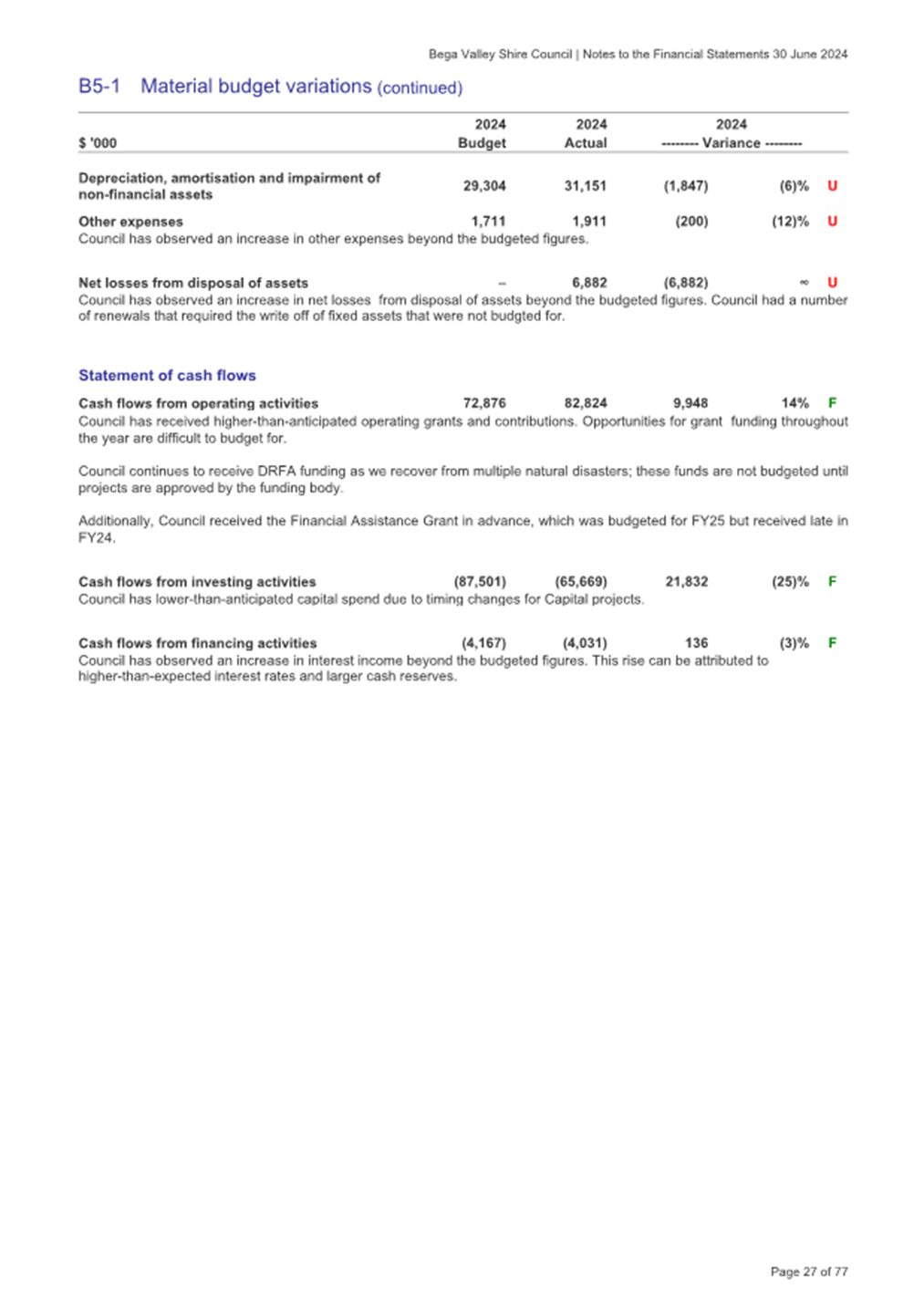

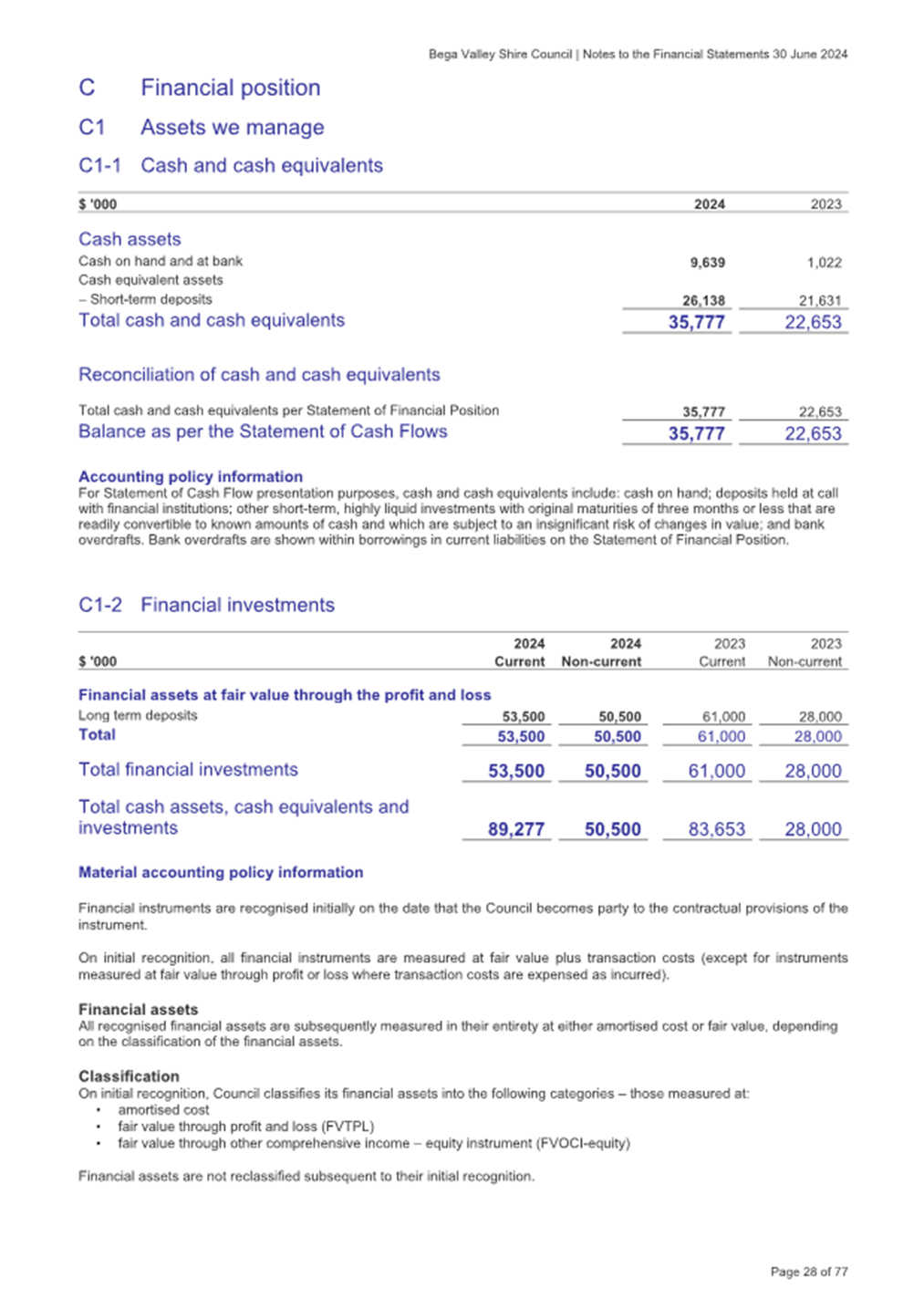

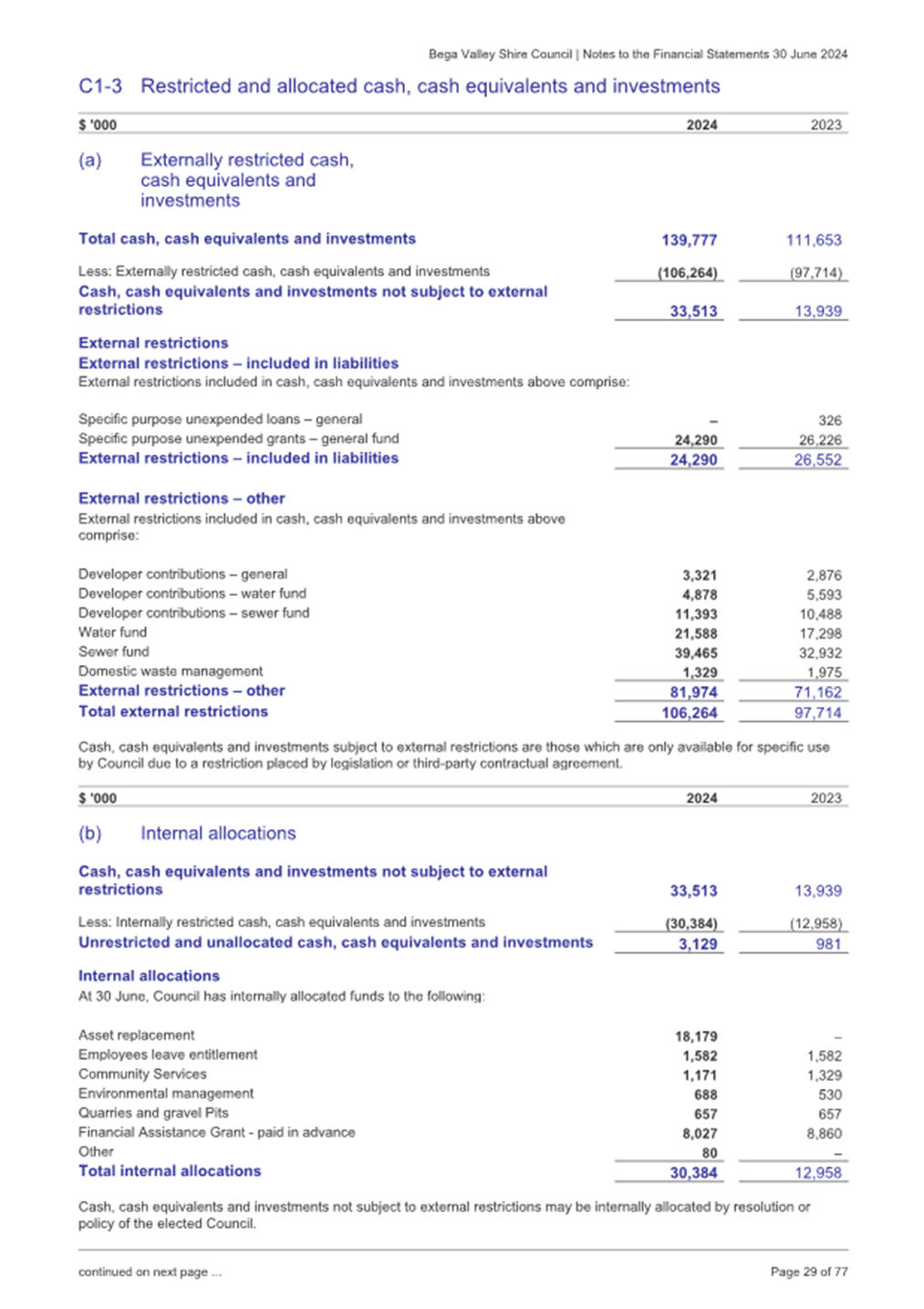

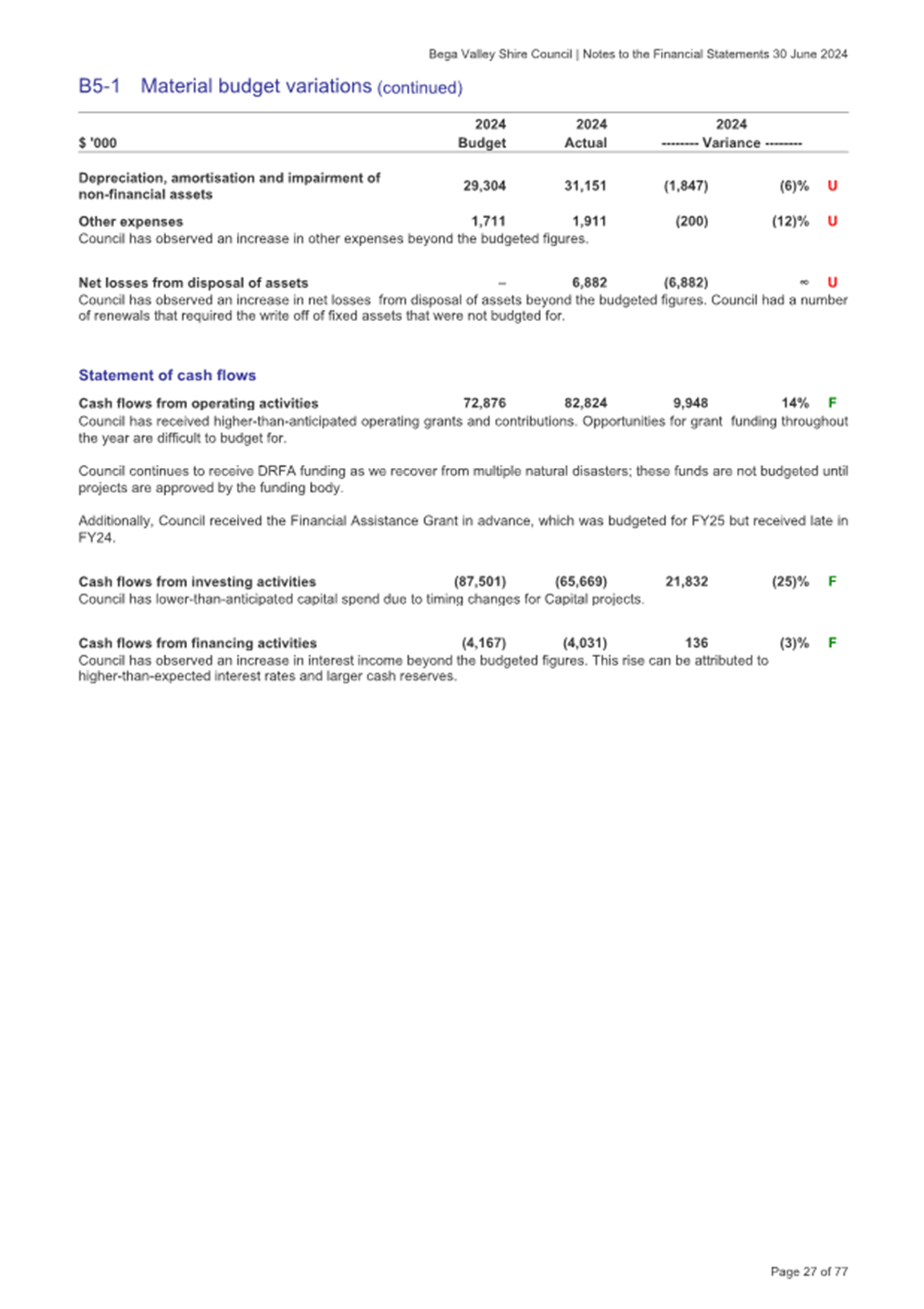

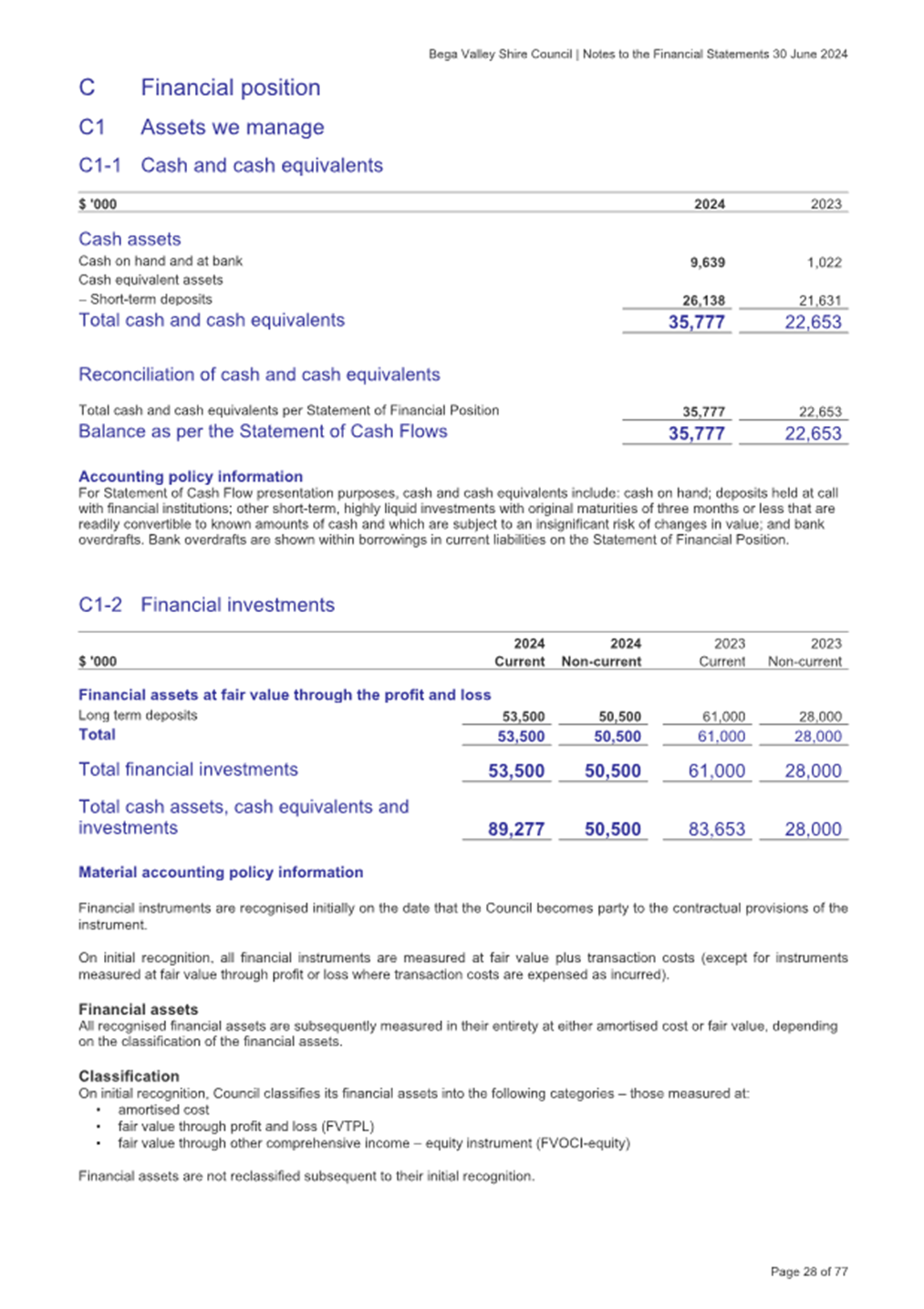

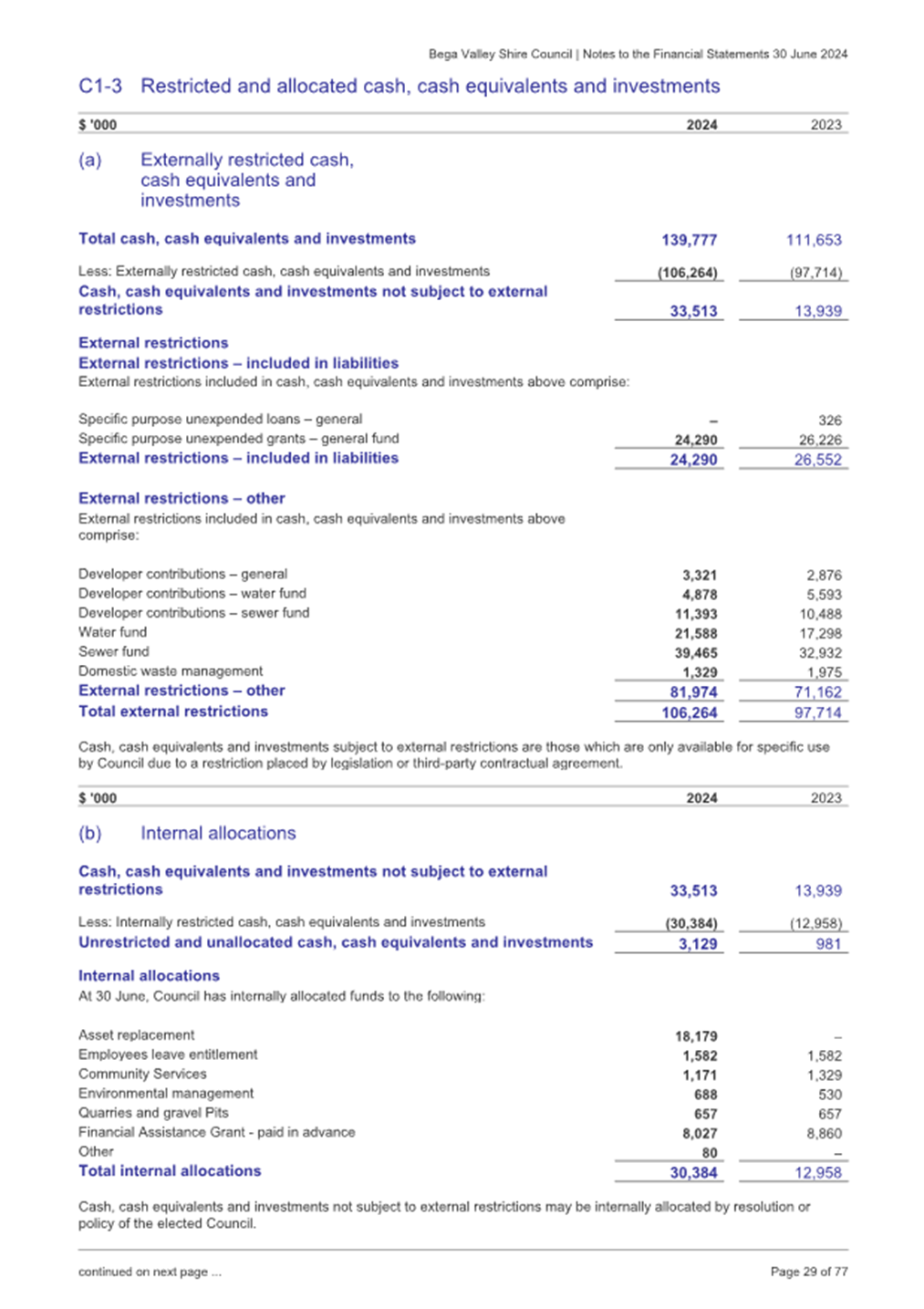

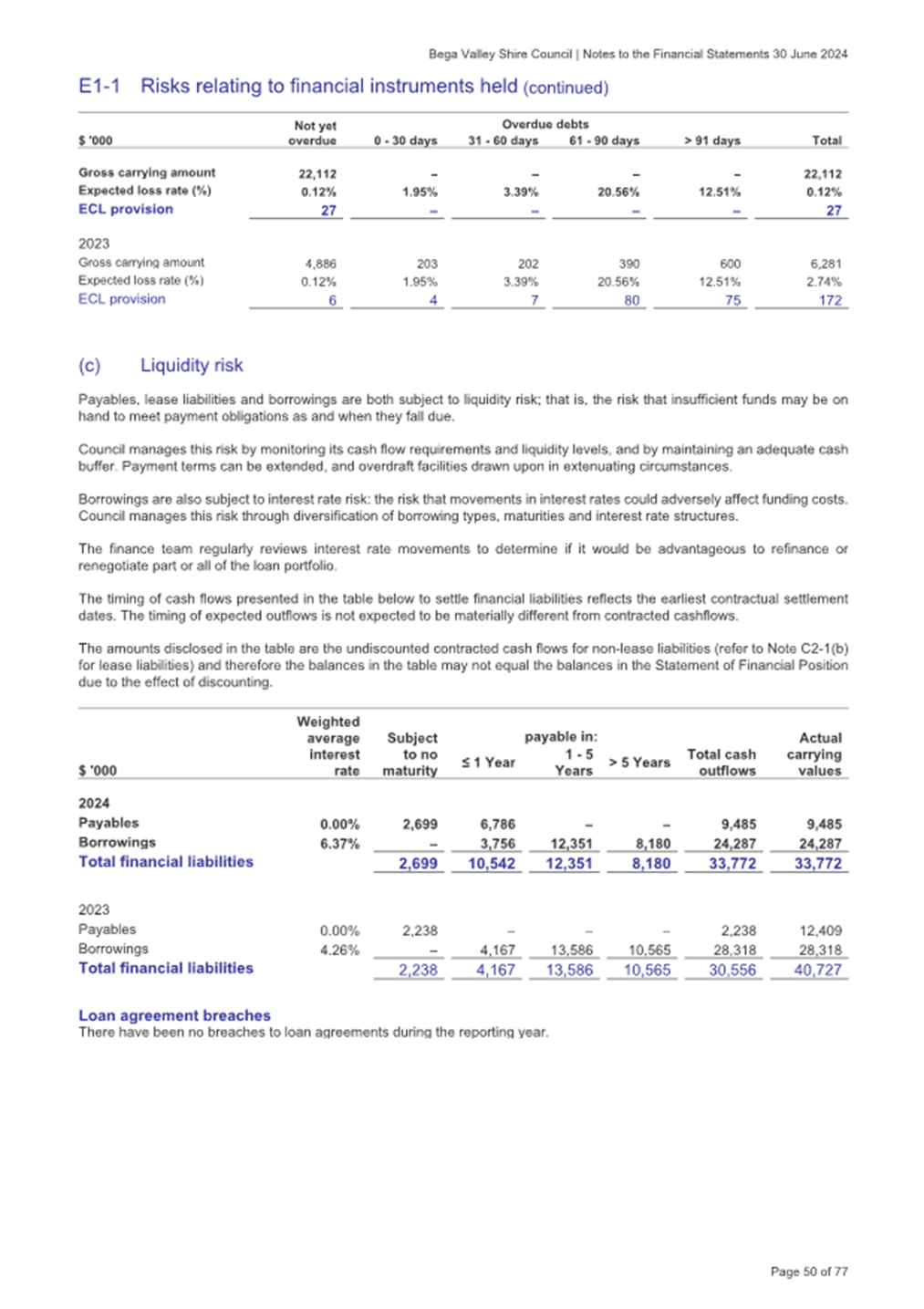

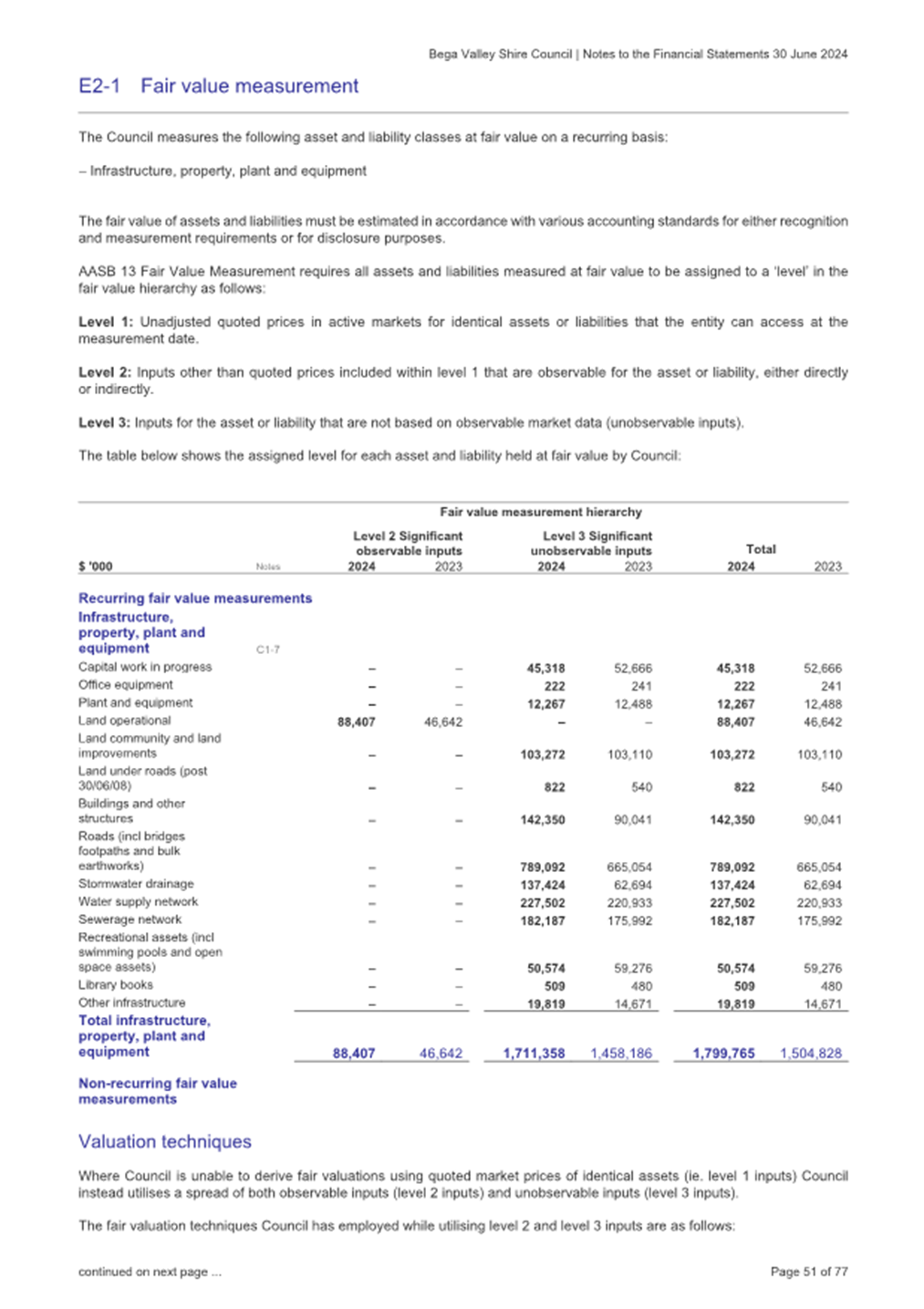

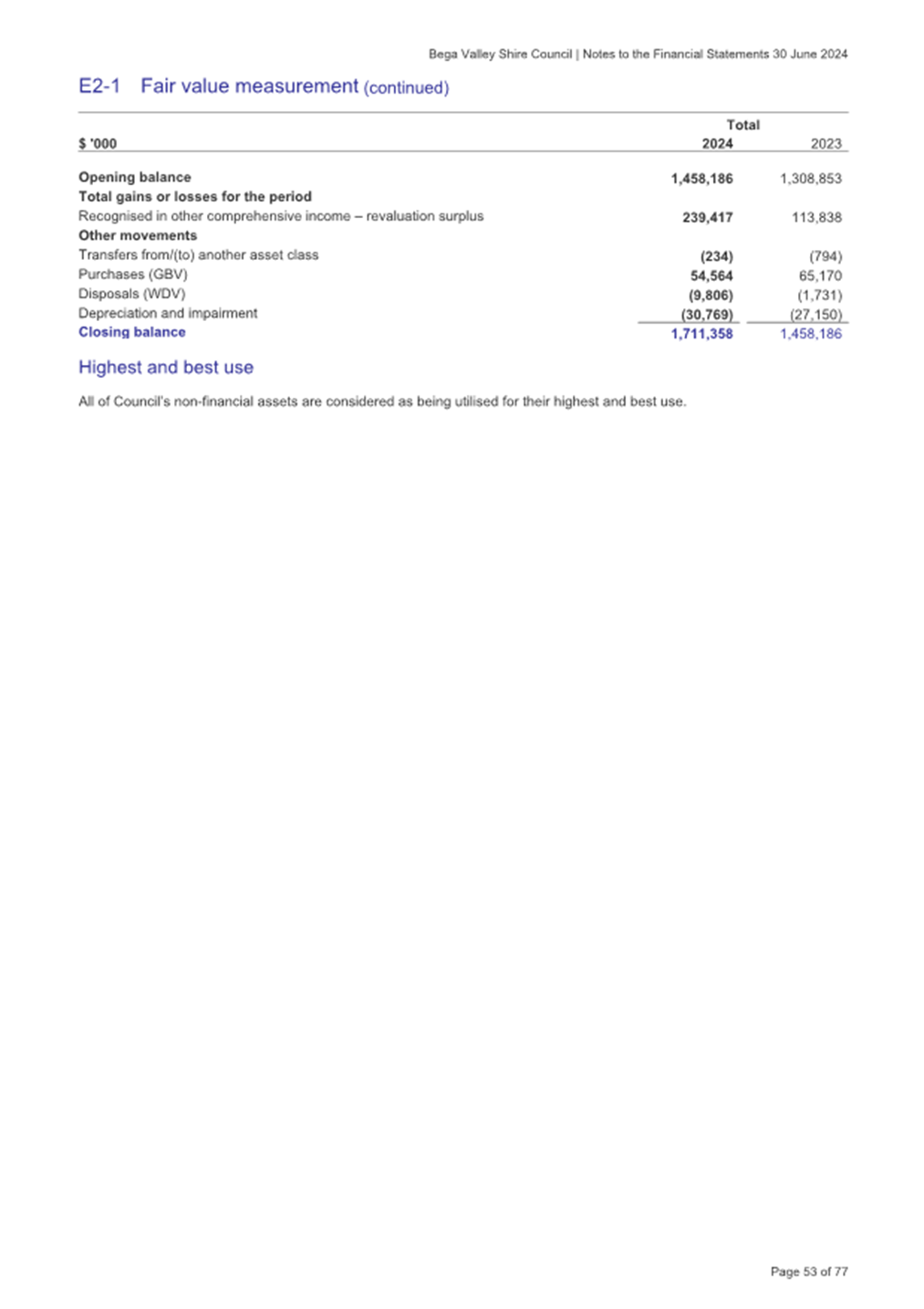

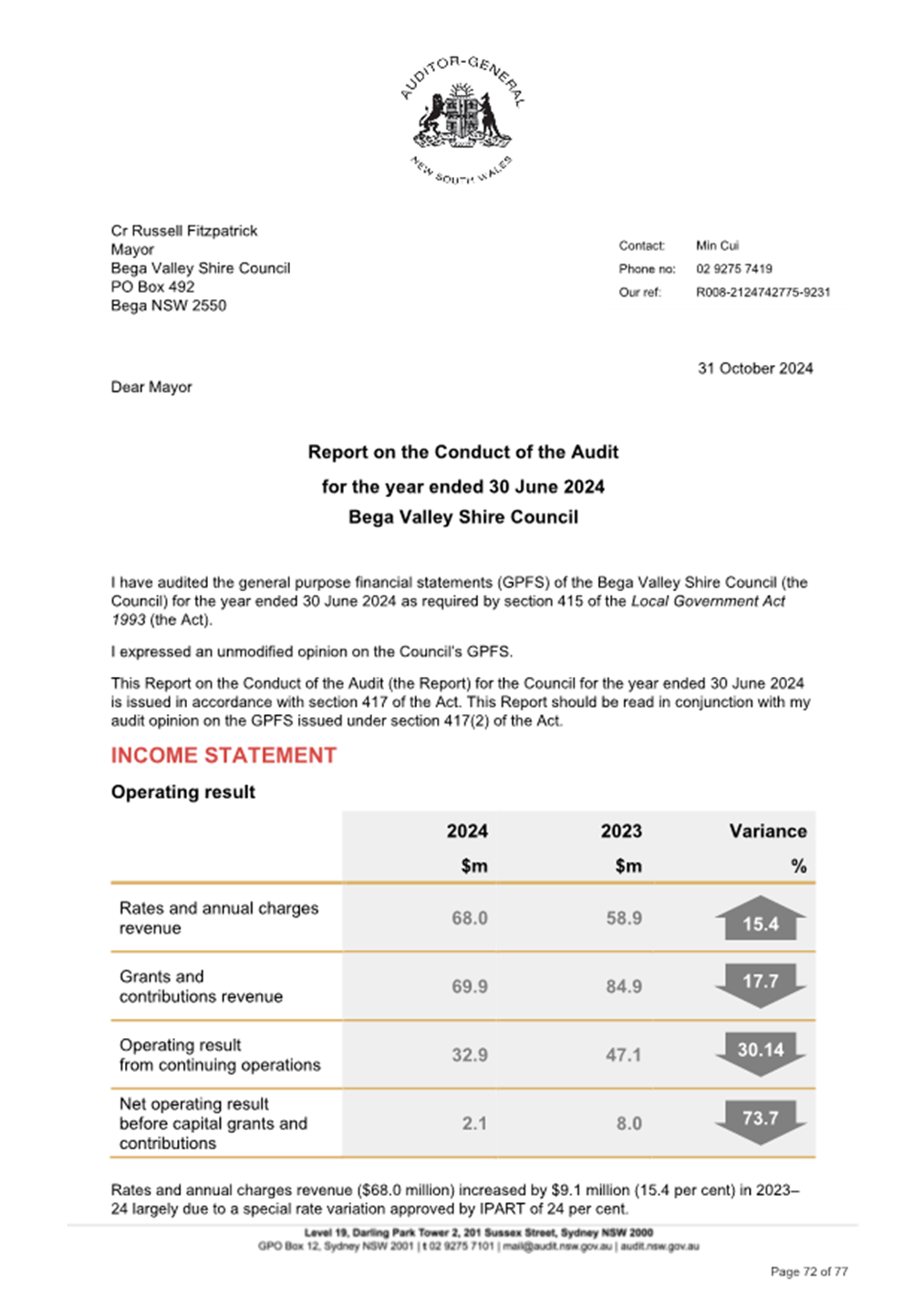

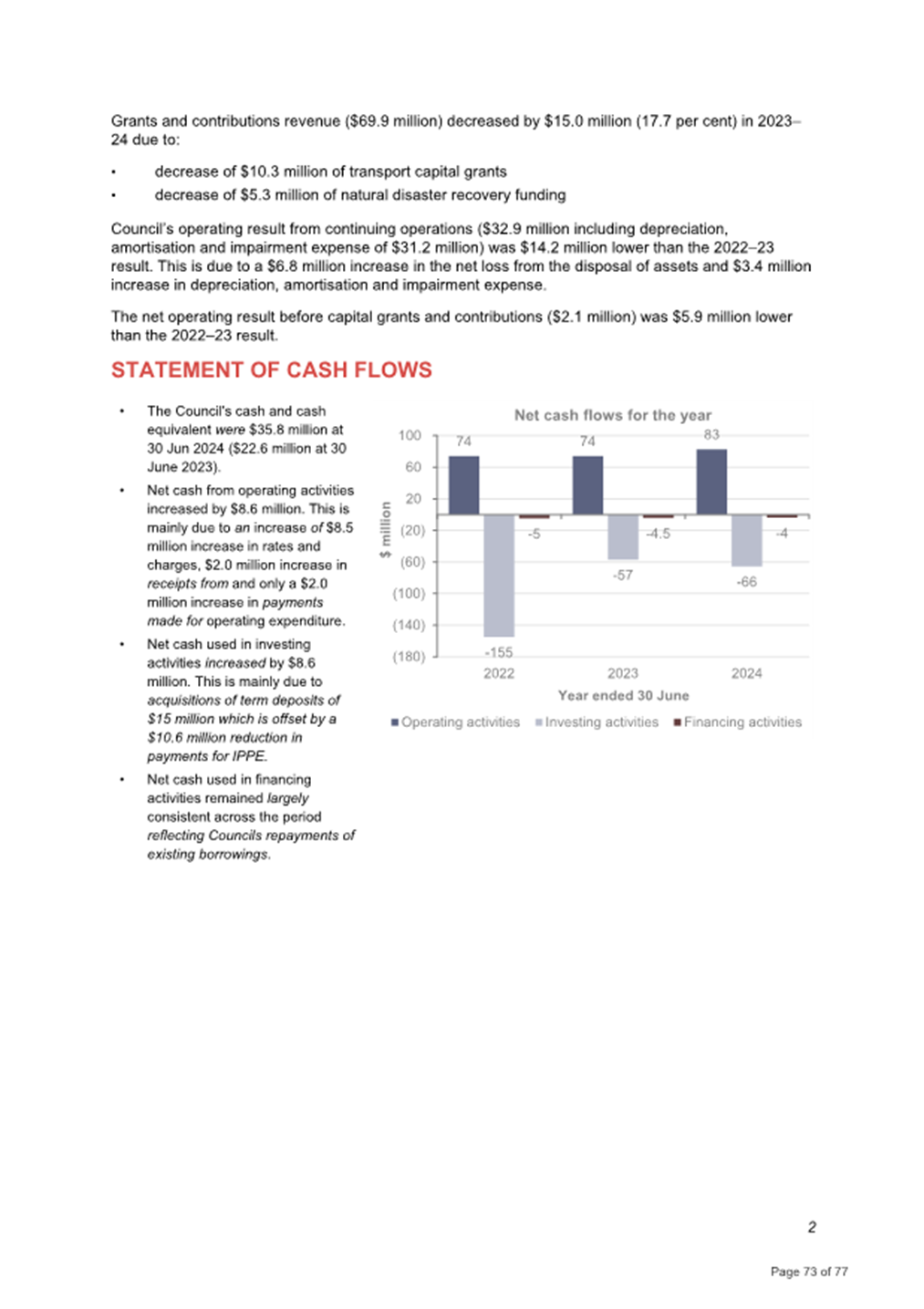

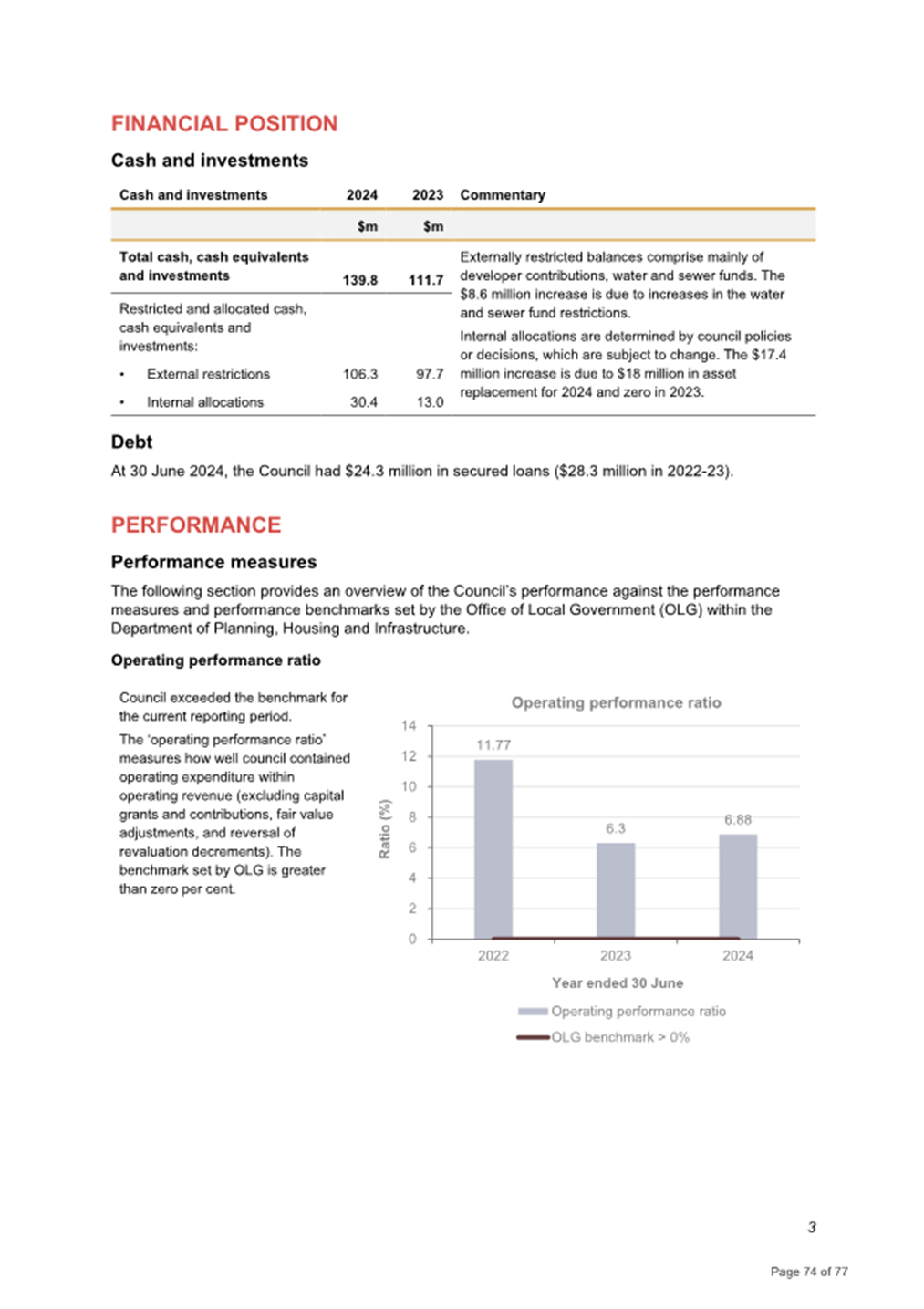

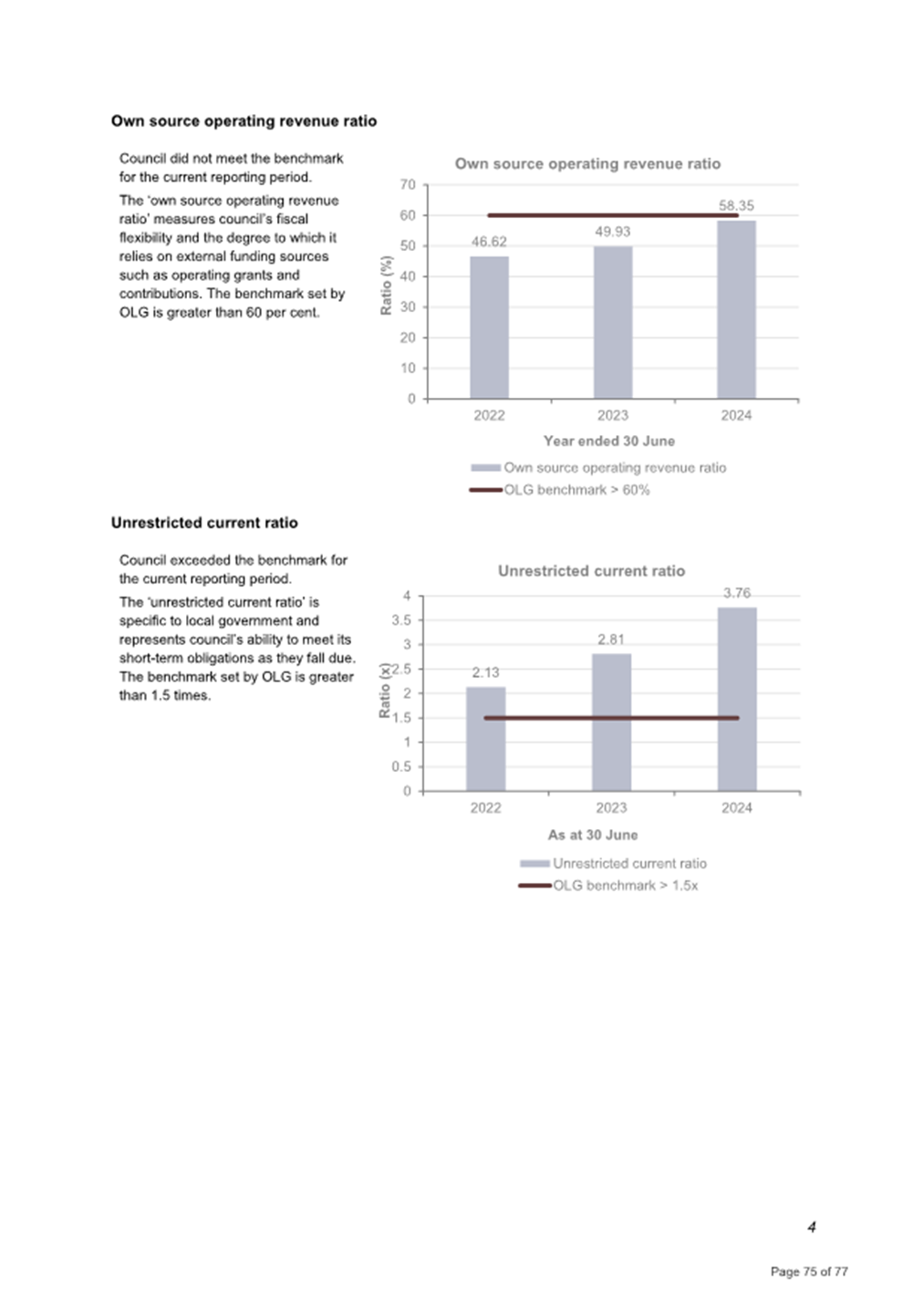

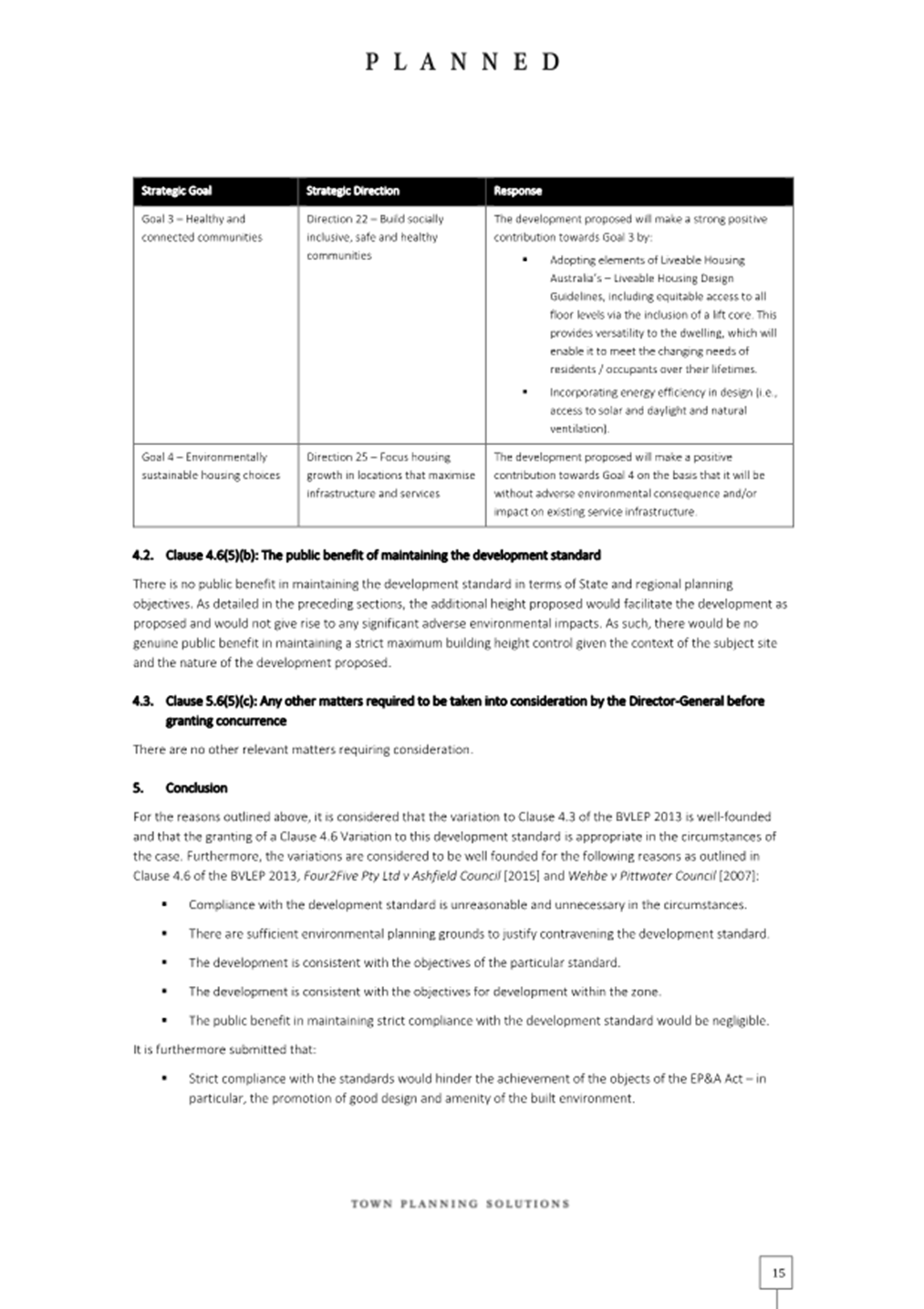

|

OrdinaryMeeting Notice and Agenda

An Ordinary Meeting of the Bega Valley Shire Council will be held at Council Chambers, Biamanga Room Bega Valley Commemorative Civic Centre

Bega on

|

|

OrdinaryMeeting Notice and Agenda

An Ordinary Meeting of the Bega Valley Shire Council will be held at Council Chambers, Biamanga Room Bega Valley Commemorative Civic Centre

Bega on

|

Council meetings are recorded and live streamed to the Internet for public viewing. By entering the Chambers during an open session of Council, you consent to your attendance and participation being recorded.

The recording will be archived and made available on Council’s website www.begavalley.nsw.gov.au. All care is taken to maintain your privacy; however as a visitor of the public gallery, your presence may be recorded.

The Agendas for Council Meetings and Council Reports for each meeting will be available to the public on Council’s website as close as possible to 5.00 pm on the Thursday prior to each Ordinary Meeting. A hard copy is also made available at the Bega Administration Building reception desk and on the day of the meeting, in the Council Chambers.

The Minutes of Council Meetings are available on Council's Website as close as possible to 5.00 pm on the Monday after the Meeting.

1. Please be aware that the recommendations in the Council Meeting Agenda are recommendations to the Council for consideration. They are not the resolutions (decisions) of Council.

2. Background for reports is provided by staff to the Chief Executive Officer for presentation to Council.

3. The Council may adopt these recommendations, amend the recommendations, determine a completely different course of action, or it may decline to pursue any course of action.

4. The decision of the Council becomes the resolution of the Council, and is recorded in the Minutes of that meeting.

5. The Minutes of each Council meeting are published in draft format, and are confirmed by Councillors, with amendments if necessary, at the next available Council Meeting.

If you require any further information or clarification regarding a report to Council, please contact Council’s Executive Assistant who can provide you with the appropriate contact details

Phone (02 6499 2222) or email execassist@begavalley.nsw.gov.au.

· Is the decision or conduct legal?

· Is it consistent with Government policy, Council’s objectives and Code of Conduct?

· What will the outcome be for you, your colleagues, the Council, anyone else?

· Does it raise a conflict of interest?

· Do you stand to gain personally at public expense?

· Can the decision be justified in terms of public interest?

· Would it withstand public scrutiny?

A conflict of interest is a clash between private interest and public duty. There are two types of conflict:

· Pecuniary – regulated by the Local Government Act 1993 and Office of Local Government

· Non-pecuniary – regulated by Codes of Conduct and policy. ICAC, Ombudsman, Office of Local Government (advice only). If declaring a Non-Pecuniary Conflict of Interest, Councillors can choose to either disclose and vote, disclose and not vote or leave the Chamber.

· Is it likely I could be influenced by personal interest in carrying out my public duty?

· Would a fair and reasonable person believe I could be so influenced?

· Conflict of interest is closely tied to the layperson’s definition of ‘corruption’ – using public office for private gain.

· Important to consider public perceptions of whether you have a conflict of interest.

1st Do I have private interests affected by a matter I am officially involved in?

2nd Is my official role one of influence or perceived influence over the matter?

3rd Do my private interests conflict with my official role?

For more detailed definitions refer to Sections 442, 448 and 459 or the Local Government Act 1993 and Bega Valley Shire Council (and Model) Code of Conduct, Part 4 – conflict of interest.

Whilst seeking advice is generally useful, the ultimate decision rests with the person concerned.Officers of the following agencies are available during office hours to discuss the obligations placed on Councillors, officers and community committee members by various pieces of legislation, regulation and codes.

|

Contact |

Phone |

|

Website |

|

Bega Valley Shire Council |

(02) 6499 2222 |

council@begavalley.nsw.gov.au |

www.begavalley.nsw.gov.au |

|

ICAC |

8281 5999 Toll Free 1800 463 909 |

icac@icac.nsw.gov.au |

www.icac.nsw.gov.au |

|

Office of Local Government |

(02) 4428 4100 |

olg@olg.nsw.gov.au |

http://www.olg.nsw.gov.au/ |

|

NSW Ombudsman |

(02) 8286 1000 Toll Free 1800 451 524 |

nswombo@ombo.nsw.gov.au |

Under the provisions of Section 451(1) of the Local Government Act 1993 (pecuniary interests) and Part 4 of the Model Code of Conduct prescribed by the Local Government (Discipline) Regulation (conflict of interests) it is necessary for you to disclose the nature of the interest when making a disclosure of a pecuniary interest or a non-pecuniary conflict of interest at a meeting.

The following form should be completed and handed to the Chief Executive Officer as soon as practible once the interest is identified. Declarations are made at Item 3 of the Agenda: Declarations - Pecuniary, Non-Pecuniary and Political Donation Disclosures, and prior to each Item being discussed:

Council meeting held on __________(day) / ___________(month) /____________(year)

|

Item no & subject |

|

|

Pecuniary Interest

|

In my opinion, my interest is pecuniary and I am therefore required to take the action specified in section 451(2) of the Local Government Act 1993 and or any other action required by the Chief Executive Officer. |

|

Significant Non-pecuniary conflict of interest |

– In my opinion, my interest is non-pecuniary but significant. I am unable to remove the source of conflict. I am therefore required to treat the interest as if it were pecuniary and take the action specified in section 451(2) of the Local Government Act 1993. |

|

Non-pecuniary conflict of interest |

In my opinion, my interest is non-pecuniary and less than significant. I therefore make this declaration as I am required to do pursuant to clause 5.11 of Council’s Code of Conduct. However, I intend to continue to be involved with the matter. |

|

Nature of interest |

Be specific and include information such as : · The names of any person or organization with which you have a relationship · The nature of your relationship with the person or organization · The reason(s) why you consider the situation may (or may be perceived to) give rise to a conflict between your personal interests and your public duty as a Councillor. |

|

If Pecuniary |

Leave chamber |

|

If Non-pecuniary (tick one) |

Disclose & vote Disclose & not vote Leave chamber |

|

Reason for action proposed |

Clause 5.11 of Council’s Code of Conduct provides that if you determine that a non-pecuniary conflict of interest is less than significant and does not require further action, you must provide an explanation of why you consider that conflict does not require further action in the circumstances |

|

Print Name |

I disclose the above interest and acknowledge that I will take appropriate action as I have indicated above. |

|

Signed |

|

NB: Please complete a separate form for each Item on the Council Agenda on which you are declaring an interest.

|

Council |

27 November 2024 |

Statement of Ethical Obligations

Recommendation

That the Minutes of the Ordinary Meeting held on 6 November 2024 as circulated, be taken as read and confirmed.

Pecuniary, Non-Pecuniary and Political Donation Disclosures to be declared and tabled. Declarations also to be declared prior to discussion on each item.

8.1 Demolition and erection of a 2 storey dwelling and swimming pool - Lot:12 DP: 249625 - 9 Weemilah Drive Pambula Beach............................................ 2

8.2 Endorsement of Minor Amendments Planning Proposal................................................................ 2

9.1 Request for Tender (RFT) 2425-010 Bemboka Reservoir Renewal................................................ 2

9.2 Waste Grants Program FY 2025-26 to FY 2028-29.. 2

9.3 Request for Tender (RFT) 2324-064 Brogo Tank 2 Replacement......................................................... 2

9.4 Regional Airport Program Round 4 (RAP4) Application............................................................ 2

9.5 Merimbula Airport Taxiway Charlie Culvert Upgrade - RAP3.................................................................... 2

10.1 Annual Report 2023-24............................................ 2

10.2 Subdivision of Central Waste Facility for lease purposes................................................................ 2

10.3 Adoption of Policy 6.23 - Payment of Expenses and Provision of Facilities to Councillors..................... 2

10.4 Certificate of Investment October 2024.................. 2

10.5 Community Satisfaction Survey 2024...................... 2

10.6 Adoption of Policy 6.07 Investment Policy.............. 2

10.7 EOI 2425-032 Use of Council owned and managed reserves for mobile food vending......................... 2

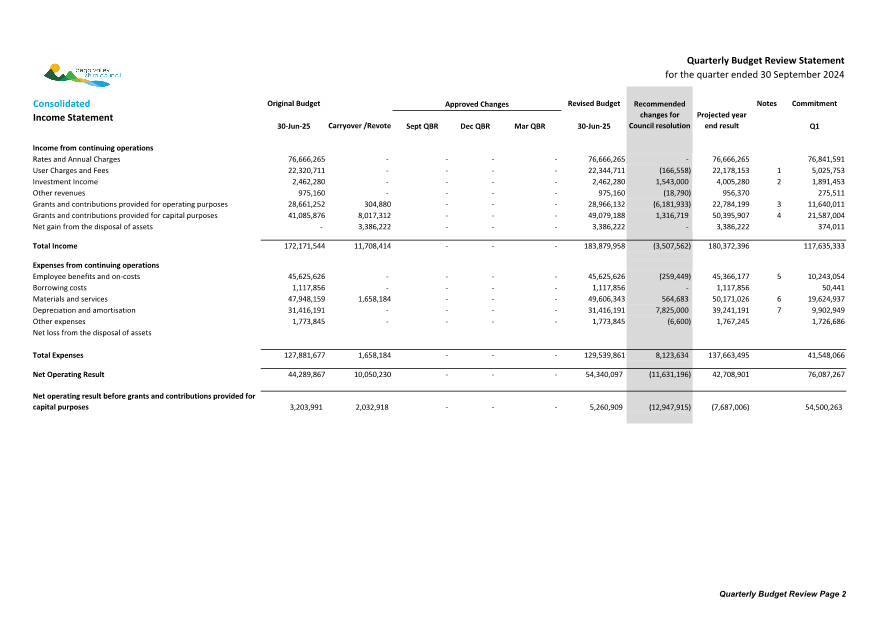

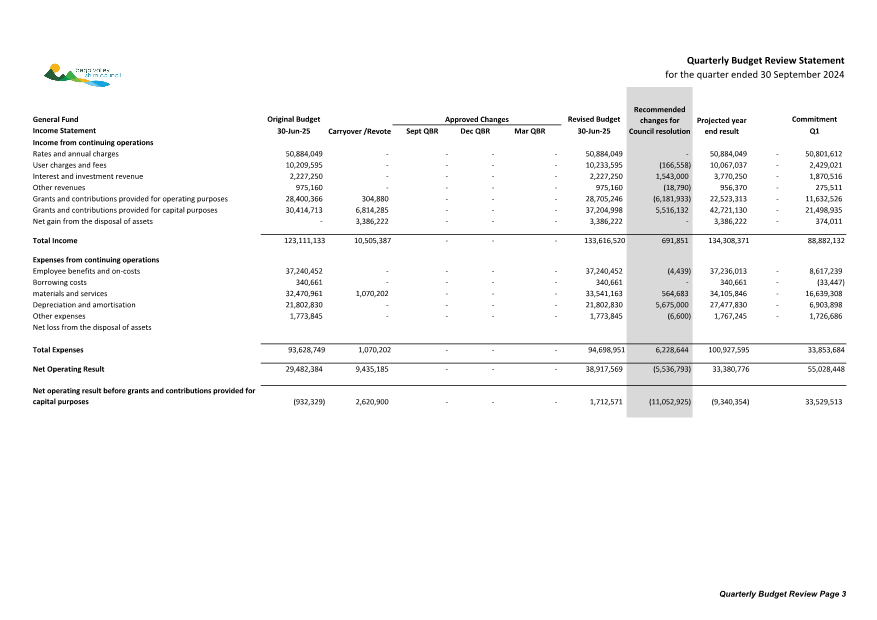

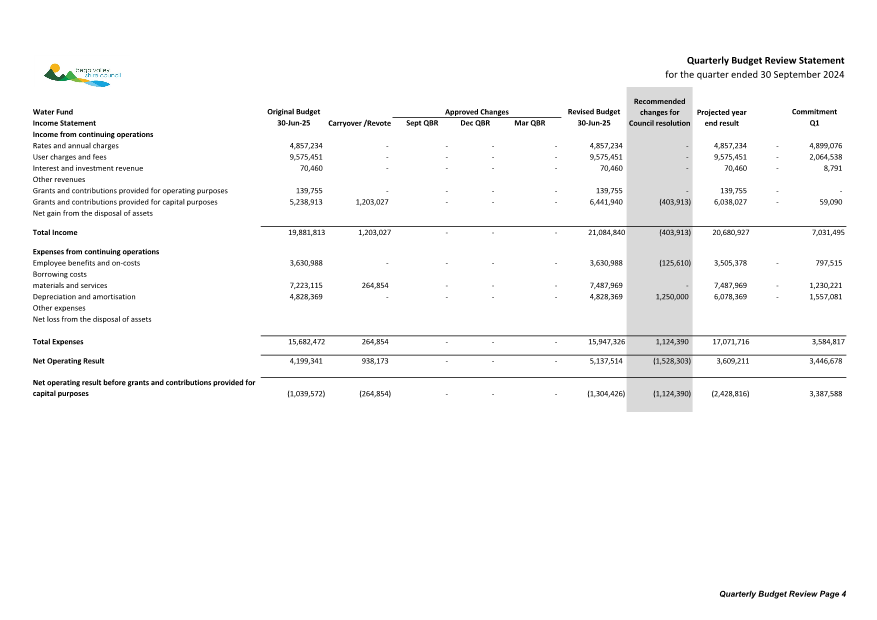

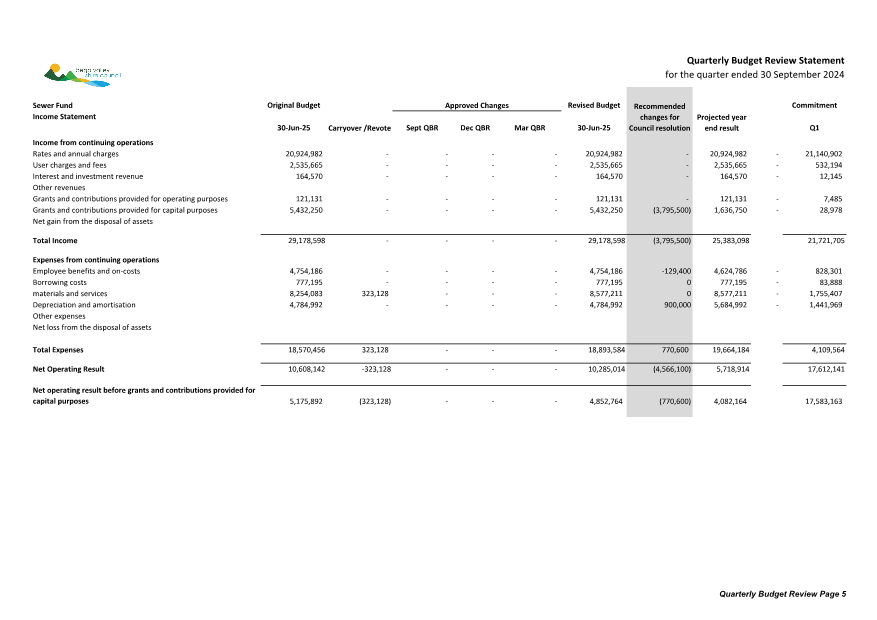

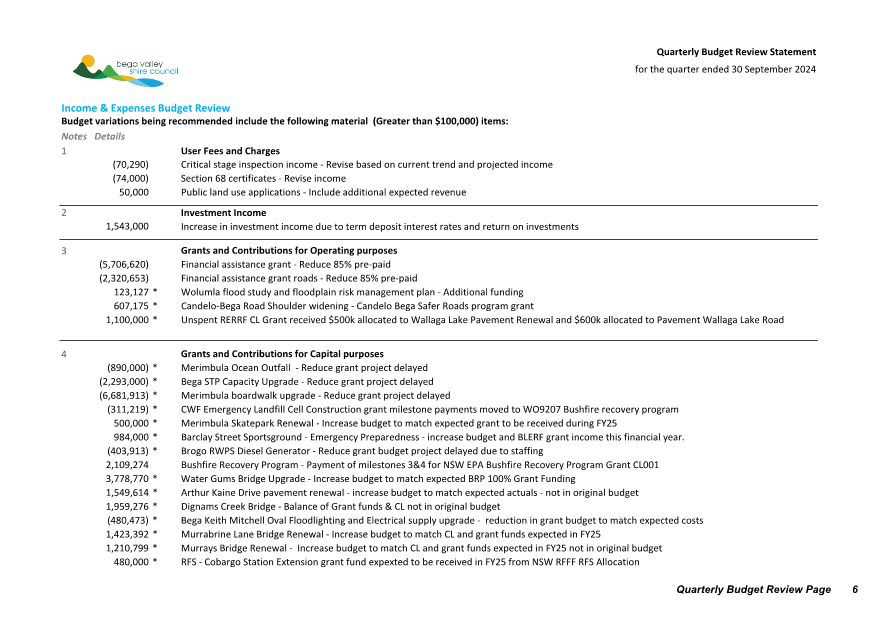

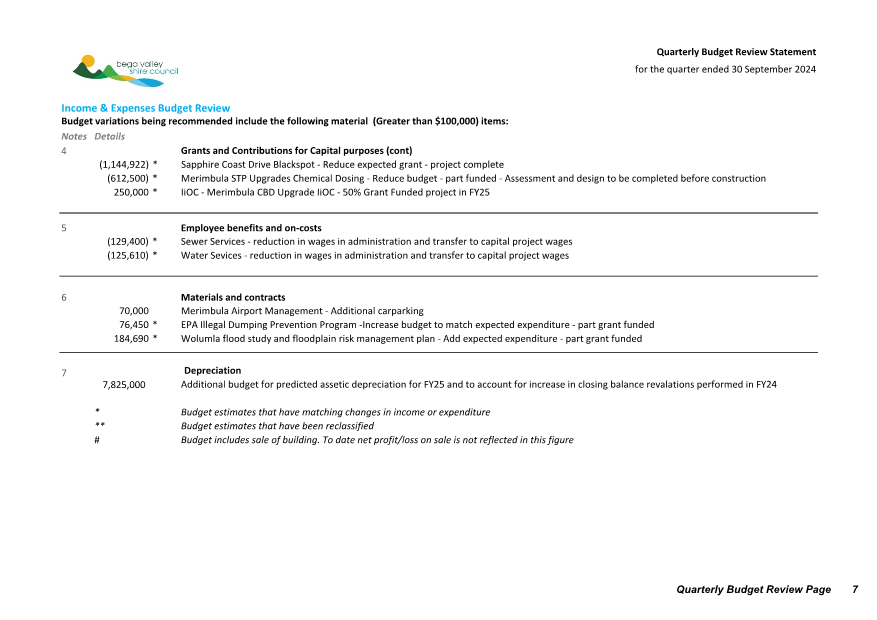

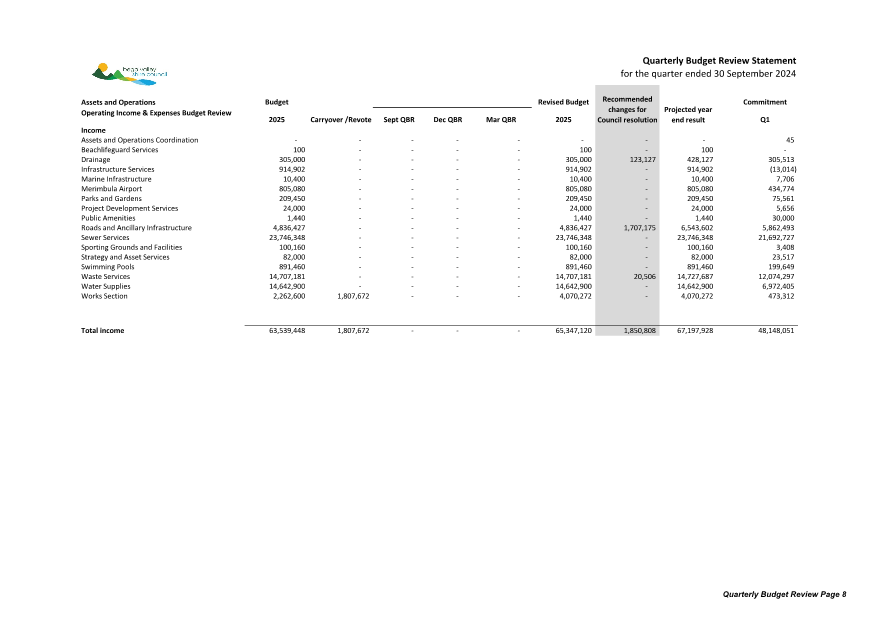

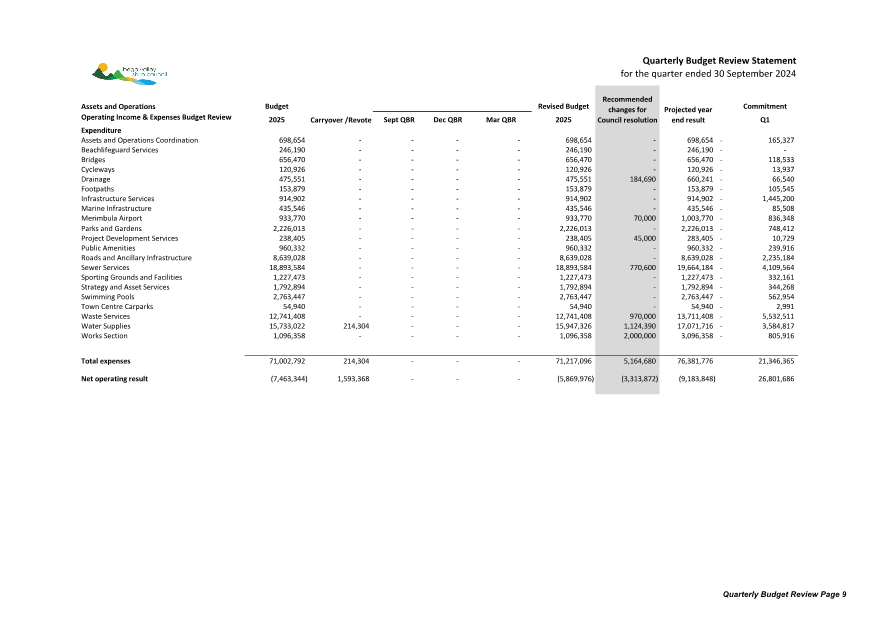

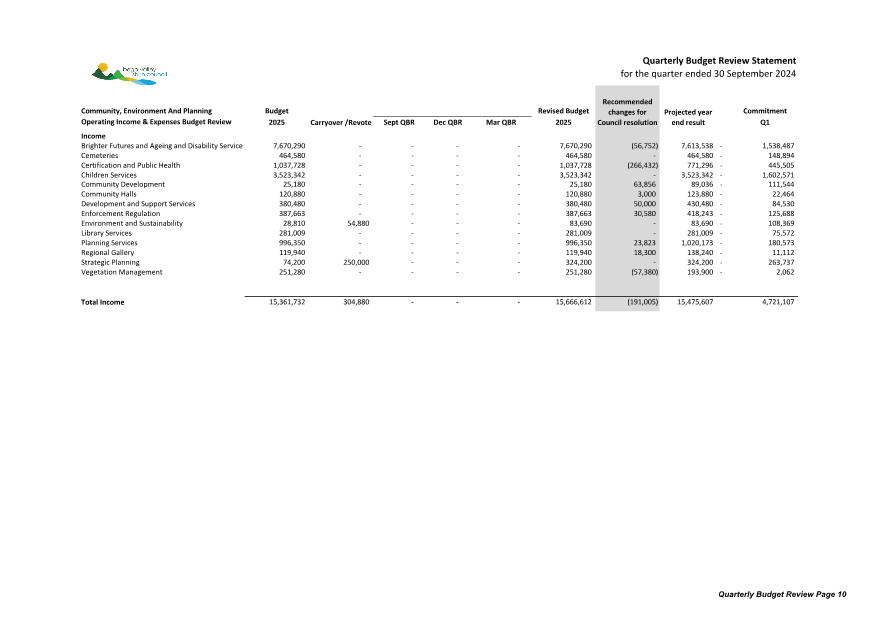

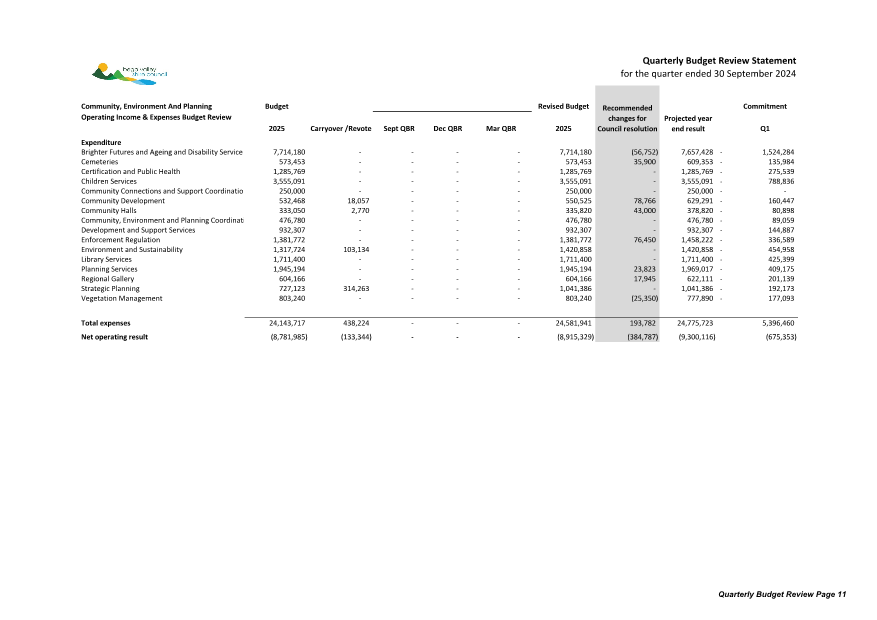

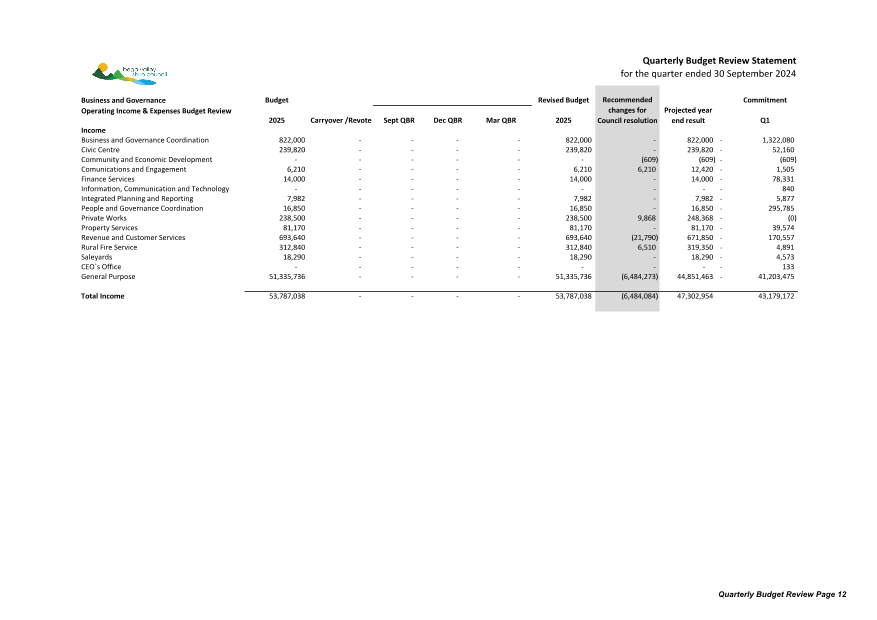

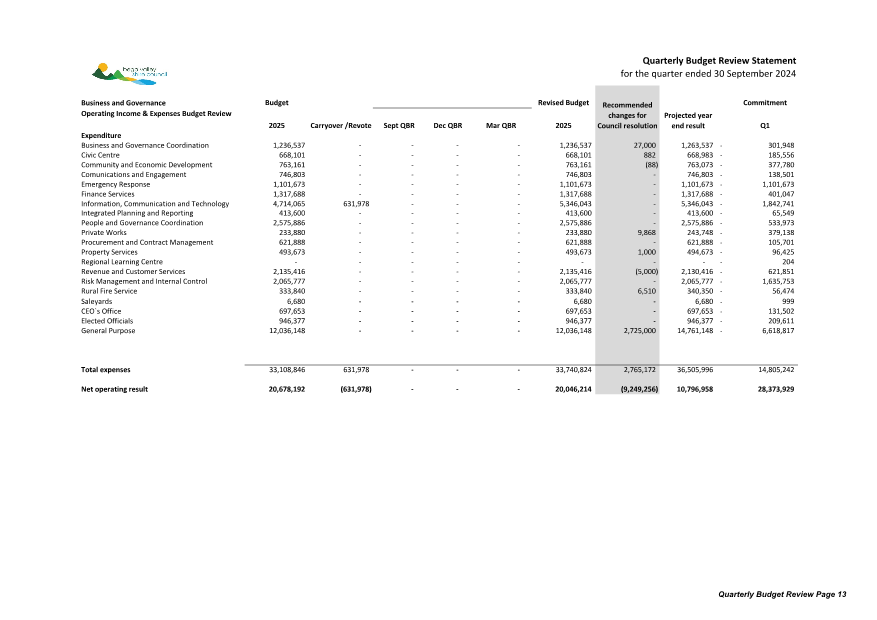

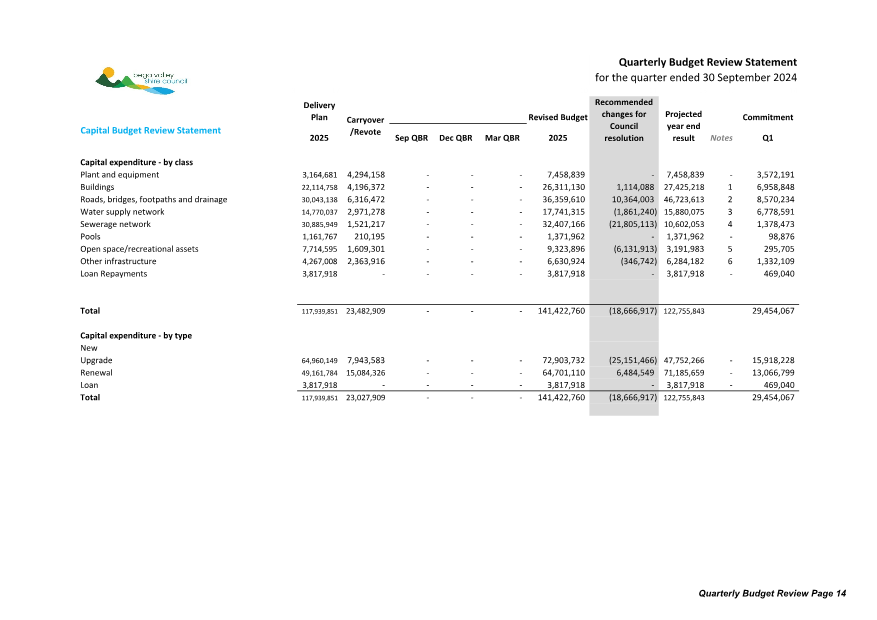

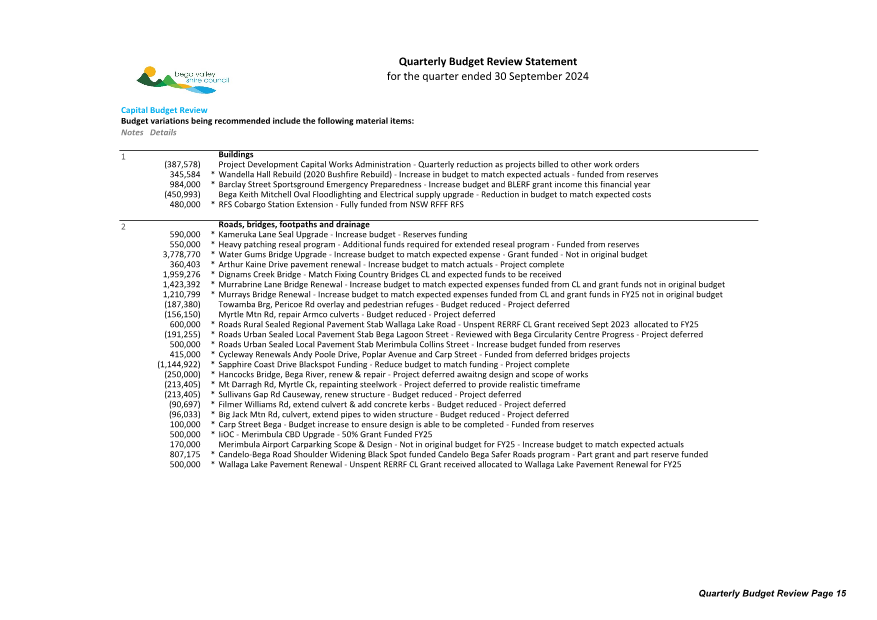

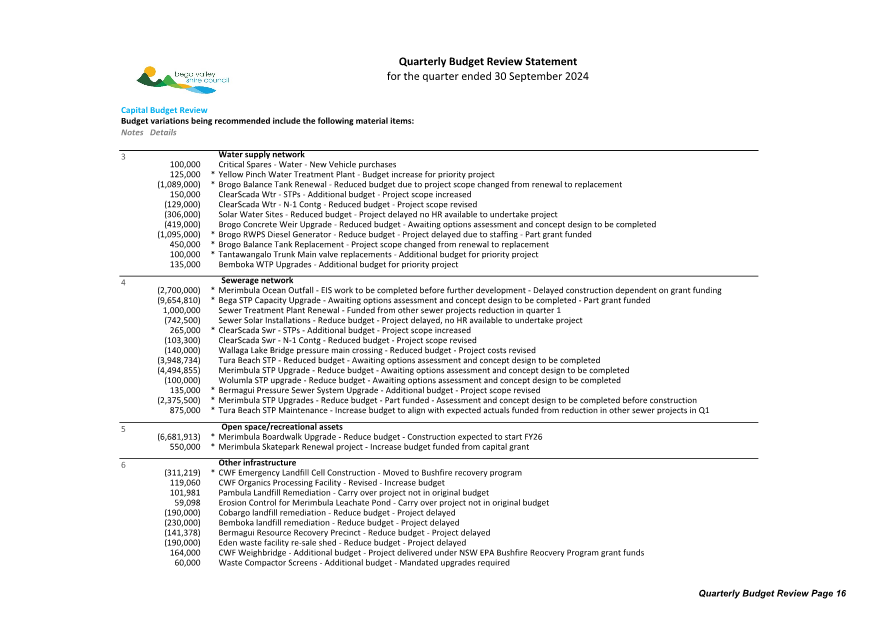

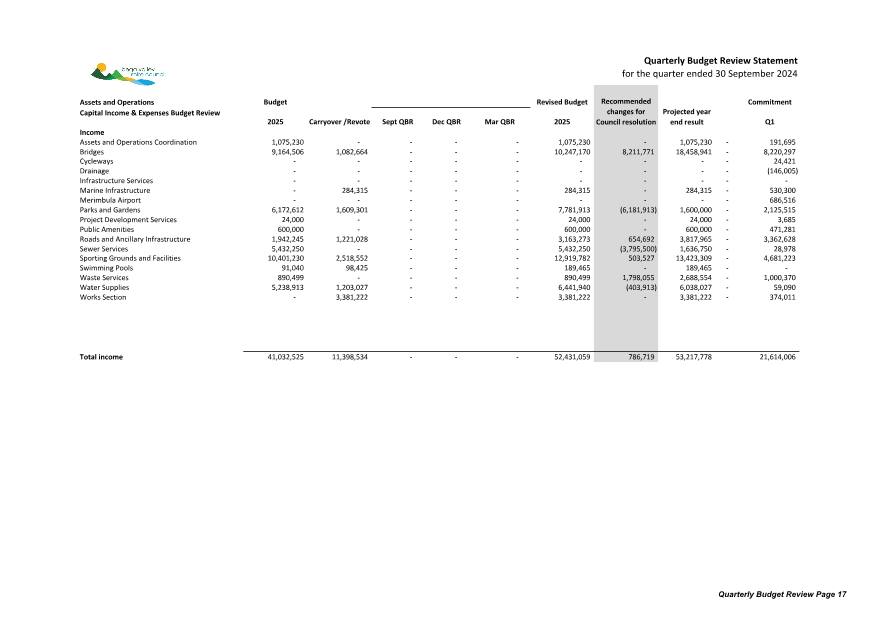

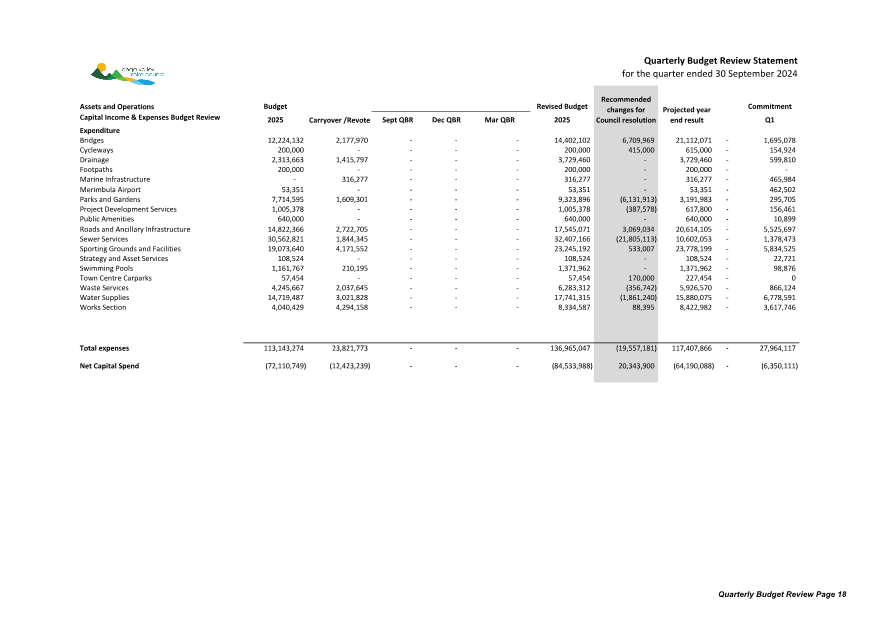

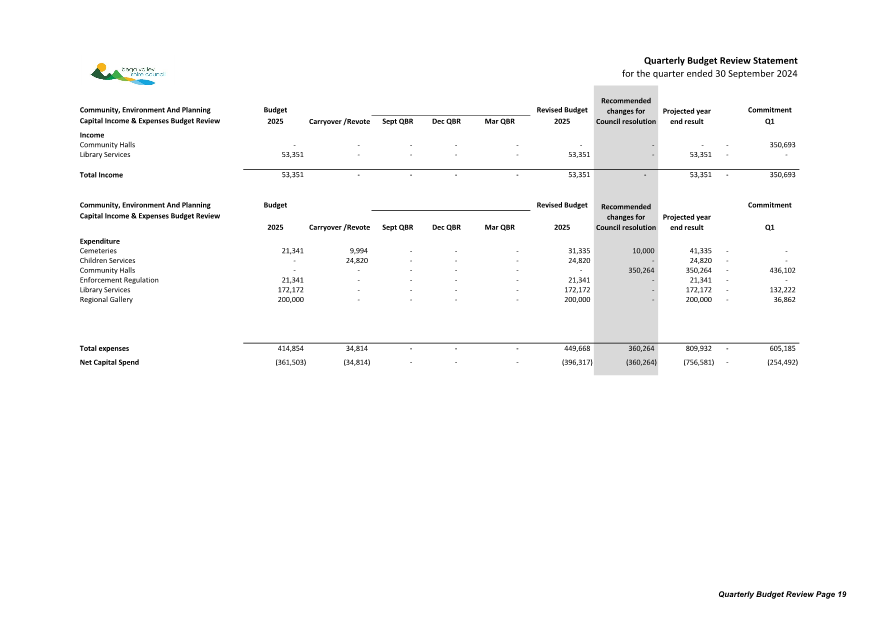

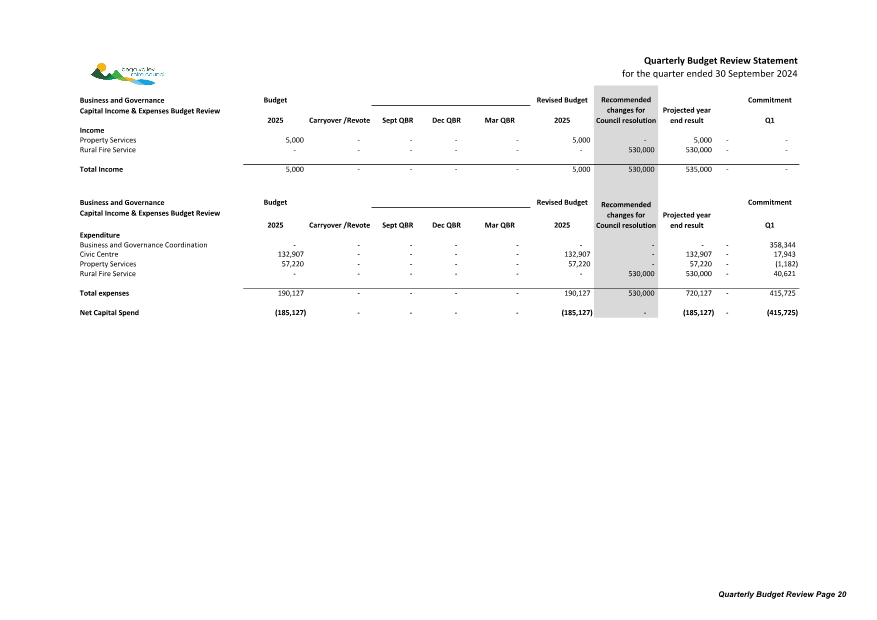

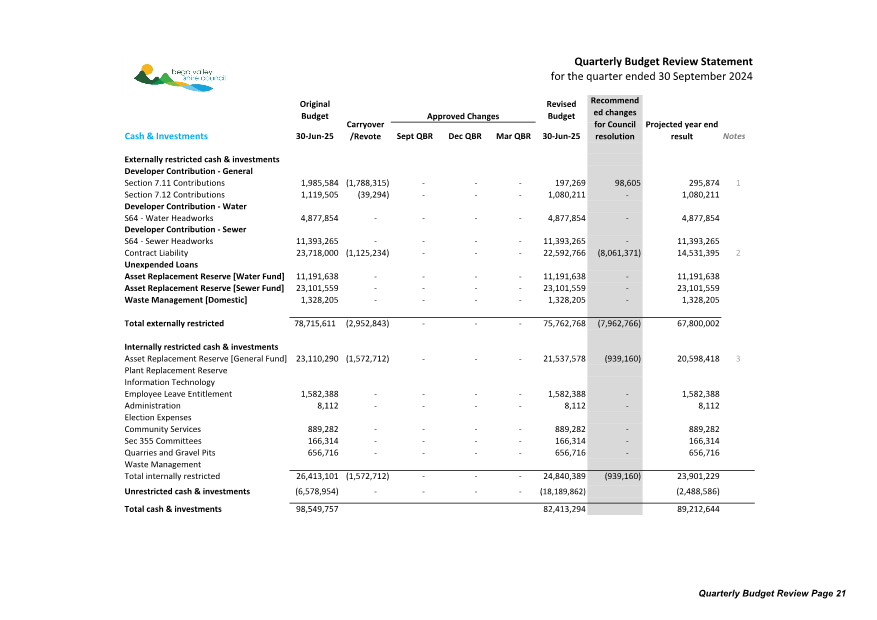

10.8 Quarterly Budget Review Statement (QBRS) September 2024 Q1.............................................. 2

10.9 Presentation of Financial Statements and Audit Report for the Year Ended 30 June 2024.............. 2

10.10 Draft 2024 - 2028 Community Engagement Strategy............................................................................... 2

10.11 Audit and Risk Improvement Committee and Councillor Representatives on Committees......... 2

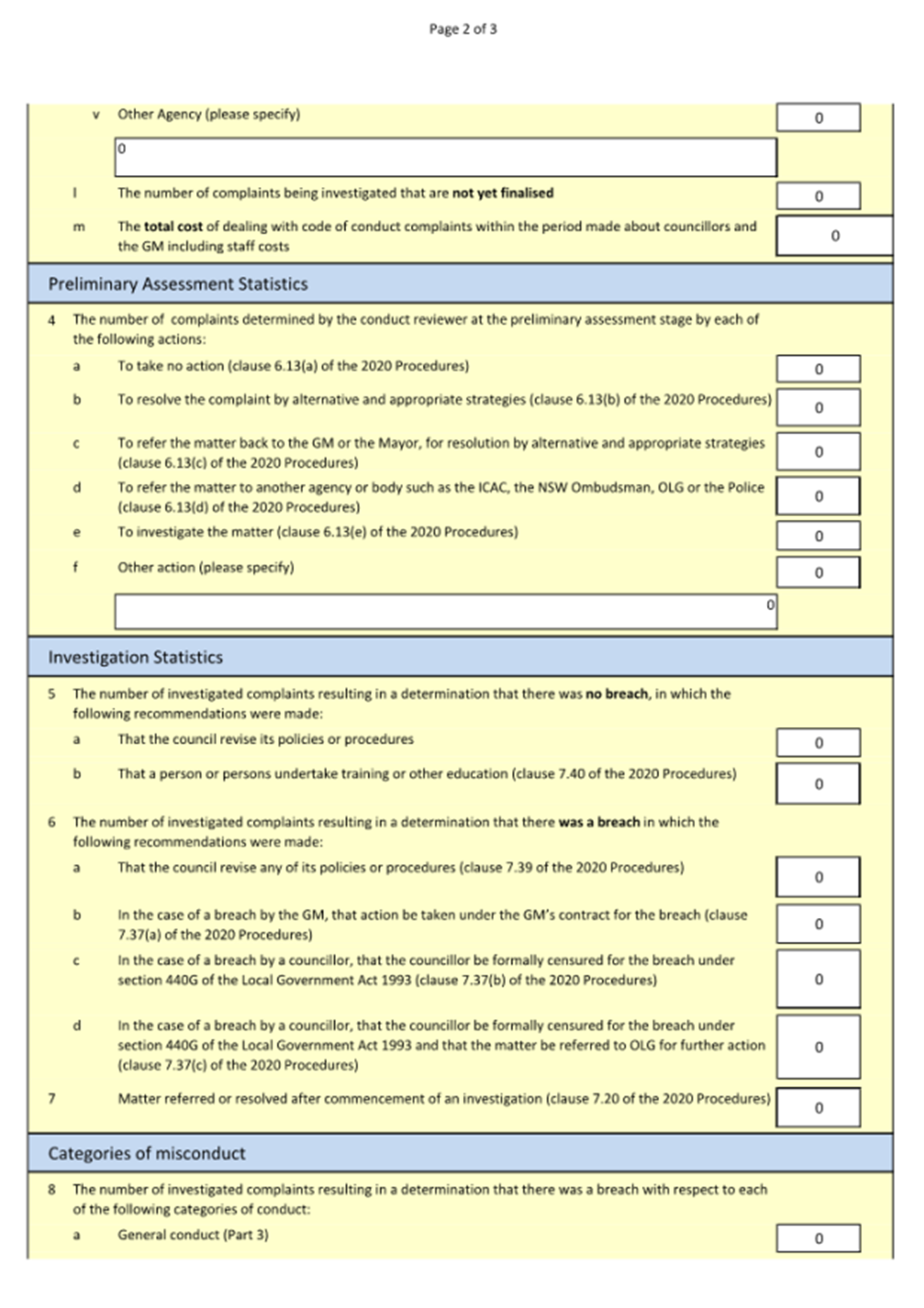

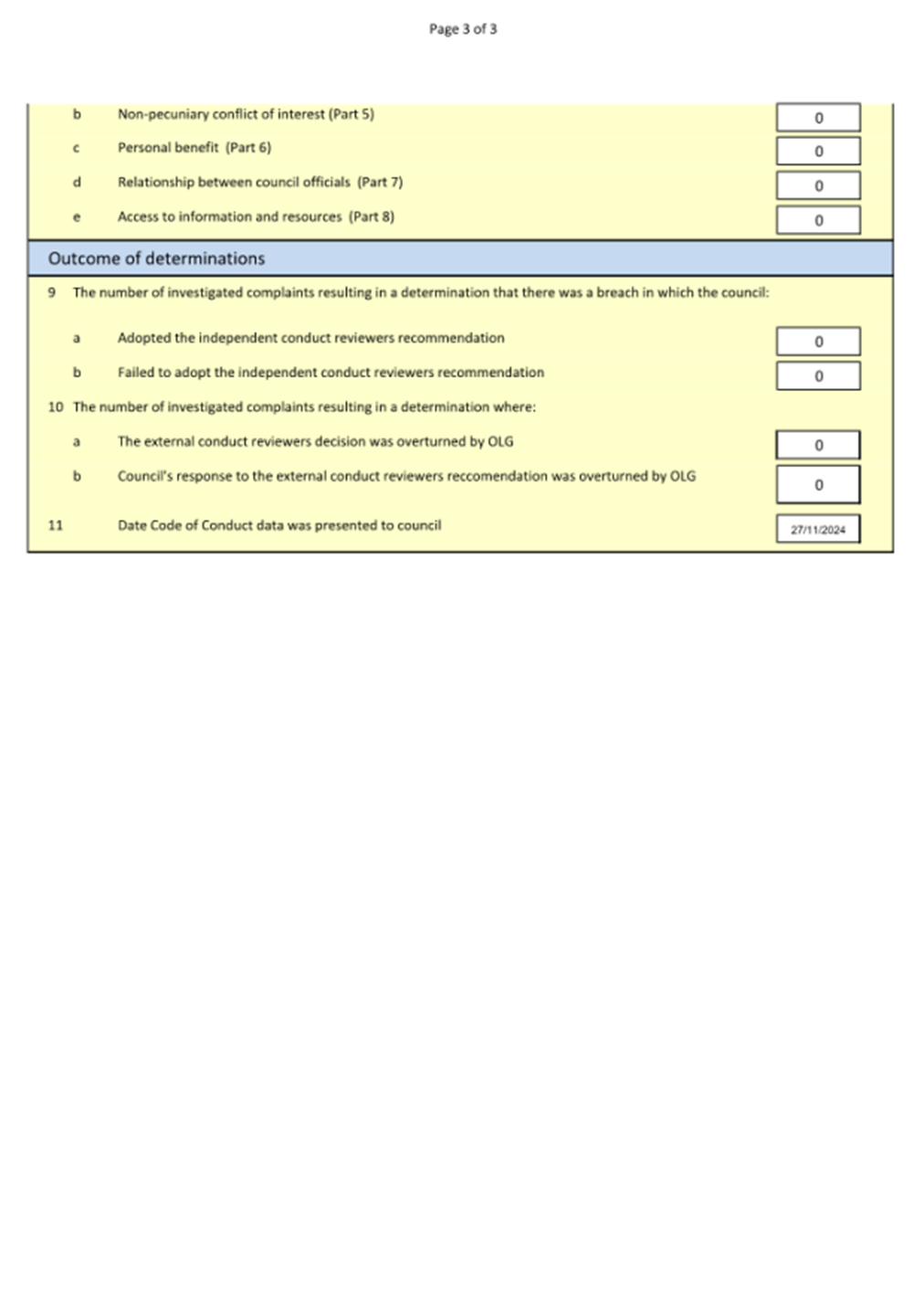

10.12 Code of Conduct Statistical Reporting 2023/2024.. 2

10.13 6.16 Draft Policy - Community Engagement............ 2

10.14 Submission to Office of Local Government (OLG) - Councillor Conduct and Meeting Practices - Discussion Paper................................................... 2

13.1 Review Pathways..................................................... 2

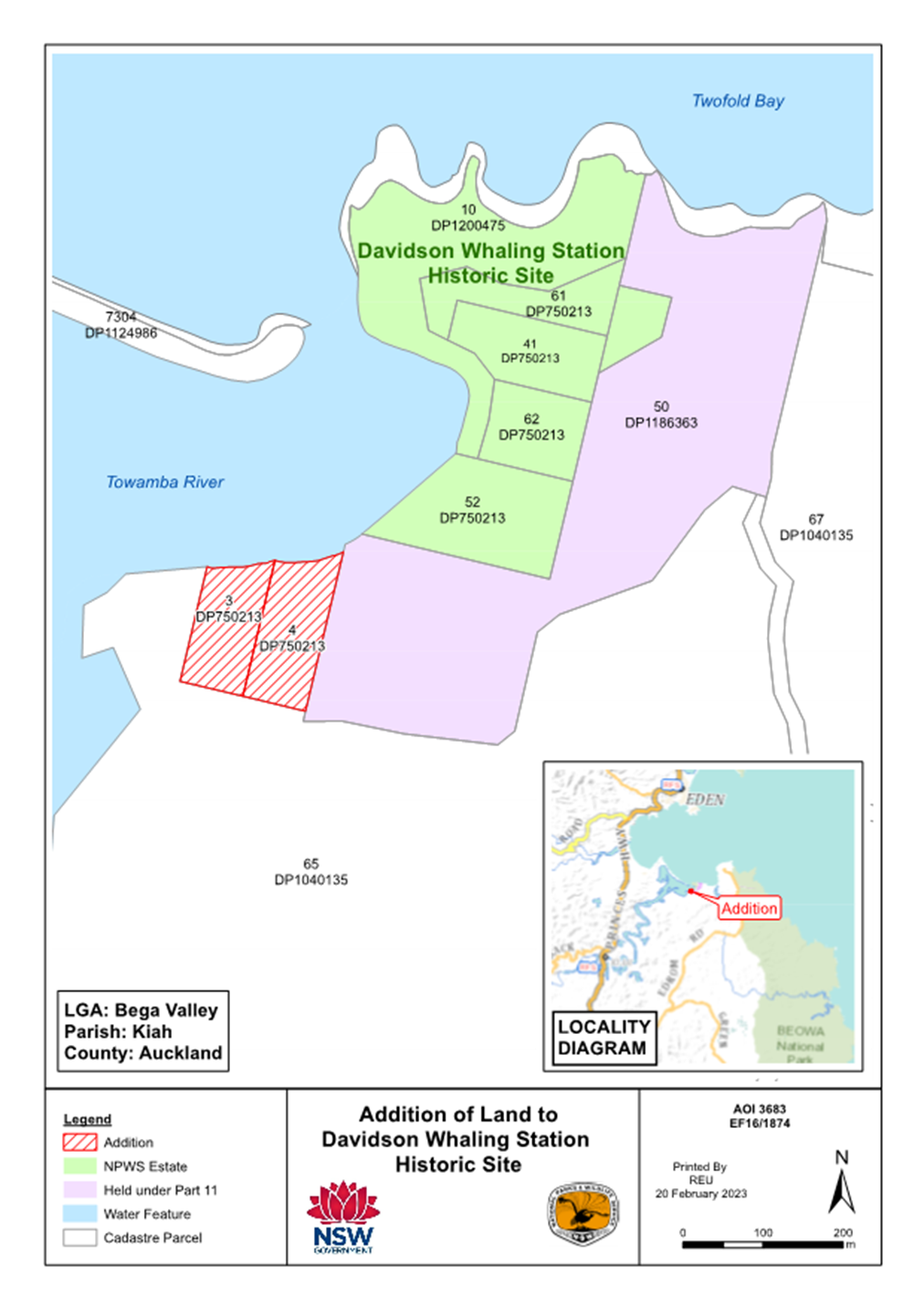

13.2 Acquisition of land in Eden...................................... 2

13.3 Development assessment audit............................... 2

13.4 Activation of Nullica Lodge site................................ 2

15.1 Cr Nadin - NSW Government PFAS water supply testing................................................................... 2

Representations by members of the public regarding closure of part of meeting

Adjournment Into Closed Session, exclusion of the media and public 2

|

Council |

27 November 2024 |

Staff Reports – Community, Environment and Planning

27 November 2024

8.1 Demolition and erection of a 2 storey dwelling and swimming pool - Lot:12 DP: 249625 - 9 Weemilah Drive Pambula Beach............................................... 2

8.2 Endorsement of Minor Amendments Planning Proposal.................................................................... 2

|

Council 27 November 2024 |

Item 8.1 |

8.1. 2023.241 Demolition and erection of a 2 storey dwelling and swimming pool - Lot:12 DP: 249625 - 9 Weemilah Drive Pambula Beach

Director Community Environment and Planning

|

Applicant |

Elizabeth Slapp (PLANNED) |

|

Owner |

Glen and Michelle Baker |

|

Site |

Lot:12 DP: 249625 – 9 Weemilah Drive, Pambula Beach |

|

Zone |

R2 Low Density Residential |

|

Site area |

682.5m² |

|

Proposed development |

Proposed demolition of existing dwelling house and the construction of a new two storey dwelling house, swimming pool and associated works |

Precis

The application includes the demolition of the existing dwelling house and the proposed construction of a new two storey dwelling house and ancillary swimming pool, with associated earthworks and retaining structures.

The application is being reported to Council as the new dwelling would exceed the height limit of 7.5 metres as prescribed in Clause 4.3 of the Bega Valley Local Environmental Plan 2013 (BVLEP 2013). The application is accompanied by a Clause 4.6 request for variation under BVLEP 2013 to the height of buildings development standard. As the variation request is greater than 10%, Council assessing staff do not have delegation to determine the application and therefore the application is to be determined by the elected Council.

The application is recommended for approval.

1. That Council support the Clause 4.6 variation request to the height of building development standard, specified under Clause 4.3(2) of the Bega Valley Local Environmental Plan 2013.

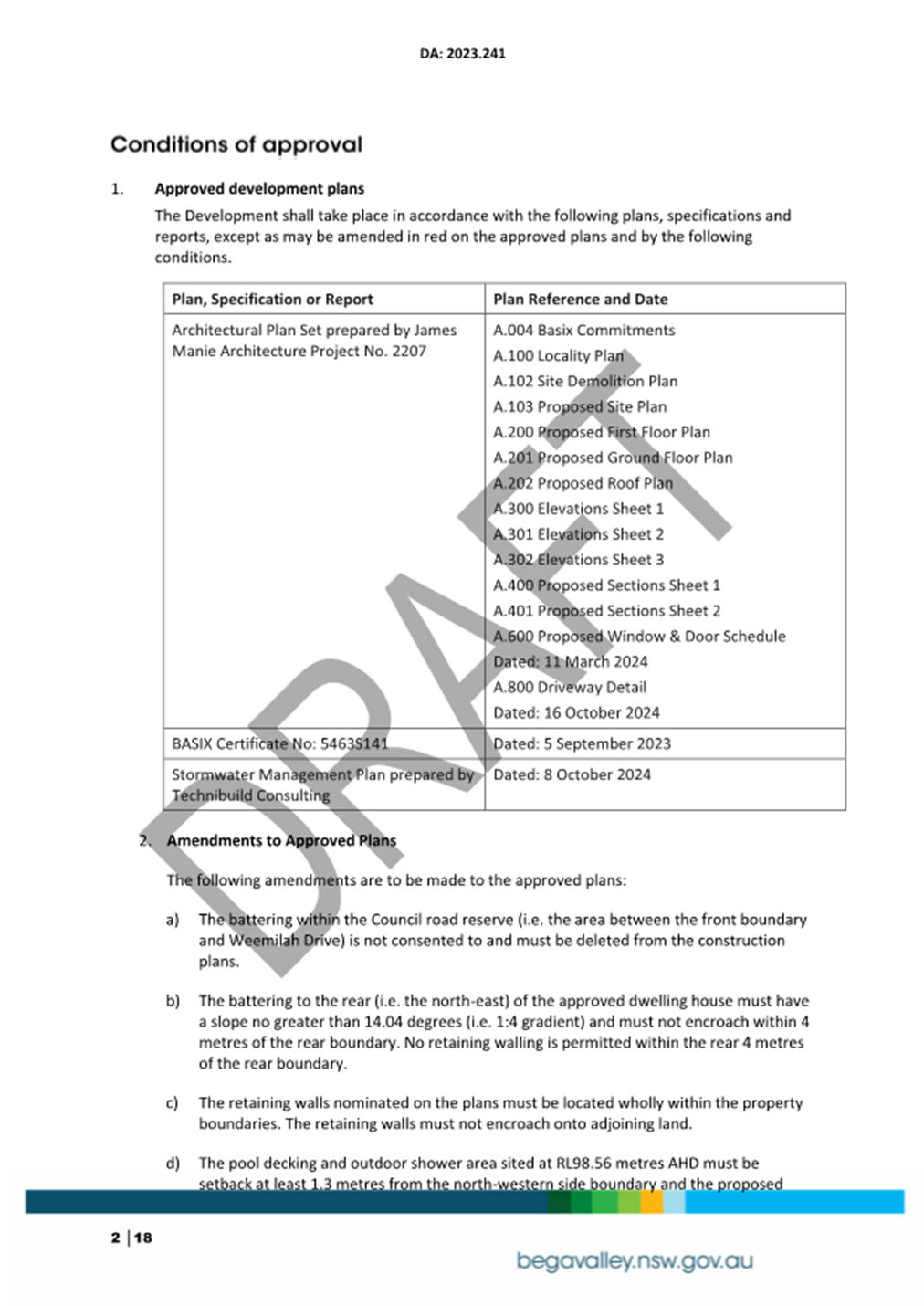

2. That Council approve development application 2023.241 for the demolition of existing dwelling and construction of a new dwelling, swimming pool and associated works at Lot 12 DP 249625, 9 Weemilah Drive, Pambula Beach, subject to the conditions of consent provided in Attachment 2.

3. Notify those who made a submission of Council’s decision.

Executive Summary

Development Application (DA) 2023.241 is being reported to Council for determination because the application seeks to vary the height of buildings development standard specified by Clause 4.3 of BVLEP 2013.

The development proposal has been assessed under Section 4.15 of the Environmental Planning and Assessment Act 1979 (EP&A Act) – refer Attachment 1. The variation to the height limit is considered moderate given the location of the exceedance to the height limit is confined to a small area of the building and is relative to the topography of the site, with minimal resulting impacts to streetscape character and neighbourhood amenity.

The proposed development is recommended for approval, subject to the draft conditions of consent provided in Attachment 2.

Background and Site description

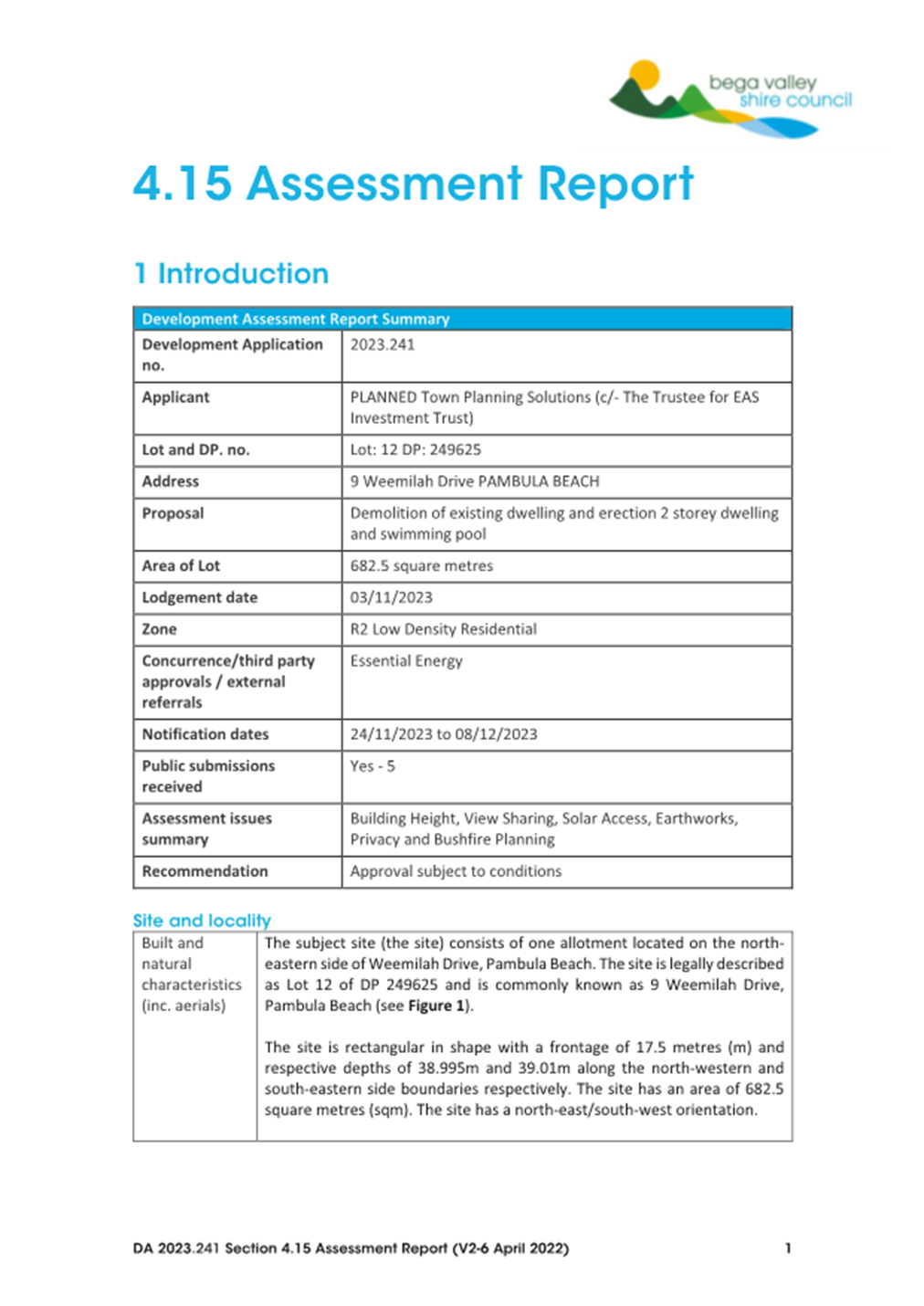

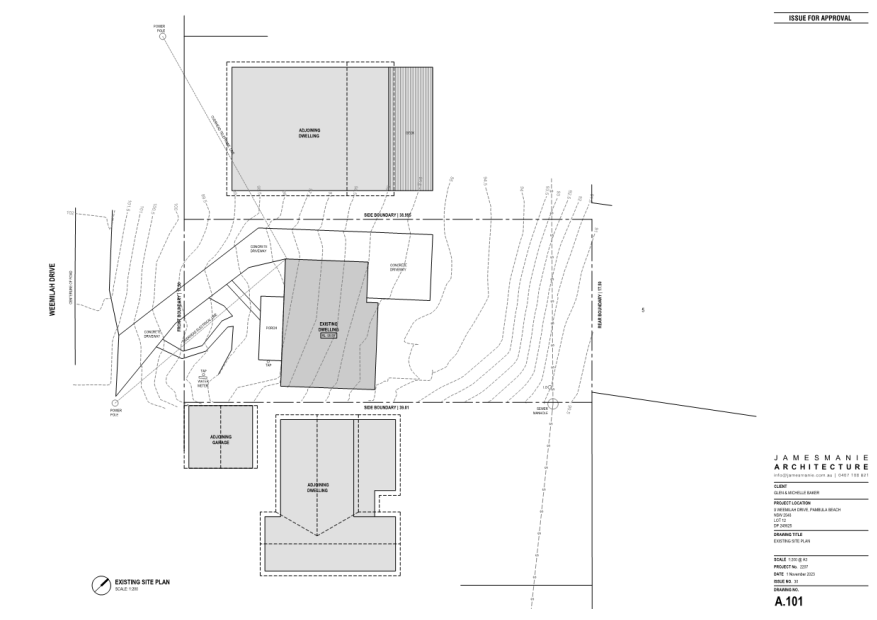

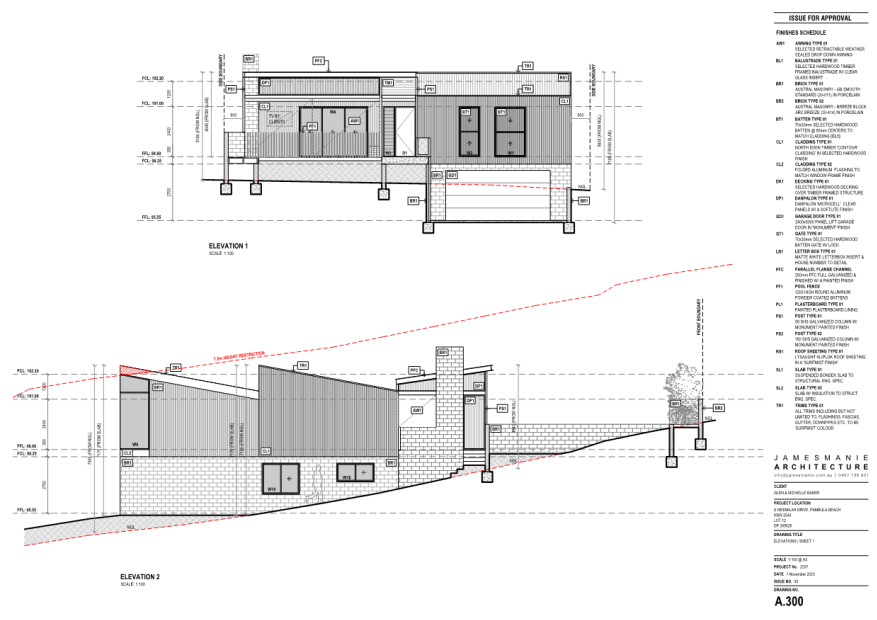

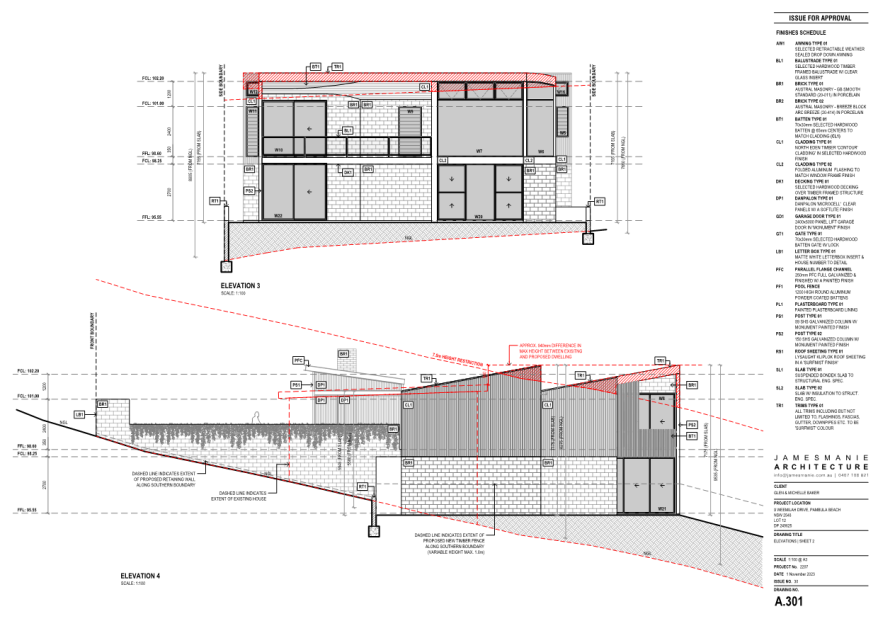

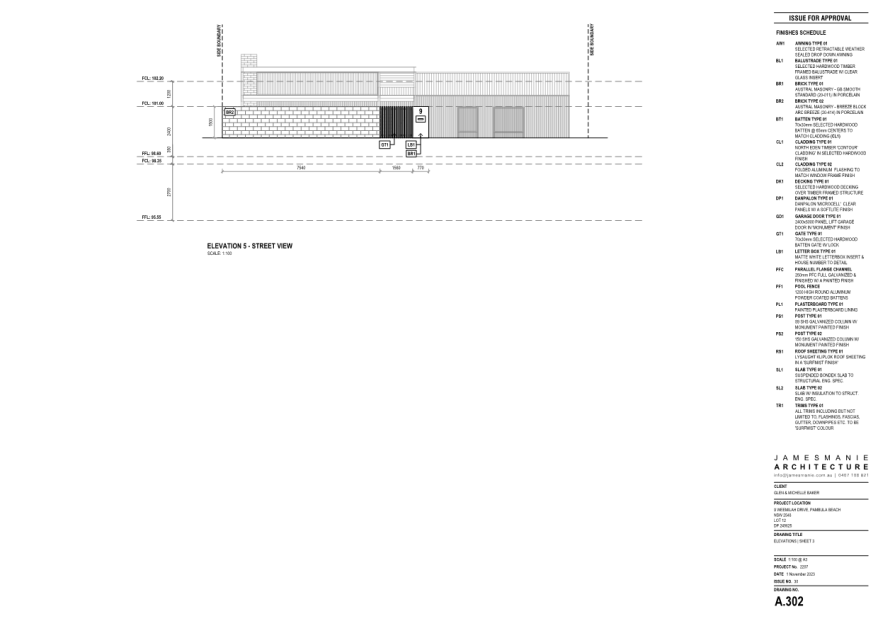

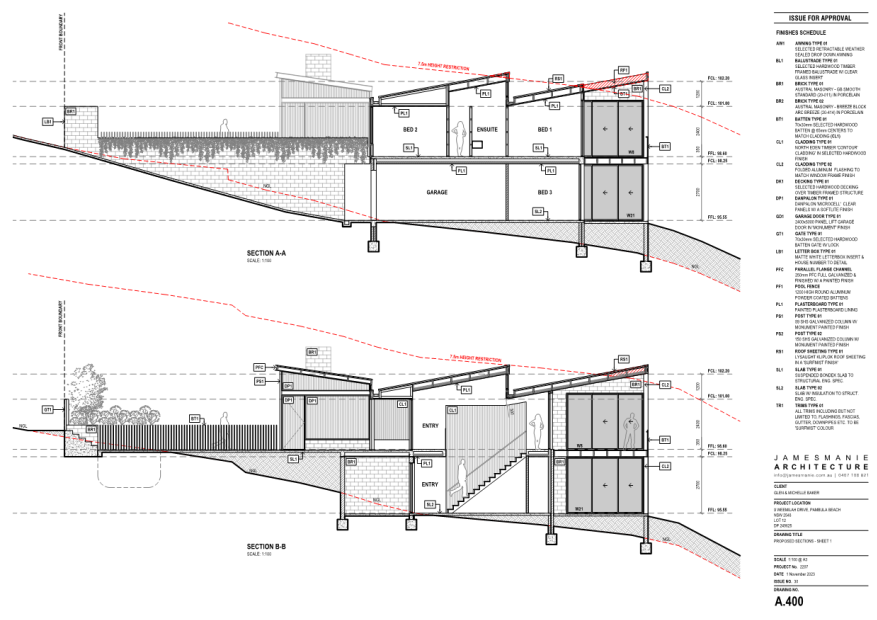

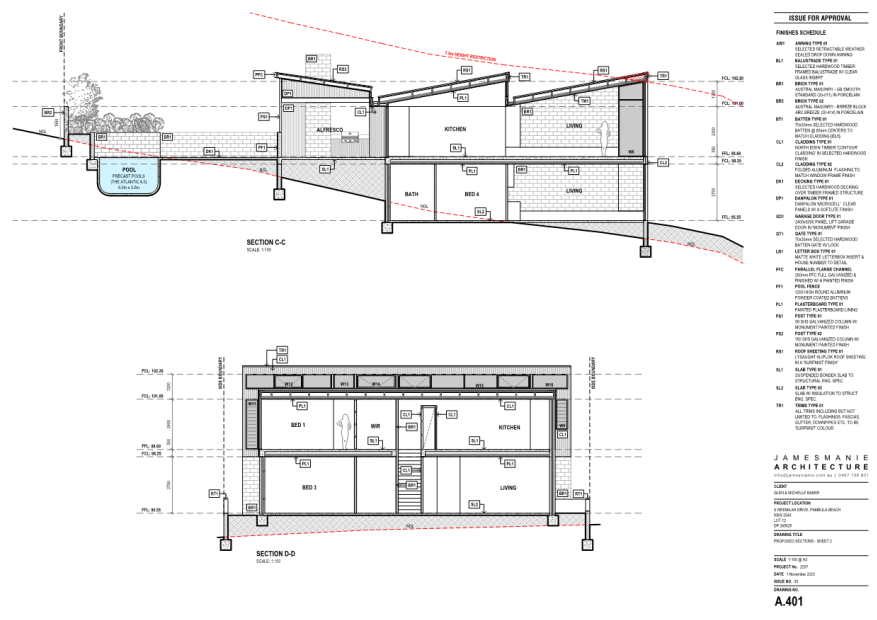

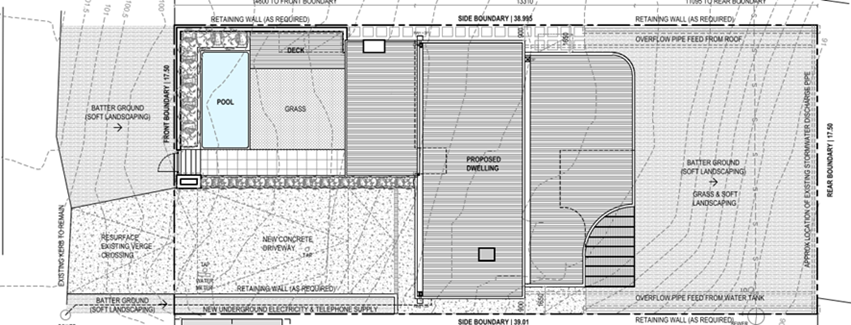

The development site is located on the north-eastern side of Weemilah Drive, Pambula Beach, and is legally described as Lot 12 of DP 249625, 9 Weemilah Drive, Pambula Beach (see Figure 1).

The site is rectangular in shape with a frontage of 17.5 metres (m) and respective depths of 38.995m and 39.01m along the north-western and south-eastern side boundaries. The site has an area of 682.5m², with a north-east/south-west orientation.

The site is zoned R2 Low Density Residential, pursuant to BVLEP 2013 and currently accommodates a part 1-2 storey dwelling house.

The site is devoid of native vegetation and includes a number of shrubs and plantings within the rear third of the site. The front of the site also contains a number of shrubs.

The site experiences a fall of approximately 10m that slopes away from the western front corner towards the eastern rear corner.

The site is environmentally constrained with regard to bushfire hazard. The site is not burdened by any easements or restrictions and is connected to all services.

Figure 1 – Subject site

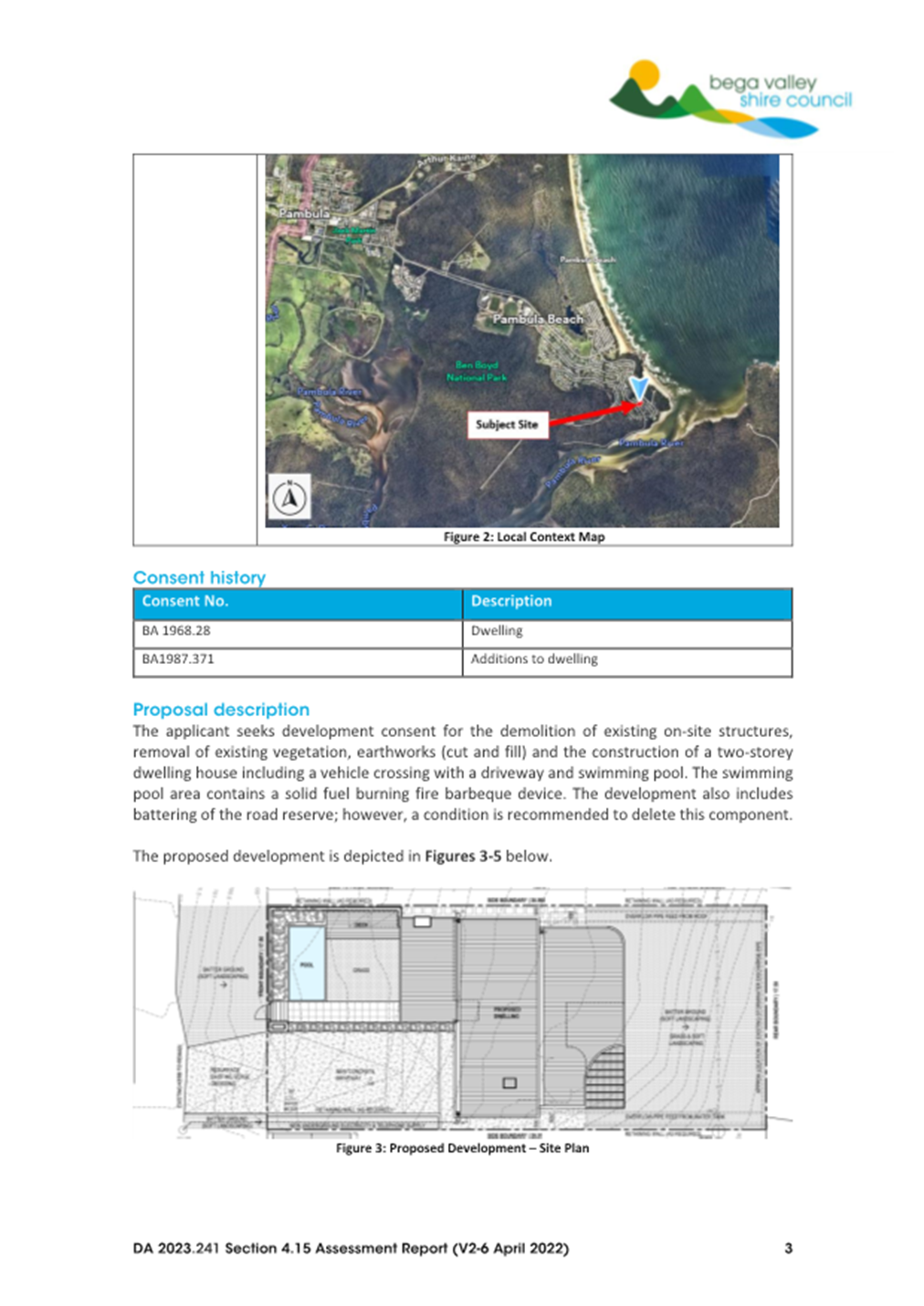

Proposed Development

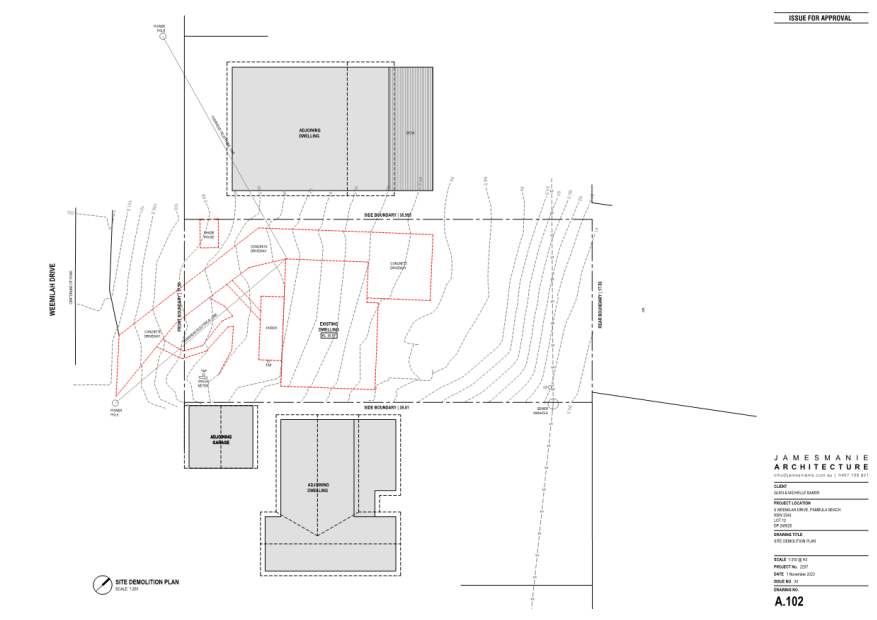

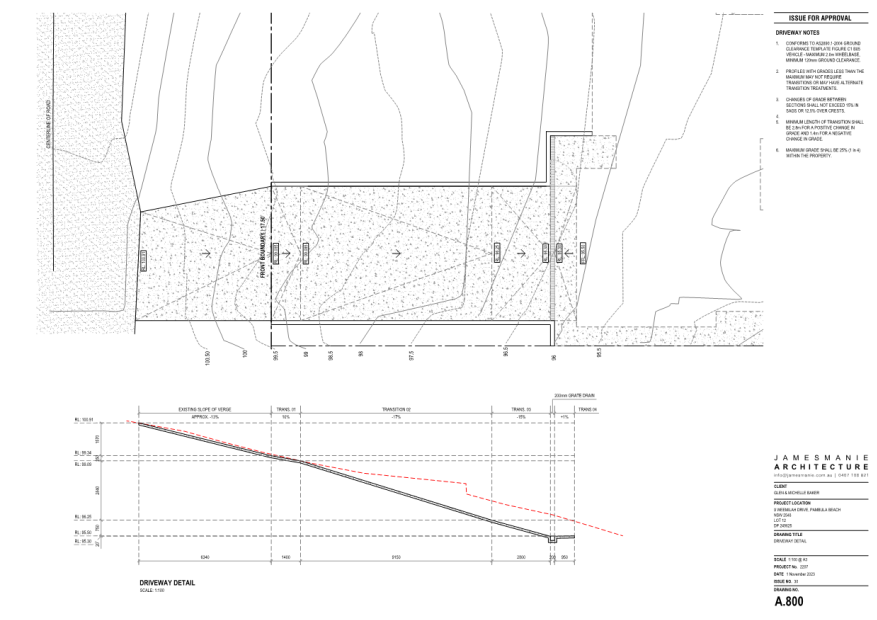

The proposal comprises the construction of a new dwelling house and swimming pool and includes the following:

· Demolition of the existing dwelling house, ancillary structures and concrete driveway

· Earthworks

· Construction of a new two-storey dwelling house

· Site landscaping, including the installation of an in-ground, pre-cast swimming pool

· Site services, driveway access arrangements and other works as documented within this application

(See Figures 2-4 below and Attachment 3)

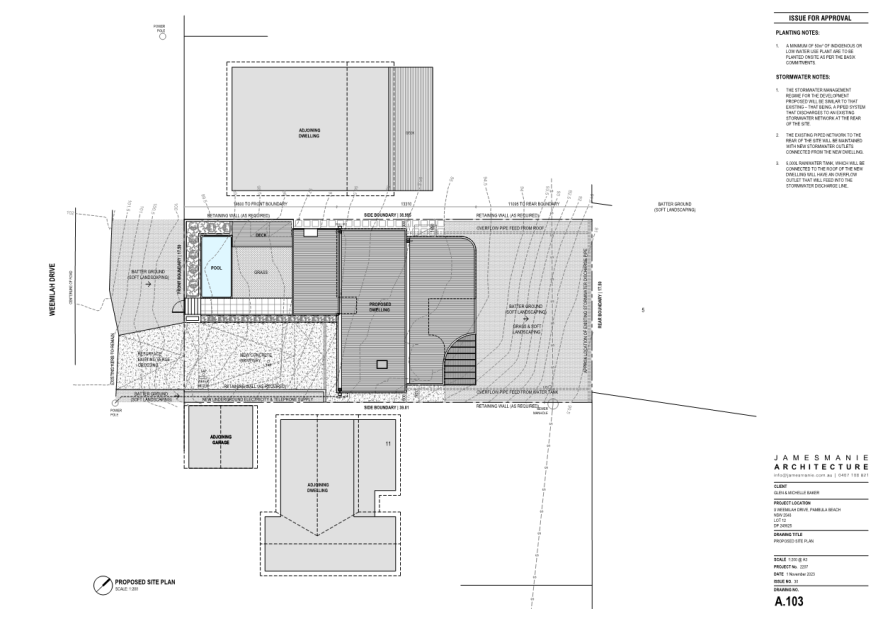

Figure 2: Proposed Development – Site Plan

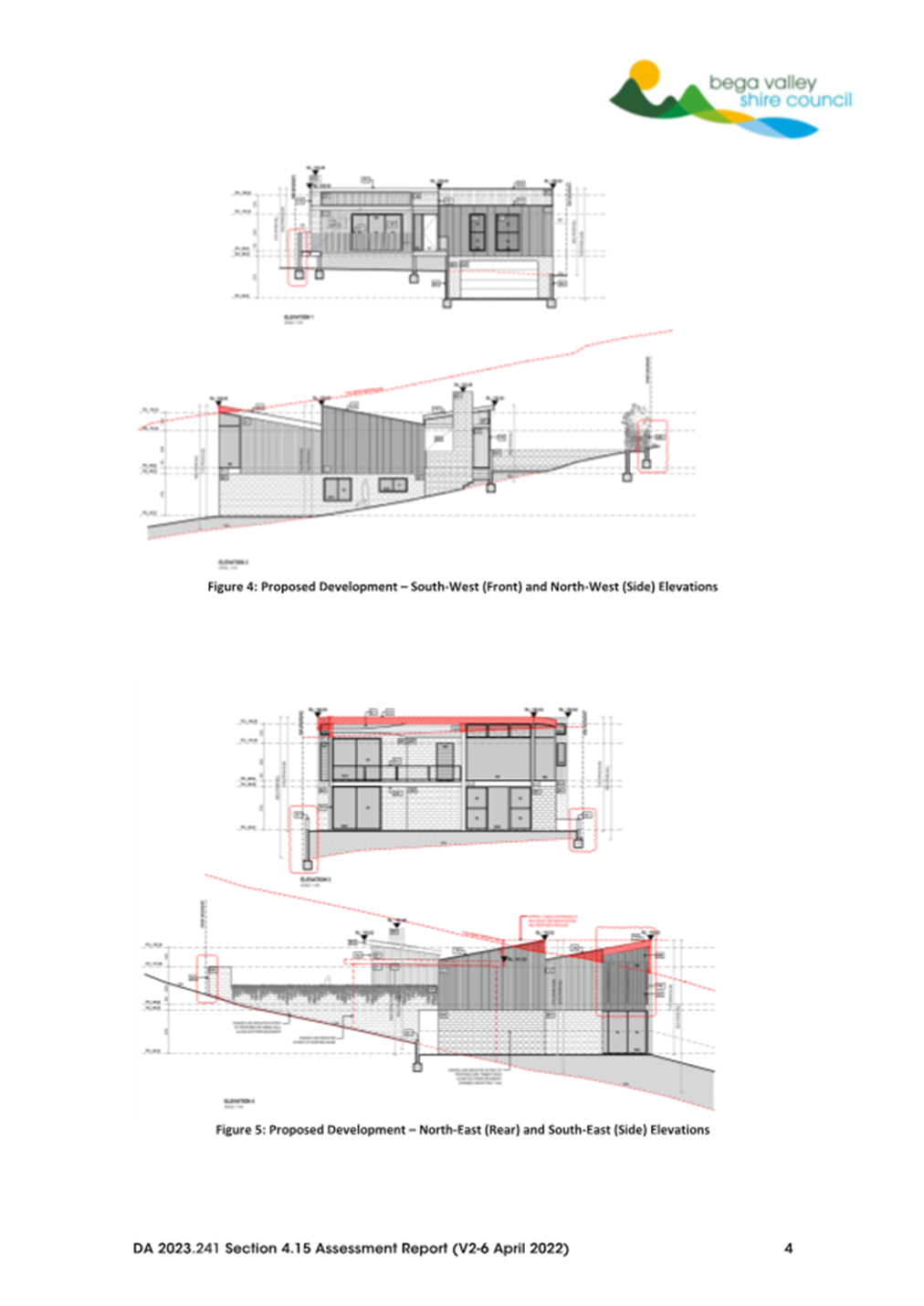

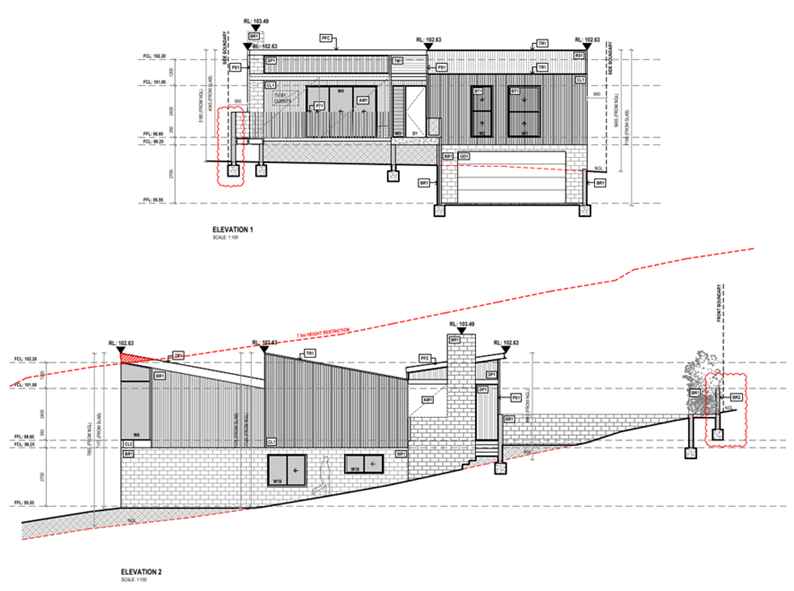

Figure 3: Proposed Development – South-West (Front) and North-West (Side) Elevations

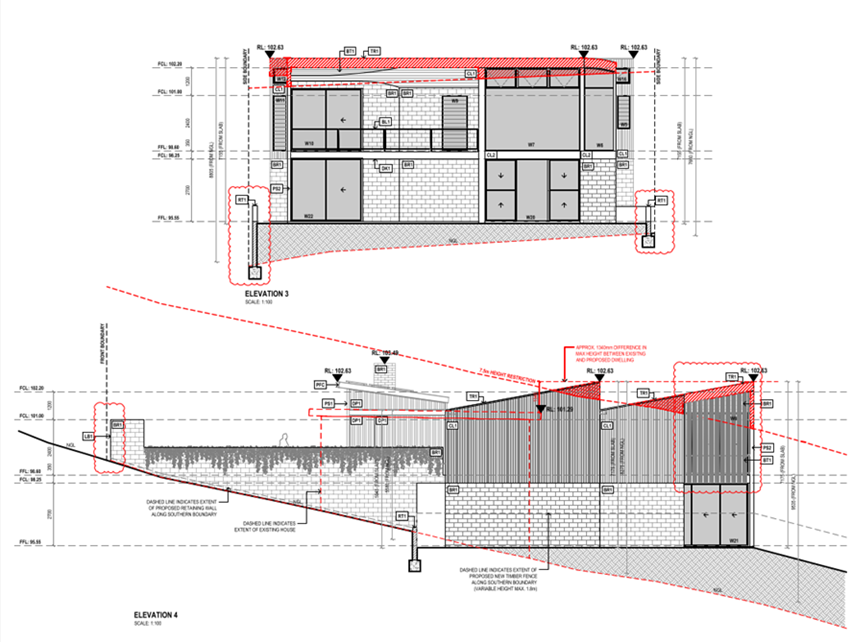

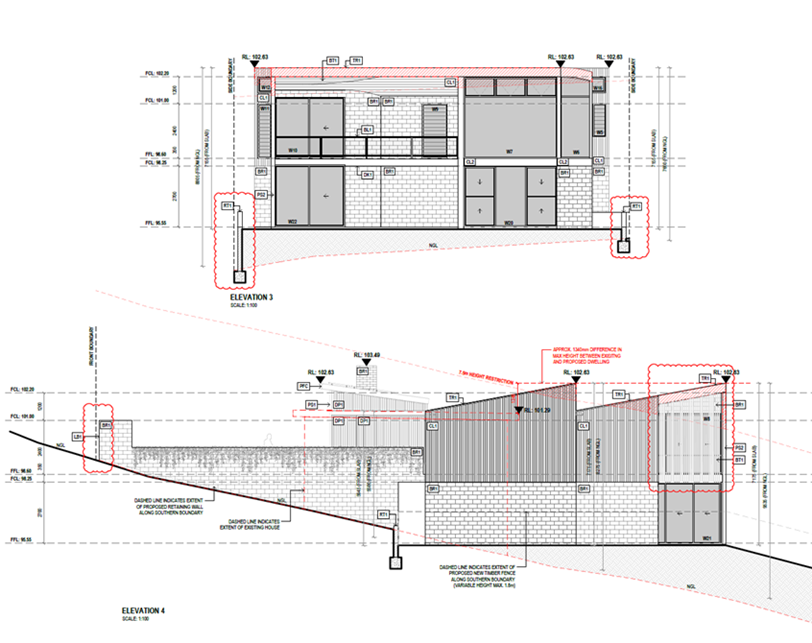

Figure 4: Proposed Development – North-East (Rear) and South-East (Side) Elevations

Planning Assessment

The development application has been assessed in accordance with the matters for consideration under Section 4.15 of the EP&A Act (refer to Attachment 1).

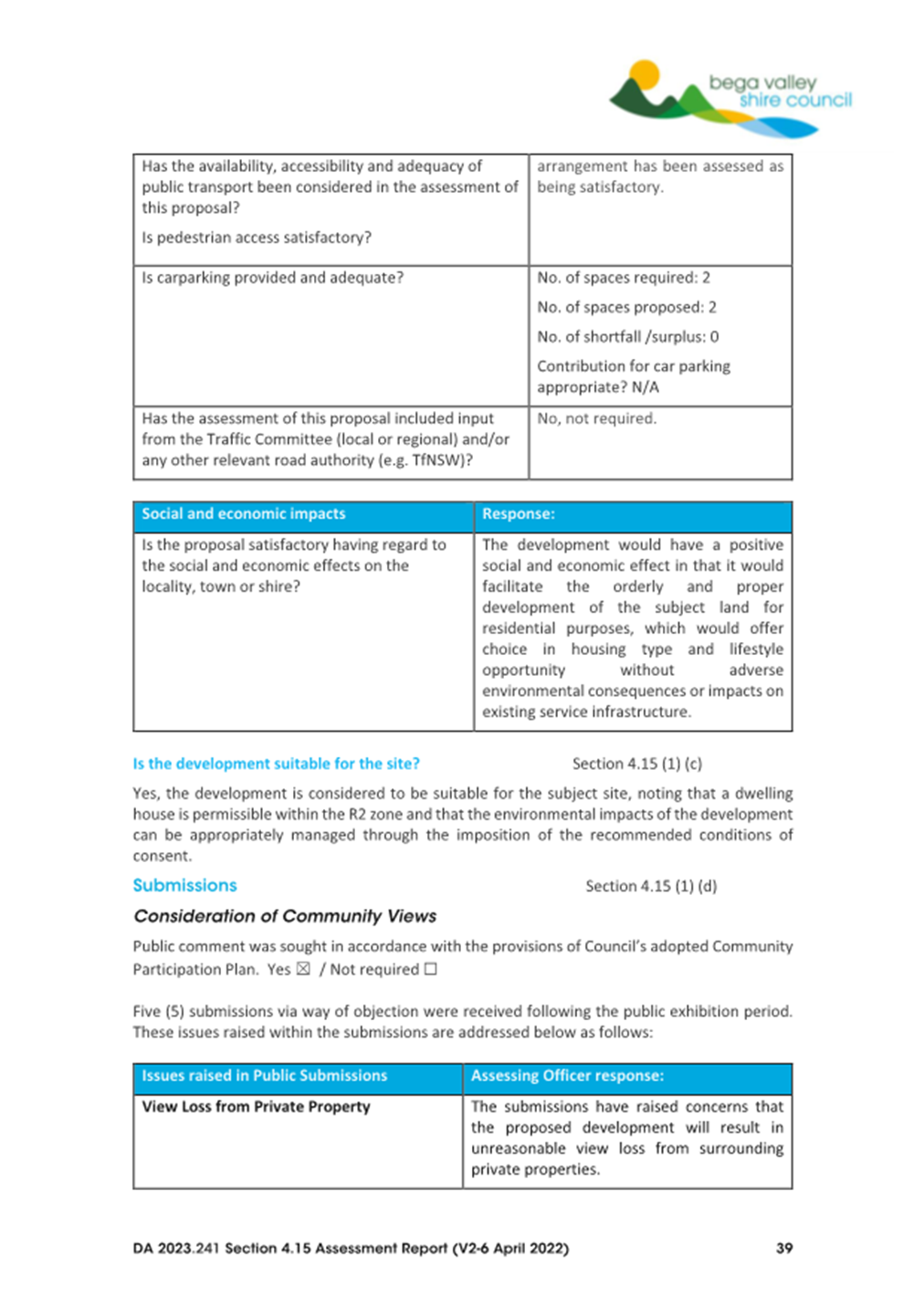

The application was notified for a period of fourteen (14) days. Five (5) submissions by way of objection were received during the exhibition process. The issues raised within the submissions are addressed in detail within Attachment 1 and later within this report.

Planning Assessment

Bega Valley Local Environmental Plan 2013 (BVLEP)

The development has been assessed in accordance with the relevant provisions of the BVLEP.

The land is zoned R2 Low Density Residential under BVLEP 2013. The proposed land use, being for a dwelling house, is permissible with consent within the R2 zone.

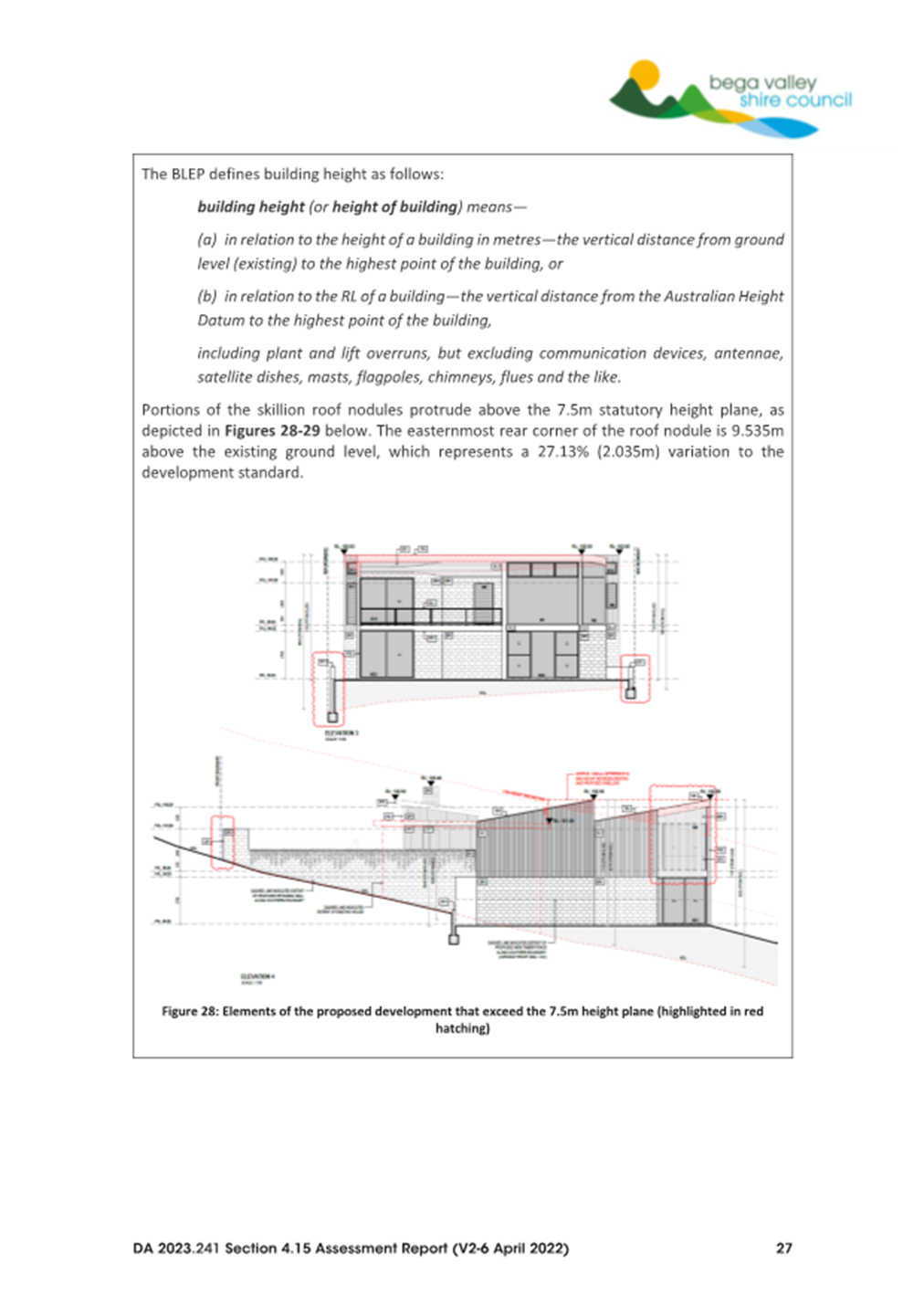

A 7.5m height limit currently applies to the site, which is measured from the existing ground level to the highest point of the building. The BVLEP defines building height as follows:

building height (or height of building) means—

(a) in relation to the height of a building in metres—the vertical distance from ground level (existing) to the highest point of the building, or

(b) in relation to the RL of a building—the vertical distance from the Australian Height Datum to the highest point of the building,

including plant and lift overruns, but excluding communication devices, antennae, satellite dishes, masts, flagpoles, chimneys, flues and the like.

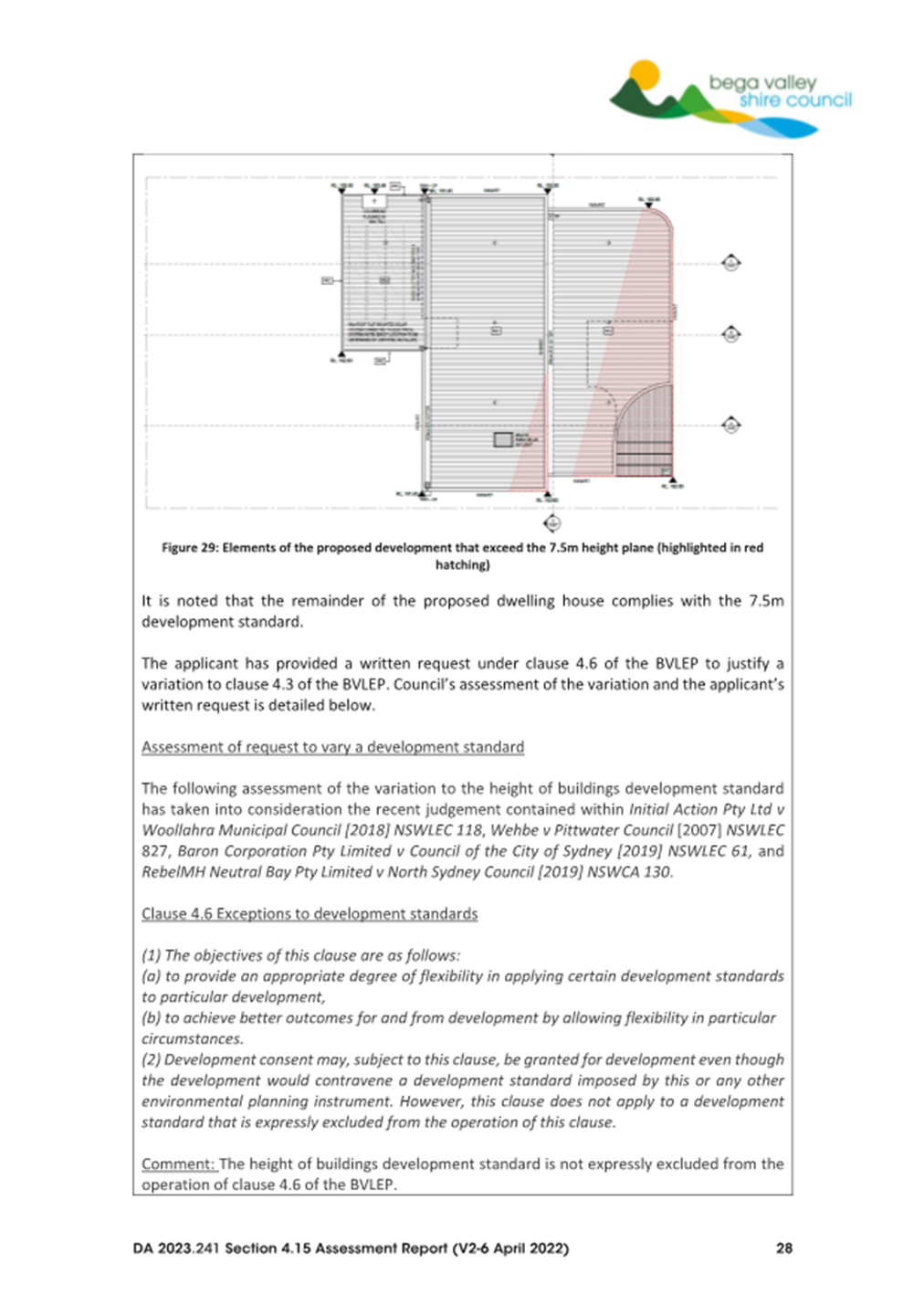

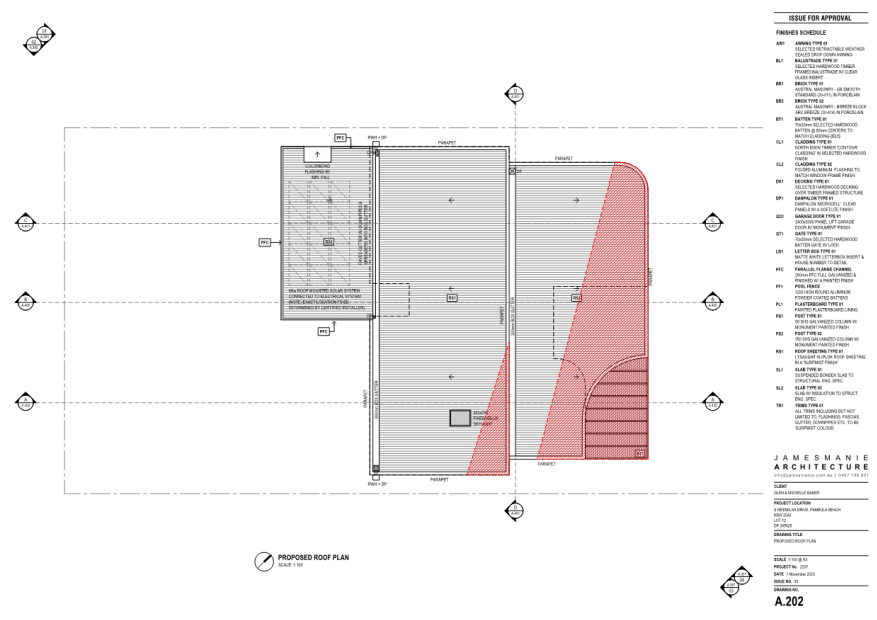

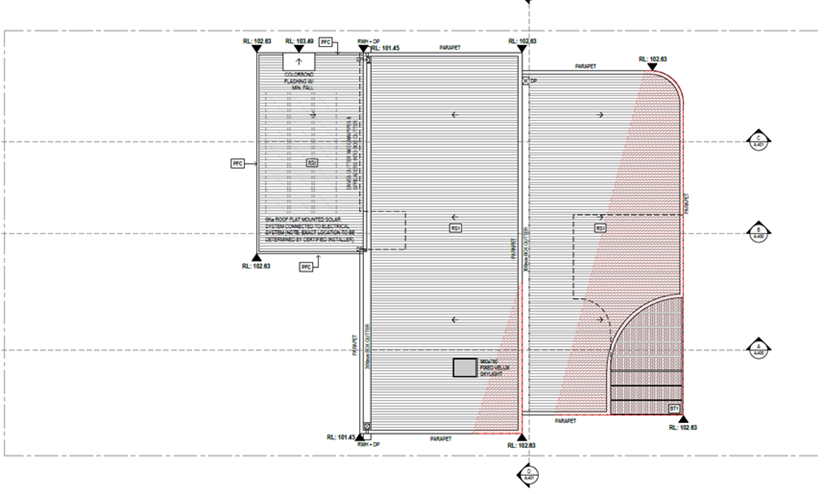

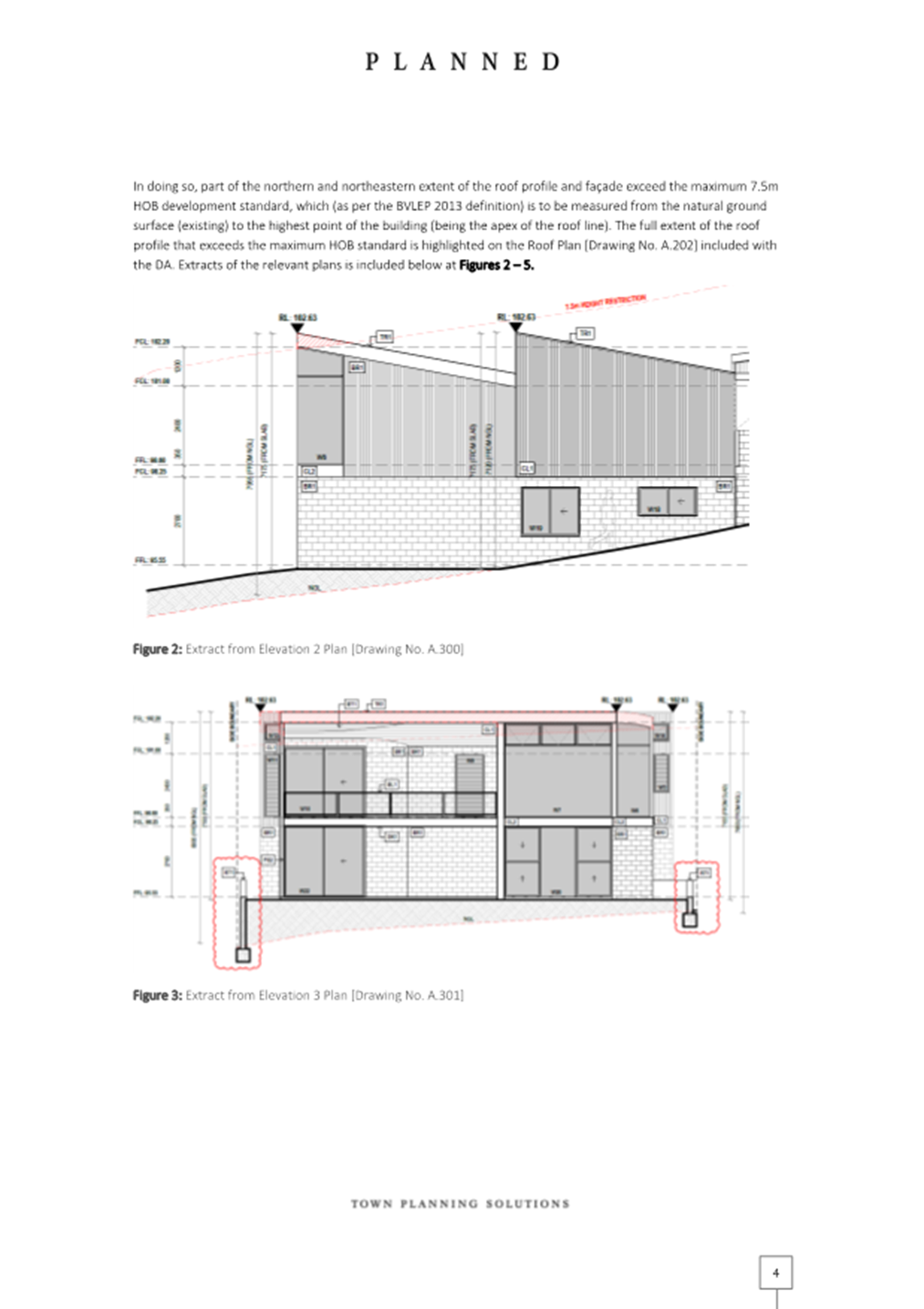

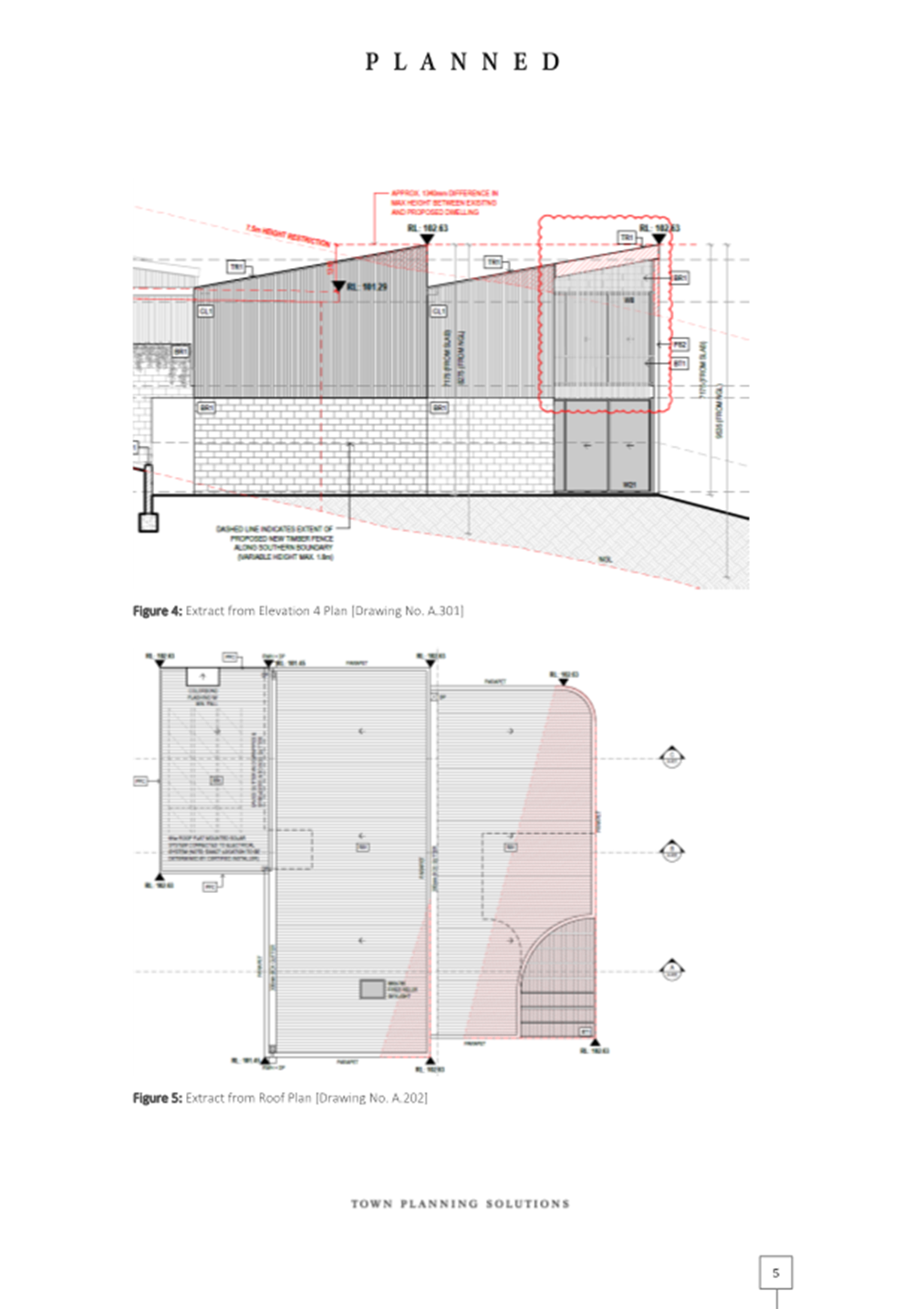

Portions of the proposed development’s skillion roof design protrudes above the 7.5m height limit, representing at its maximum a proposed building height of 9.535m. This represents a maximum 27.13% (2.035m) variation to the development standard.

The elements of the building that exceed the 7.5m height limit are depicted in Figures 5-6 below.

Figure 5: Elements of the proposed development that exceed the 7.5m height plane (highlighted in red hatching)

Figure 6: Elements of the proposed development that exceed the 7.5m height plane (highlighted in red hatching)

Variations to Development Standards under Clause 4.6

The application has been accompanied by a written request under clause 4.6 of the BVLEP 2013 to seek a variation to the development standard (see Attachment 4).

Council, as the consent authority, may consider variations to development standards with the use of clause 4.6 of the BVLEP, provided the proposal:

a) demonstrates that compliance with the development standard is unreasonable and unnecessary in the circumstances of the case, and

b) demonstrates that there are sufficient environmental planning grounds to justify the contravention of the development standard.

Whether compliance with the standard is unreasonable or unnecessary

As outlined within the matter of Wehbe v Pittwater Council [2007] NSWLEC 827, it was established that in order to demonstrate that compliance with the development standard is unreasonable or unnecessary in the circumstances of the case, an applicant must demonstrate either of the following:

• the objectives of the development standard are achieved notwithstanding non-compliance with the standard; or

• the underlying objective or purpose of the standard is not relevant to the development; or

• the underlying objective or purpose would be defeated or thwarted if compliance was required; or

• the standard has been virtually abandoned or destroyed by the Council’s own actions in granting consents departing from the standard; or

• the zoning of land was unreasonable or inappropriate, such that the standards for that zoning are also unreasonable or unnecessary.

The applicant’s written request seeks to satisfy this requirement by demonstrating that the objectives of the development standard are achieved, notwithstanding the non-compliance. The applicant’s justification can be summarised as follows:

• The proposed dwelling house is compatible with the predominant form and scale of surrounding development on the low (north-eastern) side of Weemilah Drive, notwithstanding the height breach.

• The development will not generate any unacceptable residential amenity impacts with respect to overlooking, solar access and view lines and vistas, notwithstanding the height breach.

Council assessment staff concur with the applicant’s justification and conclude that the objectives of the development standard have been achieved for the following reasons:

• Existing development located on the north-eastern side of Weemilah Drive is characterised by 1-2 storey detached dwelling houses. The proposed dwelling house is two storeys in height and presents as a single storey building within the streetscape due to the slope of the land. Furthermore, the height of the development will be consistent with existing residential development on the north-eastern side of Weemilah Drive. For these reasons the development will be appropriate in the context of the predominant form and scale of surrounding development, consistent with objective (a) of clause 4.3 of the BLEP.

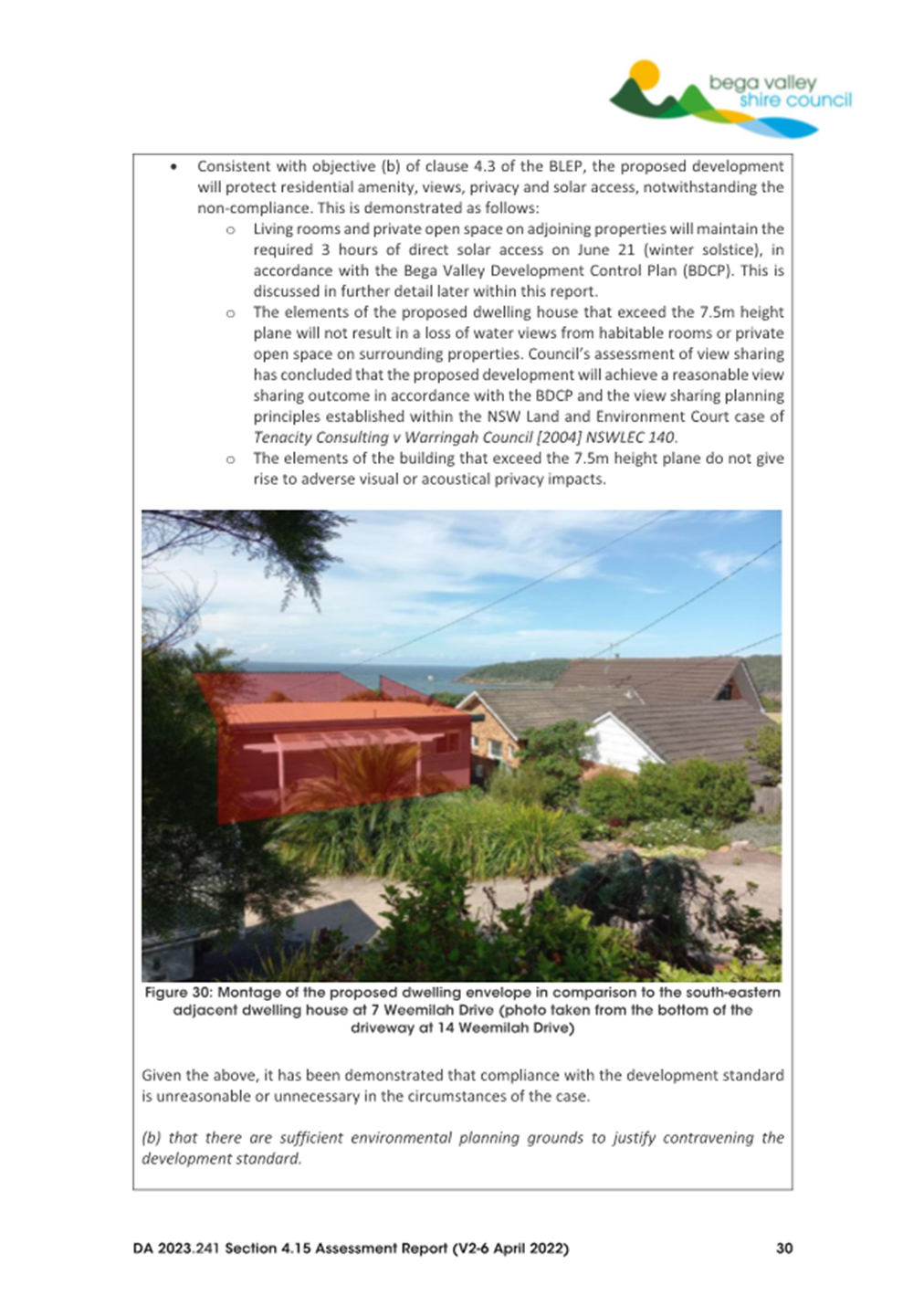

• Consistent with objective (b) of clause 4.3 of the BLEP, the proposed development will protect residential amenity, views, privacy and solar access, notwithstanding the non-compliance. This is demonstrated as follows:

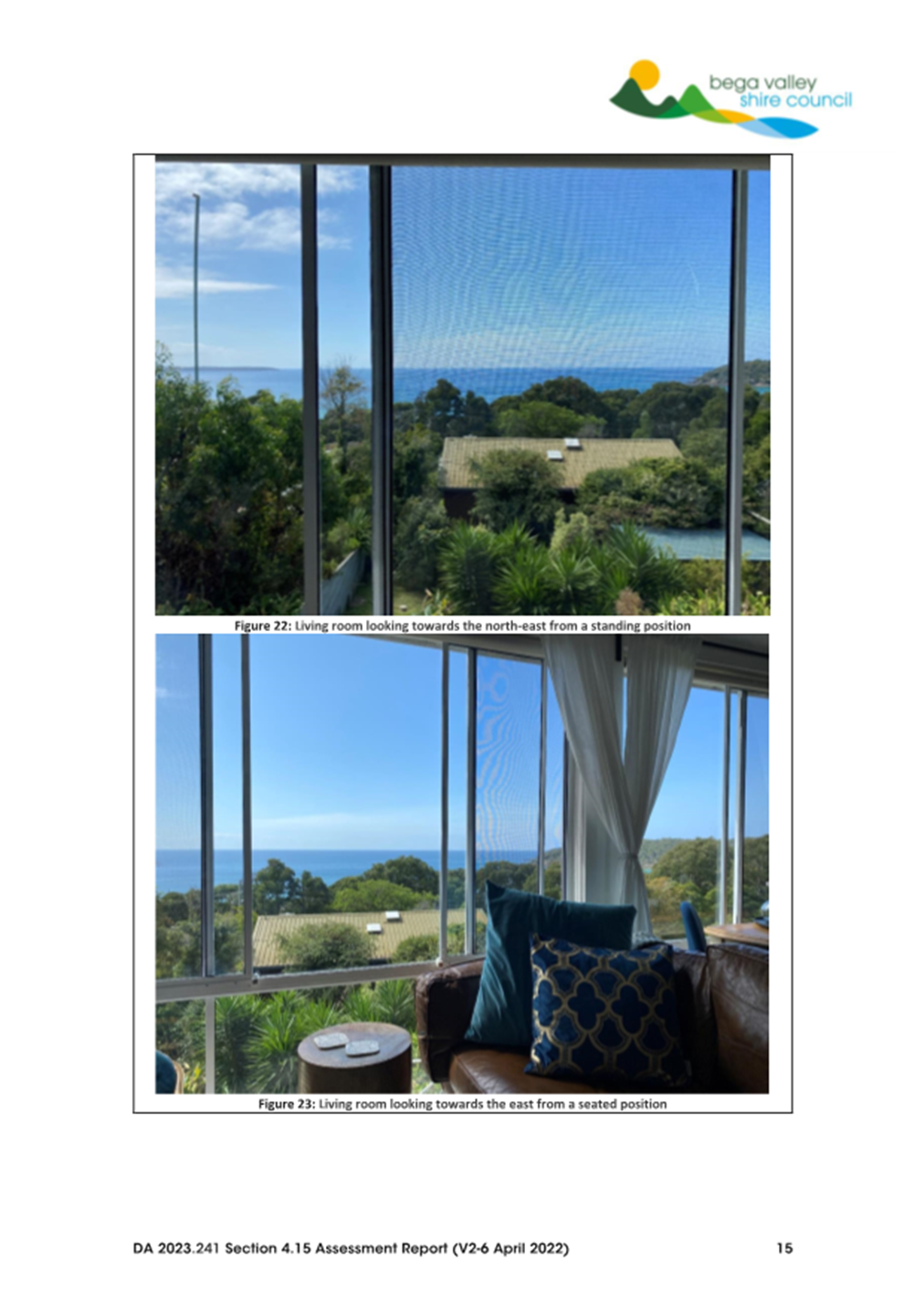

o Living rooms and private open space on adjoining properties will maintain the required 3 hours of direct solar access on June 21 (winter solstice), in accordance with the Bega Valley Development Control Plan 2013 (BVDCP 2013).

o The elements of the proposed dwelling house that exceed the 7.5m height plane will not result in a loss of water views from surrounding properties. Council’s assessment of view sharing has concluded that the proposed development will achieve a reasonable view sharing outcome in accordance with BVDCP 2013 and having regard to the view sharing planning principles established within the NSW Land and Environment Court case of Tenacity Consulting v Warringah Council [2004] NSWLEC 140 (refer to Attachment 2).

o The elements of the building that exceed the 7.5m height plane do not give rise to adverse visual or acoustical privacy impacts.

Given the above, Council assessing staff consider that it has been demonstrated that compliance with the development standard is unreasonable or unnecessary in the circumstances of the case.

Whether there are sufficient environmental planning grounds to justify the contravention of the development standard

In the matter of Initial Action Pty Ltd v Woollahra Municipal Council [2018] NSWLEC 118, Preston CJ provides the following guidance (ref: paragraph 23) to inform the consent authority’s finding that the applicant’s written request has adequately demonstrated that there are sufficient environmental planning grounds to justify contravening the development standard:

‘As to the second matter required by clause 4.6(3)(b), the grounds relied on by the applicant in the written request under cl 4.6 must be “environmental planning grounds” by their nature: see Four2Five Pty Ltd v Ashfield Council [2015] NSWLEC 90 at [26]. The adjectival phrase “environmental planning” is not defined but would refer to grounds that relate to the subject matter, scope and purpose of the EPA Act, including the objects in section 1.3 of the EPA Act.’

Section 1.3 of the Environmental Planning and Assessment Act 1979 (EP&A Act) reads as follows:

(a) to promote the social and economic welfare of the community and a better environment by the proper management, development and conservation of the State’s natural and other resources,

(b) to facilitate ecologically sustainable development by integrating relevant economic, environmental and social considerations in decision-making about environmental planning and assessment,

(c) to promote the orderly and economic use and development of land,

(d) to promote the delivery and maintenance of affordable housing,

(e) to protect the environment, including the conservation of threatened and other species of native animals and plants, ecological communities and their habitats,

(f) to promote the sustainable management of built and cultural heritage (including Aboriginal cultural heritage),

(g) to promote good design and amenity of the built environment,

(h) to promote the proper construction and maintenance of buildings, including the protection of the health and safety of their occupants,

(i) to promote the sharing of the responsibility for environmental planning and assessment between the different levels of government in the State,

(j) to provide increased opportunity for community participation in environmental planning and assessment.

The applicant has submitted that the following site-specific environmental planning grounds to justify the variation to the height of buildings development standard:

• The proposed height variation is deemed to be minor given the context of the site.

• The proposed height variation will not generate any unacceptable adverse environmental impacts in respect of overlooking, overshadowing or view loss.

• Notwithstanding the proposed height variation, the development proposed remains consistent with the objectives of the height of buildings development standard and the R2 Low Density Residential Zone.

• The breach of building height relates to part of the north and north-eastern extent of the roof profile and façade, and directly relates to the existing ground surface levels and the proposed siting of the replacement dwelling, being closer to the rear boundary than that existing. In this instance, the levels drop substantially towards the northern (rear) boundary and the south-eastern (side) boundary and as such, it is the corresponding roof profile and part of the façade that breach the maximum building height.

• On the basis that the proposed height variation relates directly to the existing ground surface levels, the variation is noted to be variable – ranging between 0.160m up to 2.035m, equating to a variable non-compliance of between 2.13% and 27.13%.

• The siting of the proposed replacement dwelling has been deliberate so as to facilitate a compliant driveway gradient to the new attached garage and to rationalise the extent of earthworks. This outcome is deemed to be superior as it removes the long existing concrete driveway extending along the north-western property boundary and to the rear of the existing dwelling – accessing the ‘rear loaded’ garage from internal to the site. The increased front setback also allows for vehicles to be parked on the driveway in front of the garage, which is important noting that on-street parking is not available along most of Weemilah Drive due to its narrow reserve width of only 4.5m – 5m.

• The proposed height variation is not a deliberate attempt by the proponent to solely maximise views. Rather, the proposed roof profile and design has been used to create a modern, decorative element to the uppermost portion of the dwelling and to maximise daylight and sunlight penetration into the interior proportions of the dwelling. This is based on limiting window exposure to the adjoining neighbours to the northwest and southeast and by angling the roof profile to maximise north and north-eastern exposure.

• The development proposed will be without adverse environmental consequence and/or impact on existing service infrastructure.

Council assessing staff generally concur with the environmental planning grounds advanced by the applicant to justify the non-compliance. In particular, Council staff agree that:

• The height breach is only limited to portions of the roof nodules and the elements of building that exceed the height plane do not result in adverse environmental amenity impacts in terms of overlooking, overshadowing, visual bulk and view loss.

• The height exceedance is partially driven by the slope of the land, which slopes away from the front boundary towards the rear.

• The elements of the dwelling that exceed the height plane allow for the maximisation of sunlight as the highlight windows with a north-eastern aspect are included on the breaching elements of the building.

In this regard, the applicant’s written request has demonstrated that the proposed development is an orderly and economic use and development of the land, and that the structure is of a good design that will reasonably protect and improve the amenity of the surrounding built environment, thereby satisfying sections 1.3 (c) and (g) of the EP&A Act 1979.

Therefore, the applicant's written request has adequately demonstrated that there are sufficient environmental planning grounds to justify contravening the development standard as required by clause 4.6(3)(b).

Bega Valley Local Development Control Plan 2013 (BVDCP 2013)

The development has been assessed in accordance with the relevant sections of the BVDCP 2013. The relevant sections are detailed in Attachment 1. The development is considered to meet the relevant sections of the BVDCP 2013, subject to the recommended conditions contained within Attachment 2.

Options

1. Approve the development application subject to the conditions of consent provided in Attachment 2. This is the recommended option.

2. Defer consideration of the matter and request a separate report identifying any relevant Section 4.15 matters for consideration and draft reasons for refusal.

3. Defer consideration of the matter and seek an alternative design that complies with the provisions of BVLEP 2013 height of building.

Community and Stakeholder Engagement

Engagement undertaken

The development application was notified to adjacent and adjoining owners for 14 days in accordance with Council’s Community Participation Plan (which forms part of Council’s Community Engagement Strategy) from 24 November 2023 to 8 December 2023. The application received 5 submissions during the notification period.

A copy of each submission has been provided to Councillors via the Councillor portal.

The issues raised are detailed in the Assessment Report included as Attachment 1 of this report. The key issues raised in the submissions include:

• View loss from private property

• Building height non-compliance

• Retaining Wall / Battering of the site

• Stormwater management

• Overshadowing of adjoining properties

• Overlooking of adjoining properties

• Removal of boundary fencing

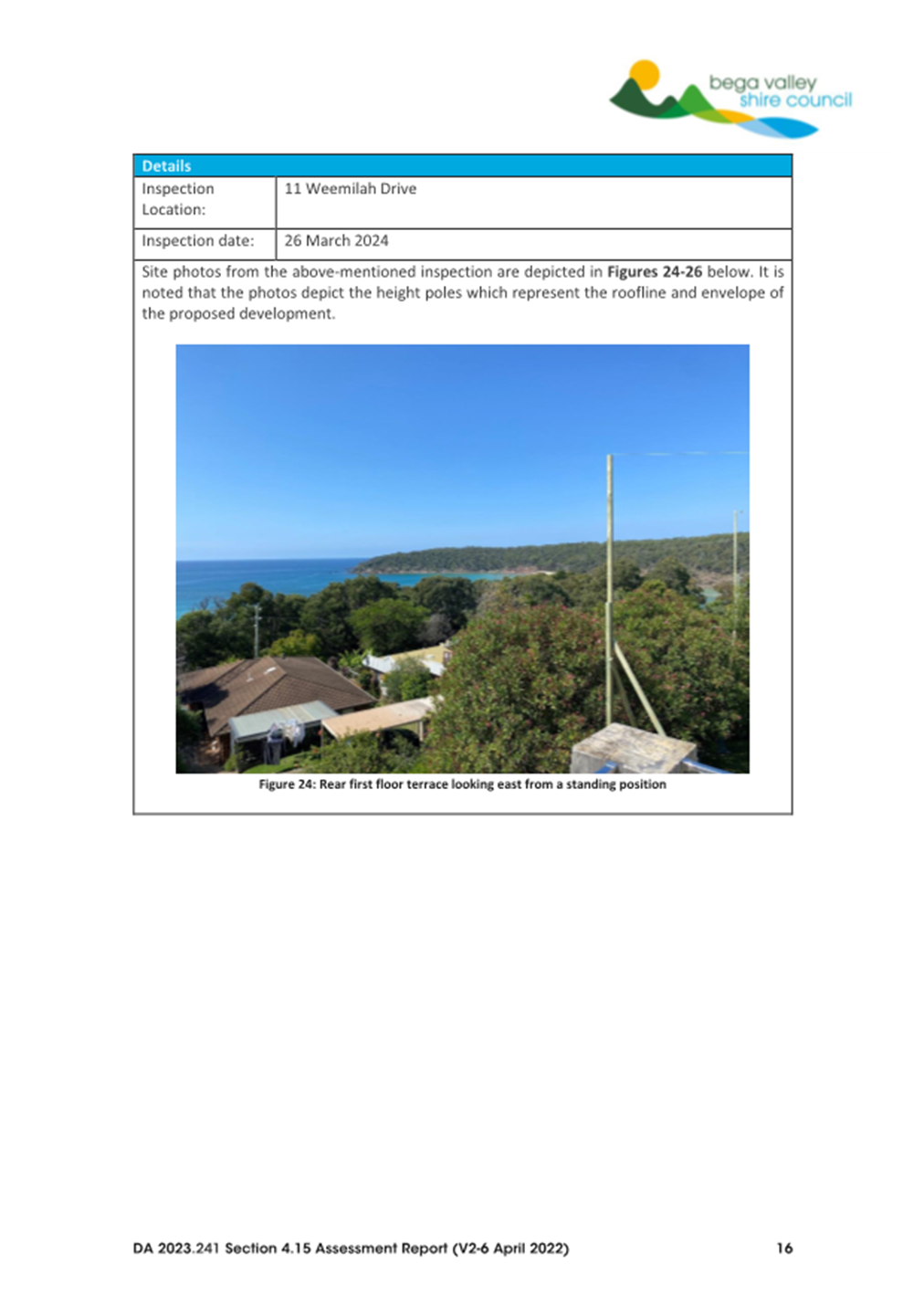

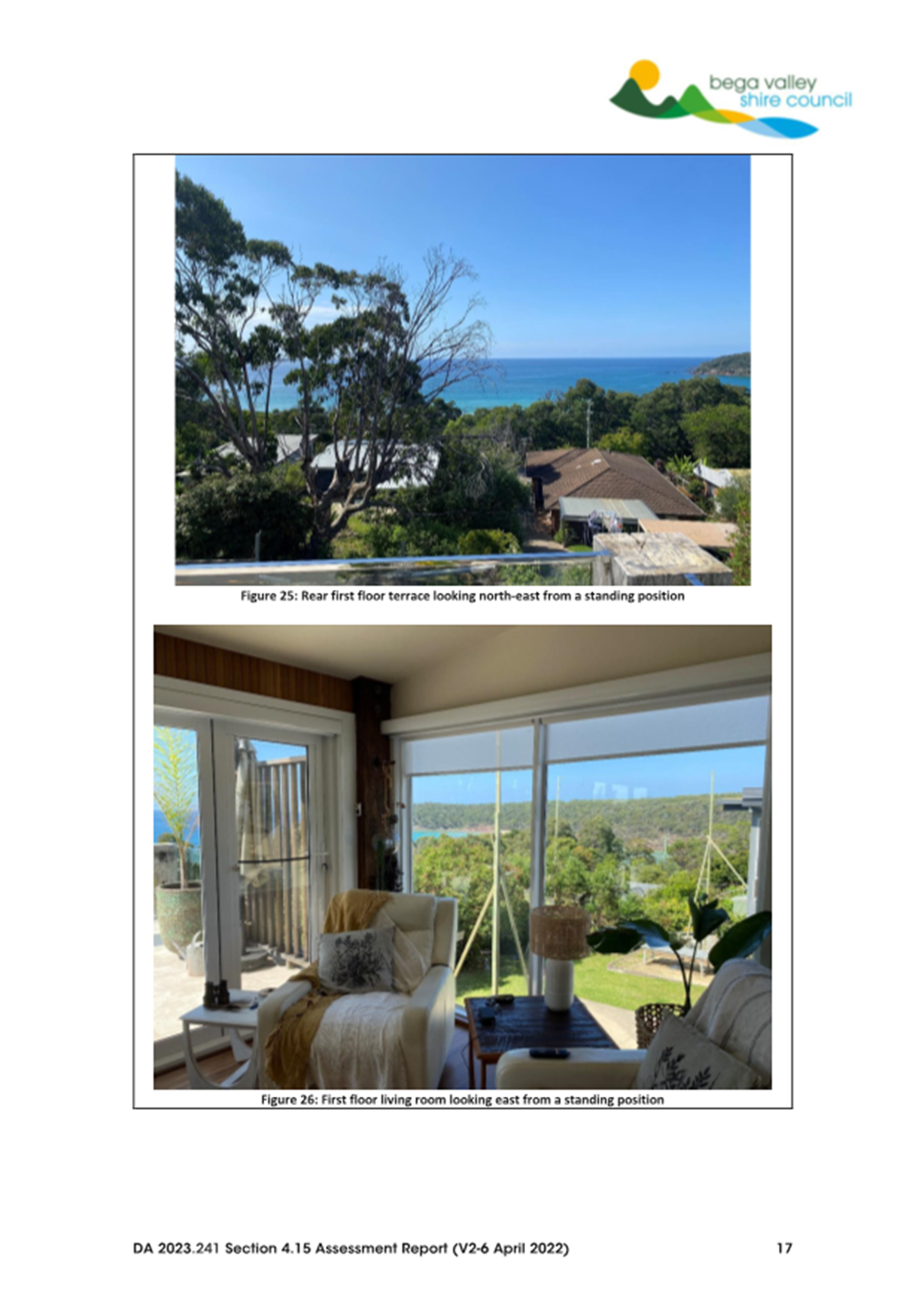

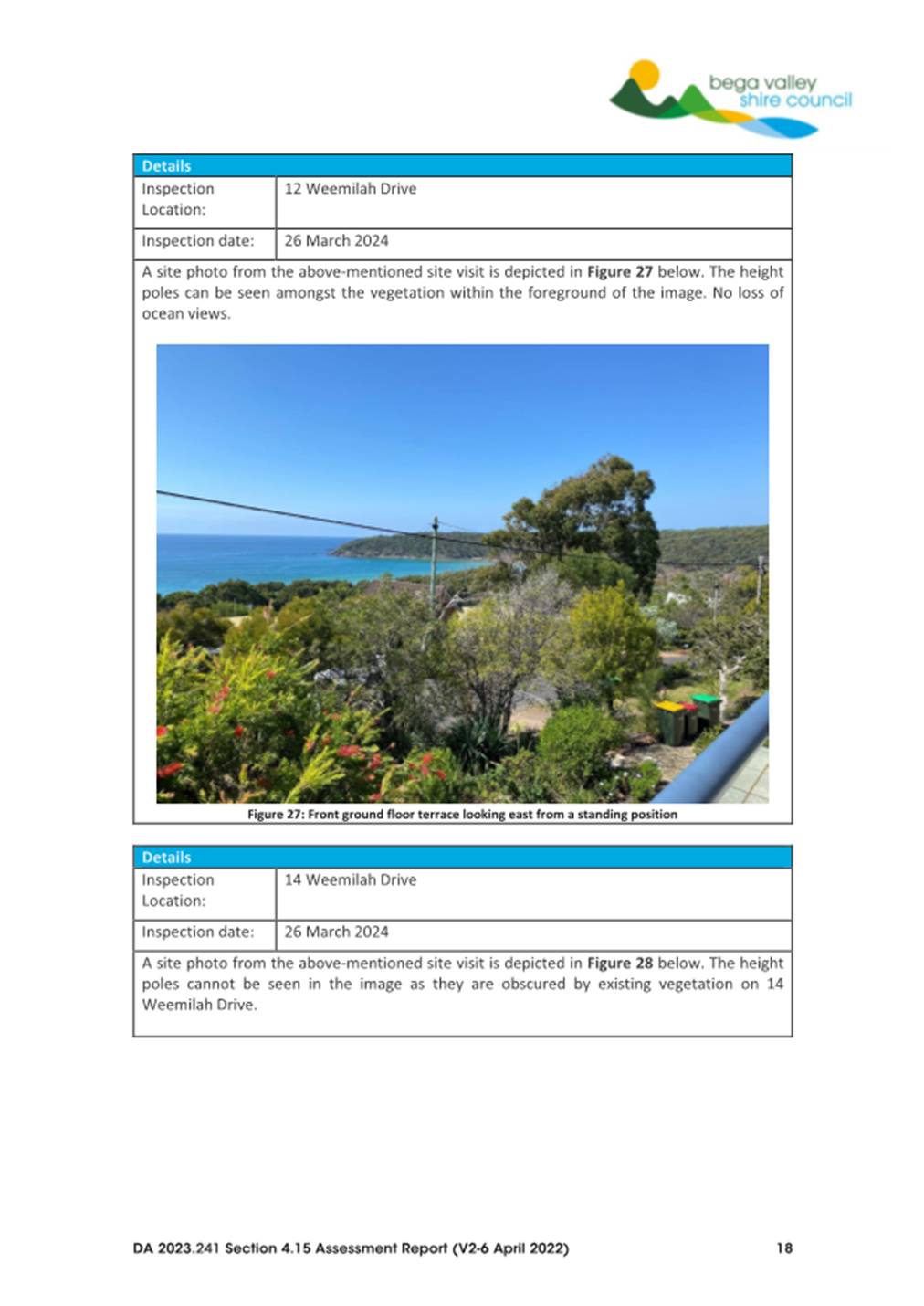

Inspections were undertaken from the premises who submitted submissions to review issues associated with view loss from private property, building height non-compliance, overshadowing and overlooking of adjoining properties.

Upon site inspections and consideration of the applicable matters detailed under BVLEP 2013 and BVDCP 2013, it is assessed that the matters raised within the public submissions are not considered to be of a significance that would warrant refusal of the development application or a further redesign. It is noted that suitable conditions have been recommended where appropriate to resolve various issues, in particular those pertaining to the retaining walls and battering of the site, stormwater management, overlooking and the retention of boundary fencing.

The impacts in relation to the building height non-compliance, view loss from private properties and overshadowing of adjoining properties are assessed as being acceptable.

Stakeholder Engagement

The development has also been referred to Essential Energy for review and comment.

Essential Energy have raised no objections in relation to the development and have provided a number of recommendations, which are included as recommended conditions of consent which are proposed to be included.

Engagement planned

All those persons who made submissions will be notified of the determination of the development application.

Financial and Resource Considerations

Assessing proposals for development is part of the regular business of Council and resourcing to undertake this function is included in Council’s adopted budget.

Legal /Policy

Should Council resolve to refuse the application, the applicant has appeal rights to the Land and Environment Court under the provisions of the Environmental Planning and Assessment Act 1979.

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

The development will provide for the housing needs of the community within a low-density residential environment.

Environment and Climate Change

This application, if approved, will not have any additional adverse impacts on the environment or climate change with the development meeting the provisions of State Environmental Planning Policy (Sustainable Buildings) 2022. Any vegetation required to be removed would be existing landscaped gardens.

Economic

The impacts of the development on the economy are considered minor. It is considered that utilising the same building footprint, is not the best economic use of the land, as envisaged by the Residential Land Strategy and therefore the proposed development is suitable for the reasons outlined in this report.

Risk

The assessment of development is a core function of Council. There are no material impacts on Council’s operations associated with determination of the proposed development. Refusal of the development application could be subject to an appeal in the Land and Environment Court, which would have cost implications to defend Council’s position.

Social / Cultural

This application, if approved, will improve the existing housing stock within the Bega Valley Shire.

Attachments

1⇩. Section 4.15 Assessment Report

2⇩. Draft Conditions of Consent

3⇩. Proposed Development Plans

4⇩. Clause 4.6 Variation to Height Request from Applicant

|

27 November 2024 |

|

|

Item 8.1 - Attachment 4 |

Clause 4.6 Variation to Height Request from Applicant |

|

Item 8.2 |

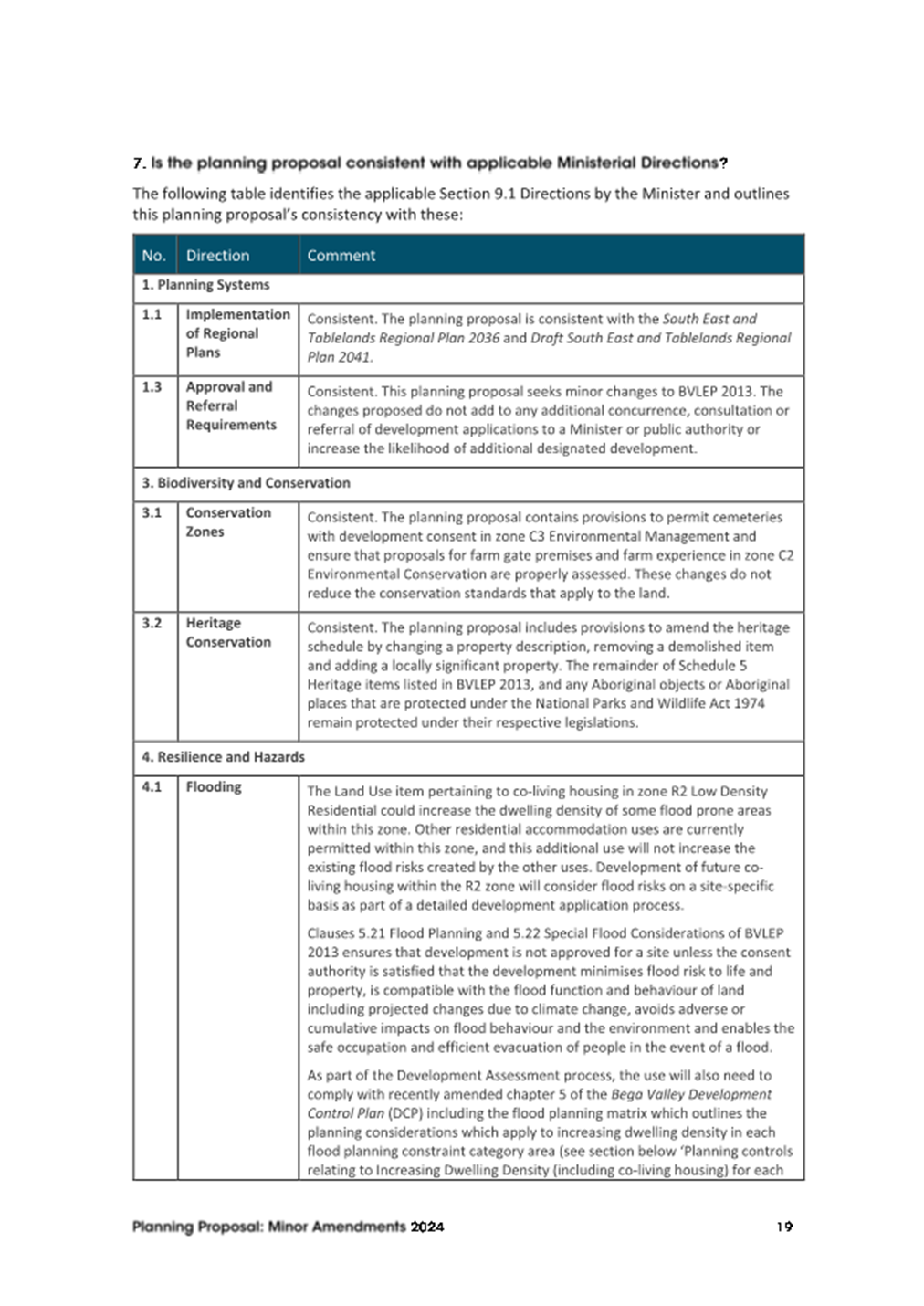

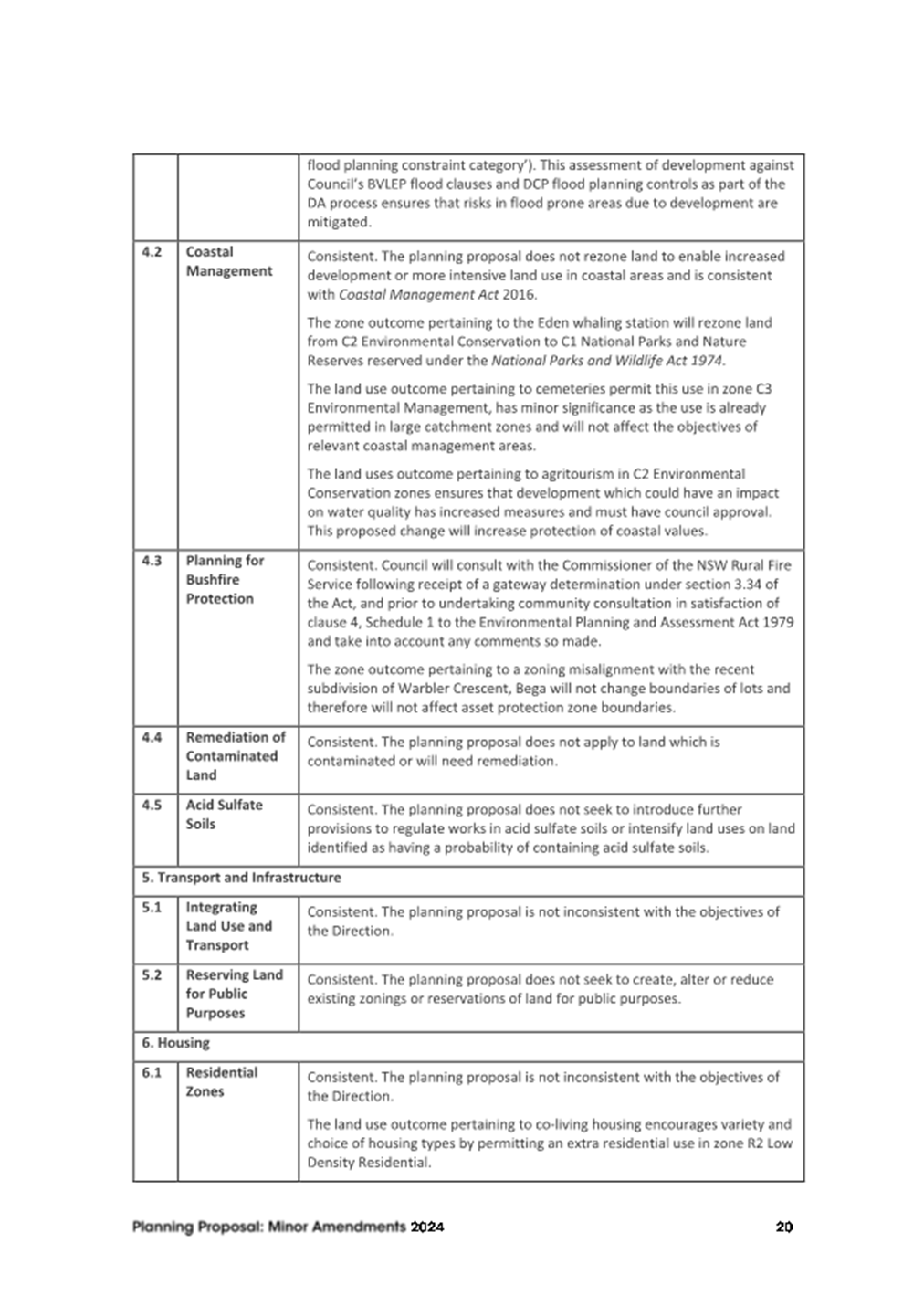

8.2. Endorsement of Minor Amendments Planning Proposal

This report seeks a resolution of Council to support a planning proposal for minor amendments to the Bega Valley Local Environmental Plan 2013.

Director Community Environment and Planning

That Council:

1. Support a planning proposal to implement several minor amendments to the Bega Valley Local Environmental Plan 2013.

2. Authorise Council officers to submit the planning proposal (Attachment 1) and supporting information to the Department of Planning, Housing and Infrastructure requesting a Gateway Determination under Section 3.34 of the Environmental Planning and Assessment Act 1979.

3. Authorise Council officers, subject to the conditions of the Gateway Determination (including public exhibition) and providing no substantial changes to the planning proposal are required and no objections are received during exhibition, to progress the planning proposal to finalisation and gazettal without a further report to Council.

Executive Summary

This report seeks Council’s resolution to support a planning proposal to make minor amendments to the Bega Valley Local Environmental Plan 2013 (BVLEP 2013). These proposed amendments have no significant or strategic impact and are considered suitable for inclusion in a ‘minor amendments’ planning proposal.

This Council initiated planning proposal (Attachment 1) results from the need to amend BVLEP 2013 to update references, correct omissions and make several minor administrative amendments regarding:

· property references and zones

· permissible uses and approval pathways

· the heritage schedule

· changes to clauses to protect the environment, amenity and character.

Background

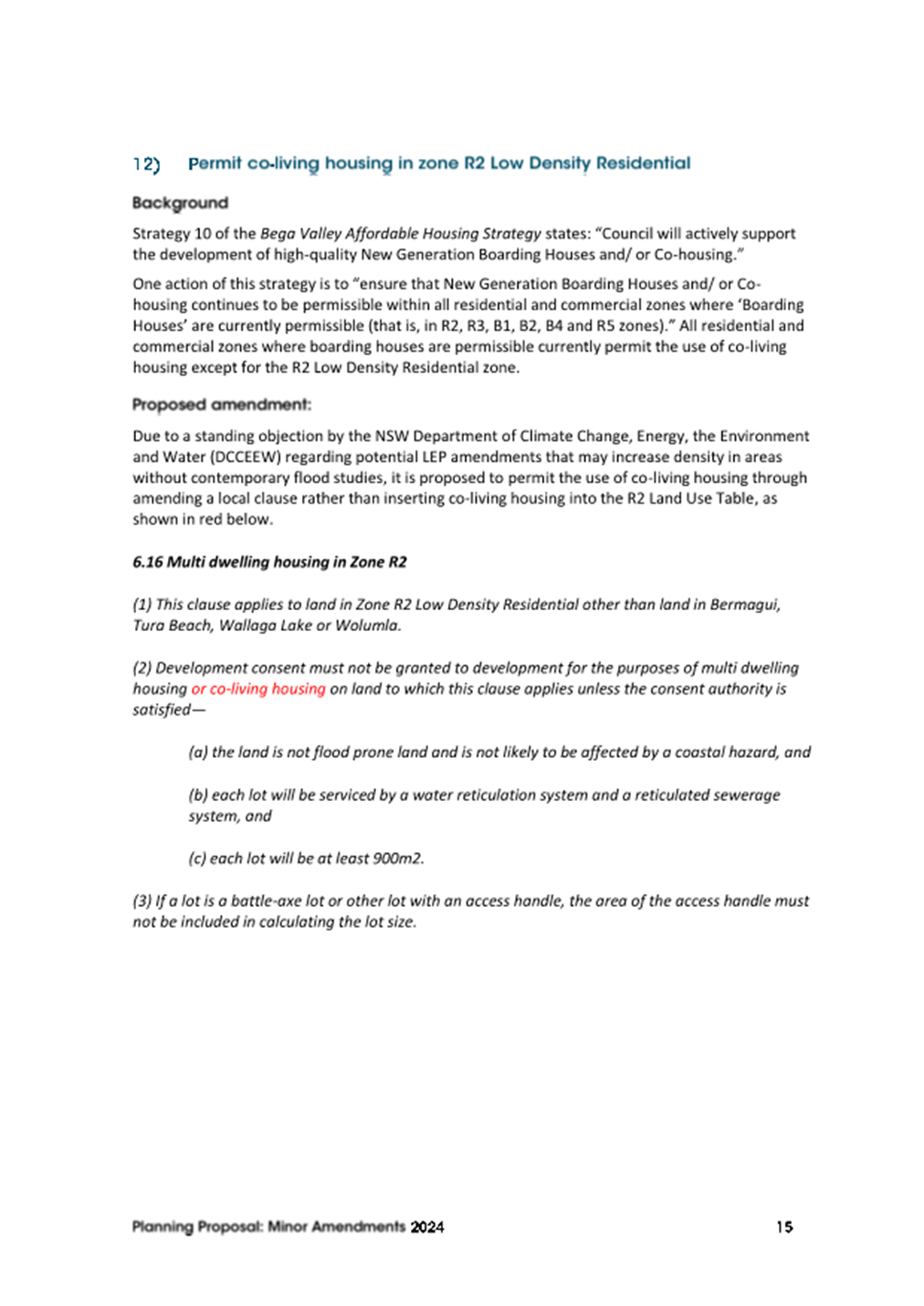

The planning proposal aims to:

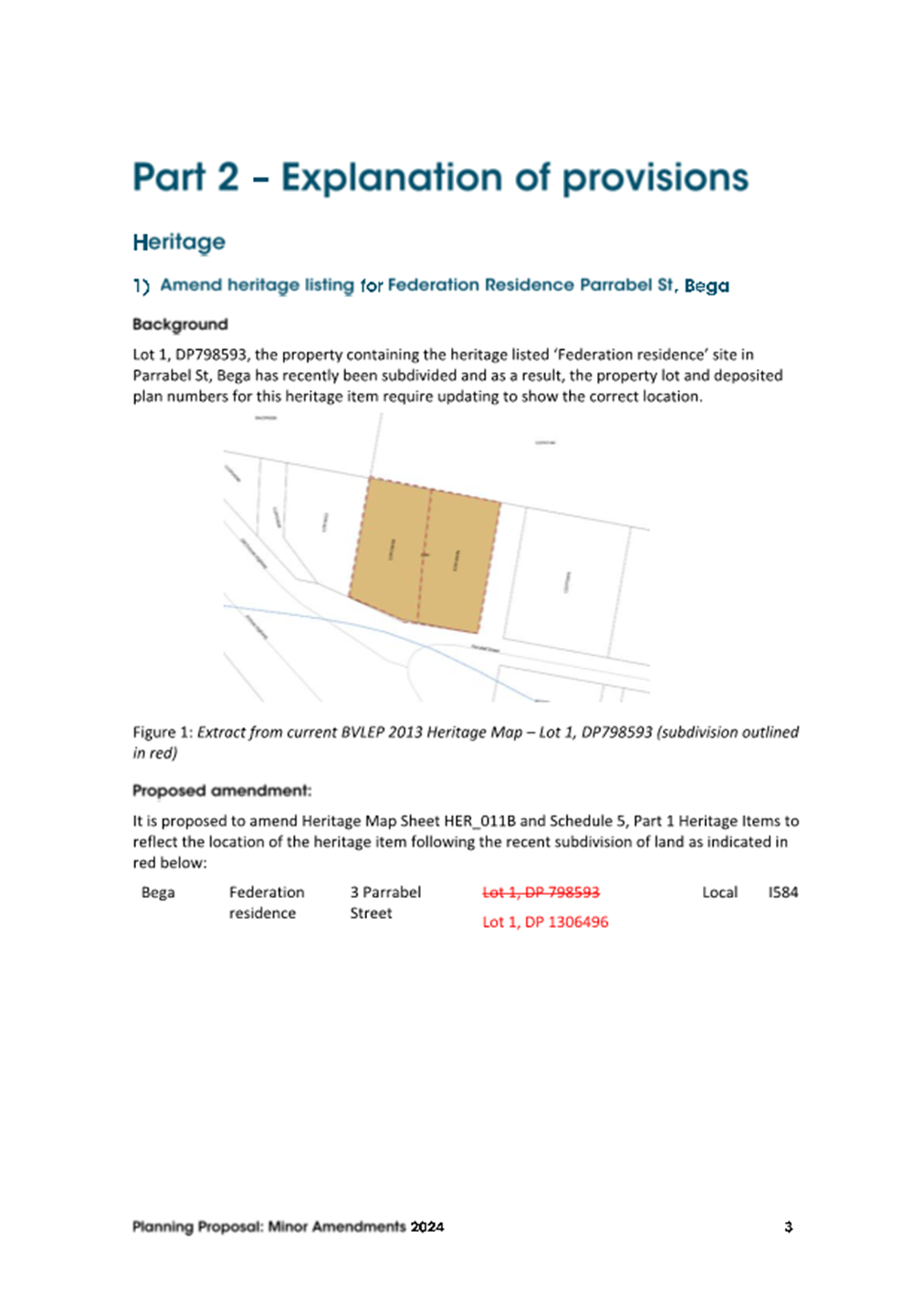

1. Amend the property description for a heritage listing at Parrabel St, Bega due to subdivision of land

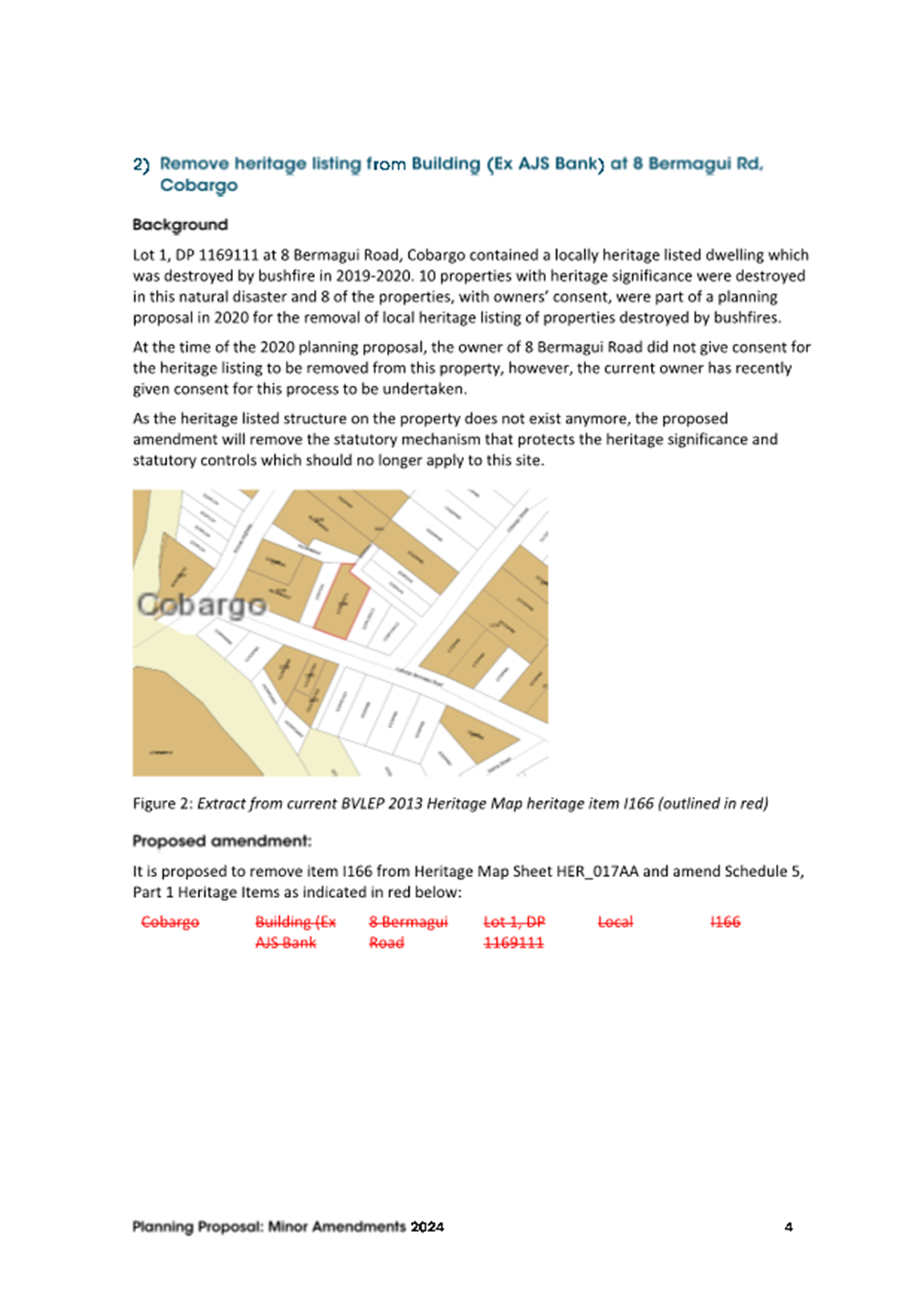

2. Remove a heritage listing from 8 Bermagui Rd, Cobargo due to demolition

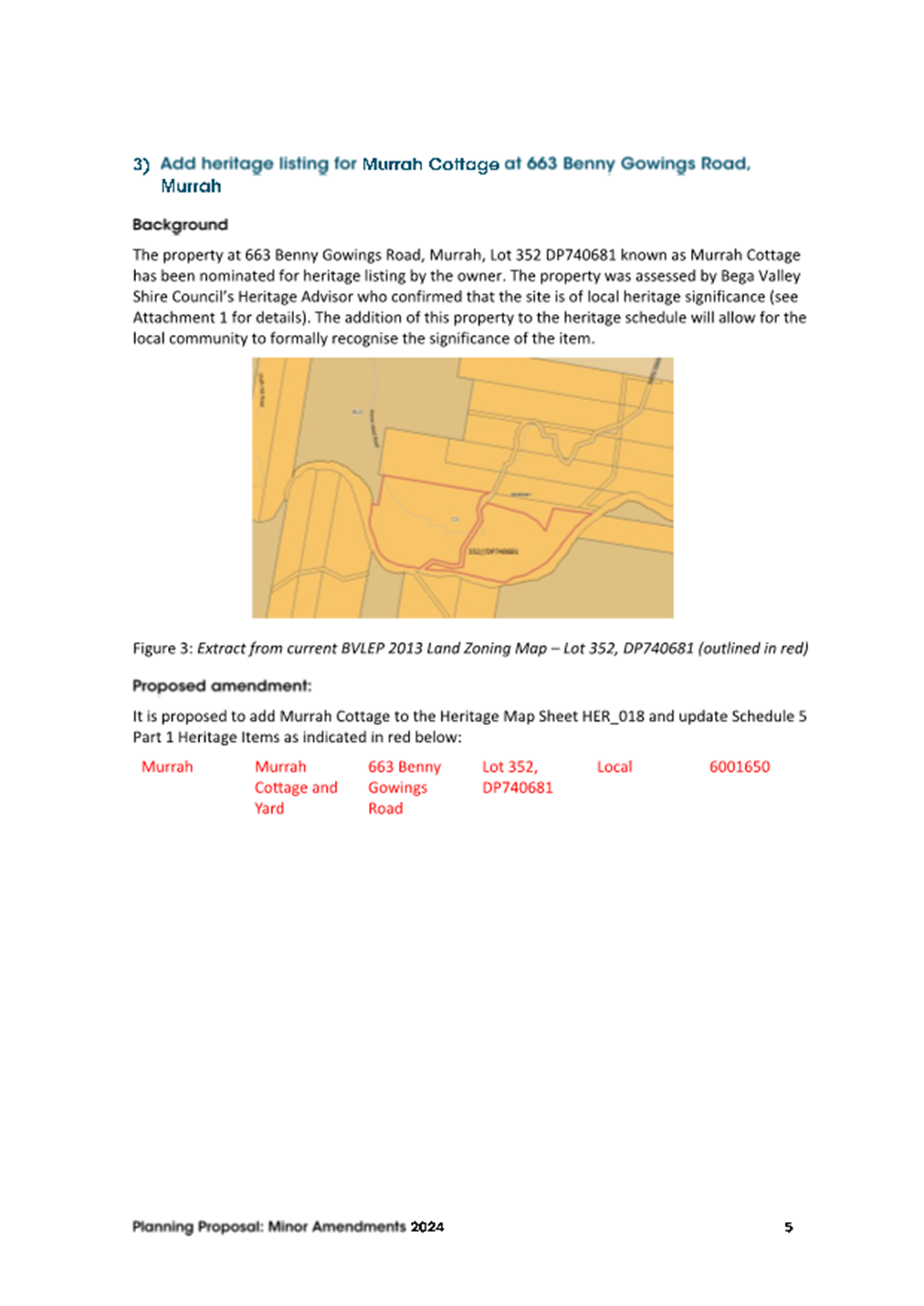

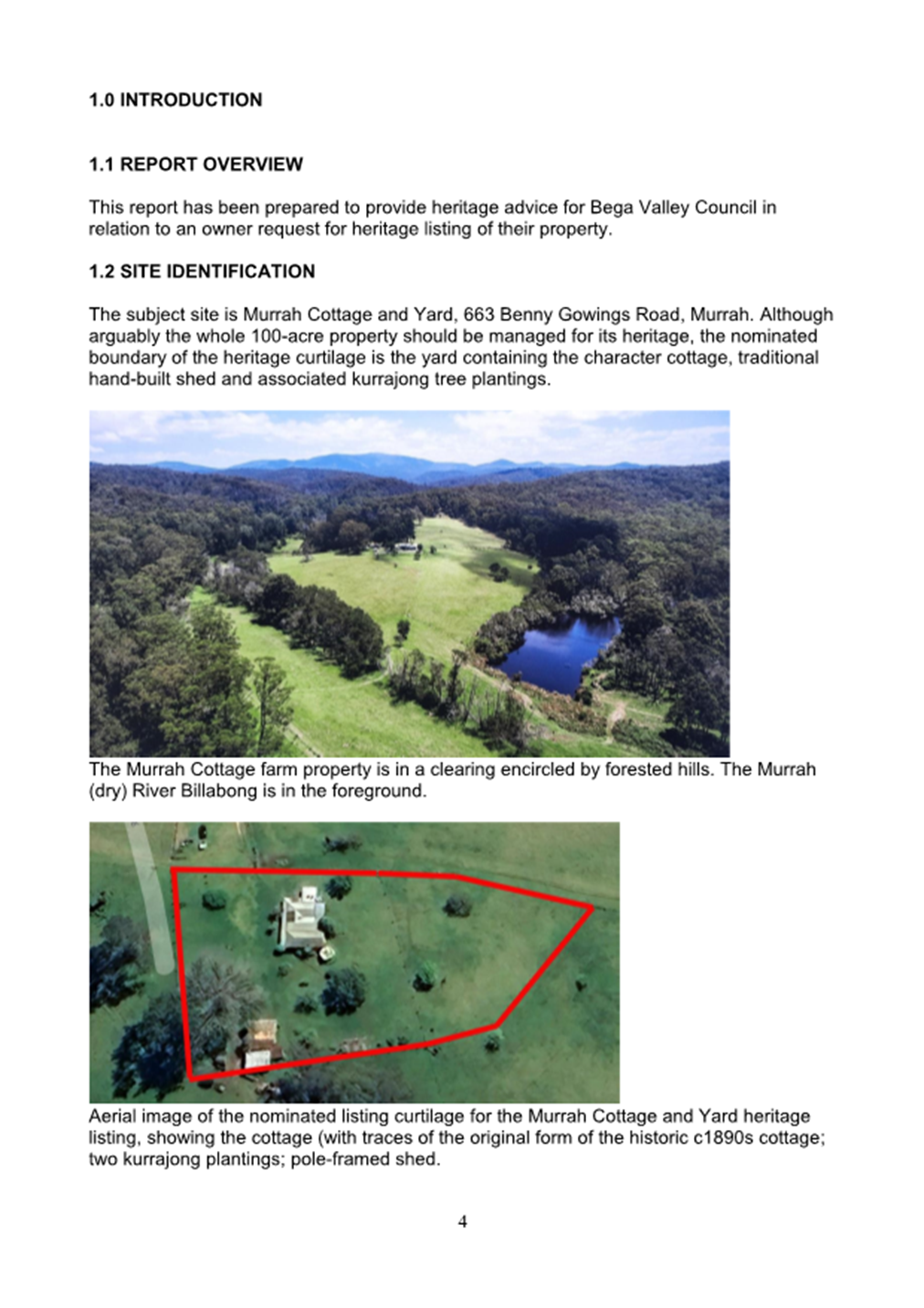

3. Add a heritage listing to 663 Benny Gowings Rd, Murrah at the owner’s request

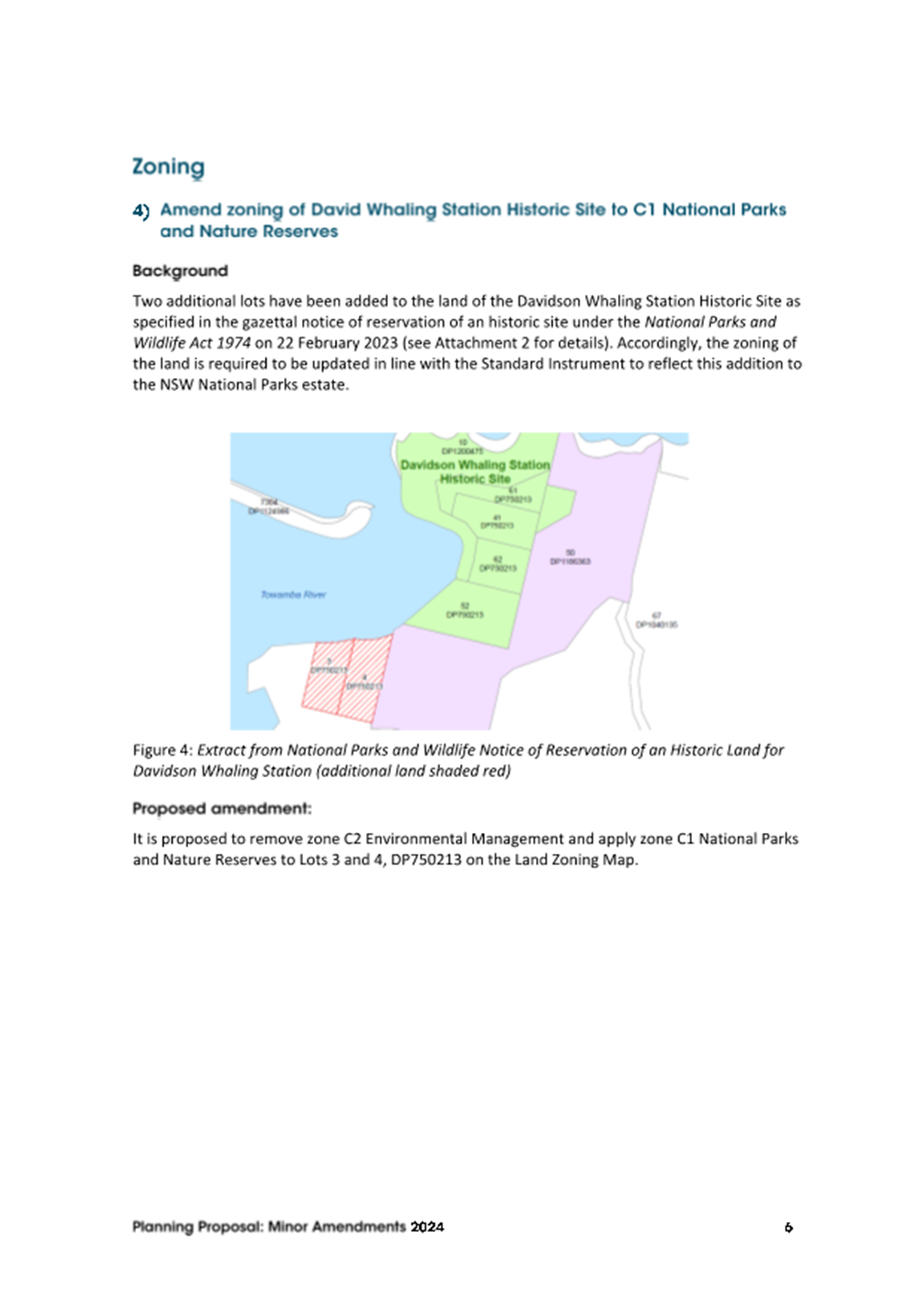

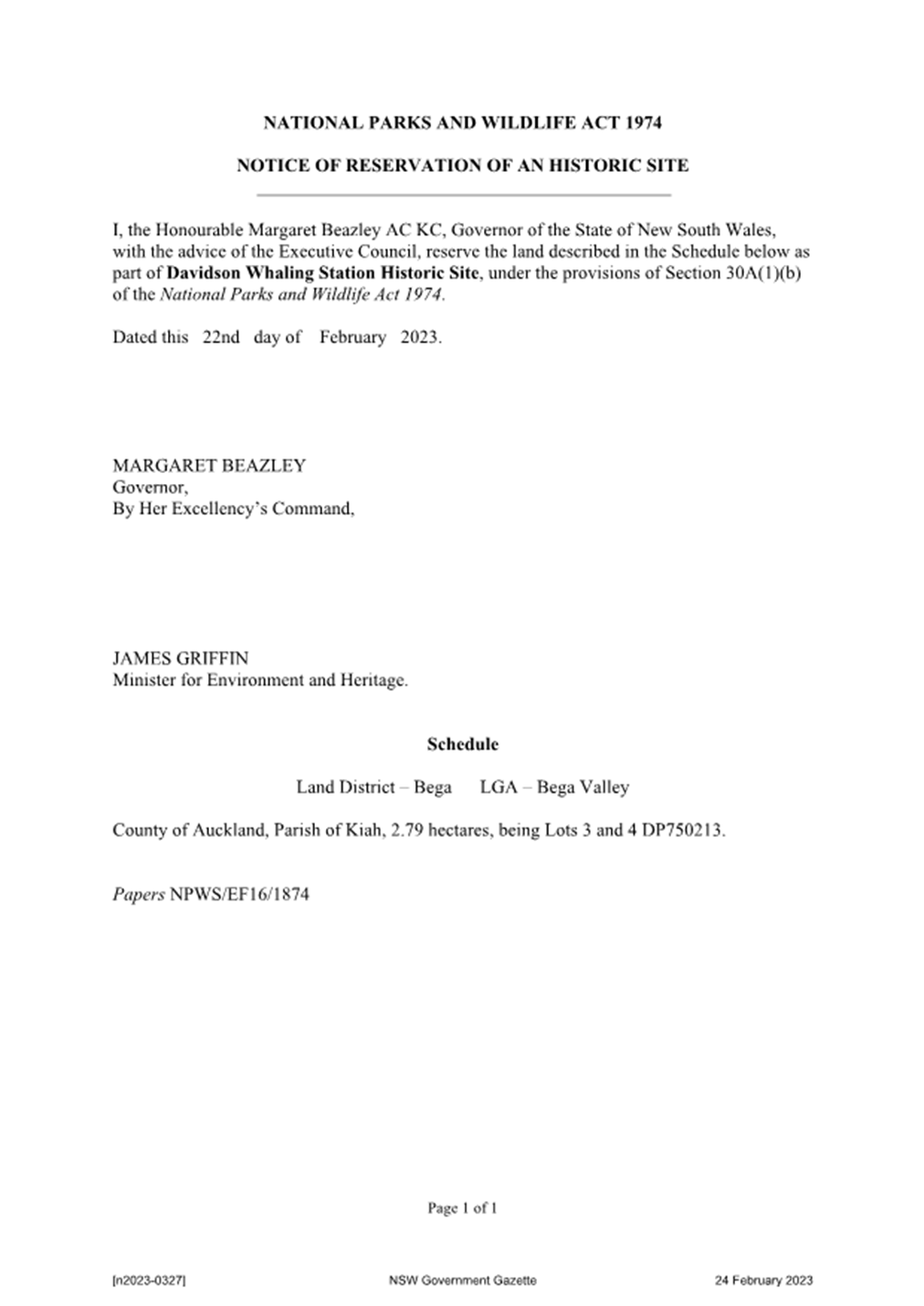

4. Zone David Whaling Station Historic Site C1 National Parks and Nature Reserves

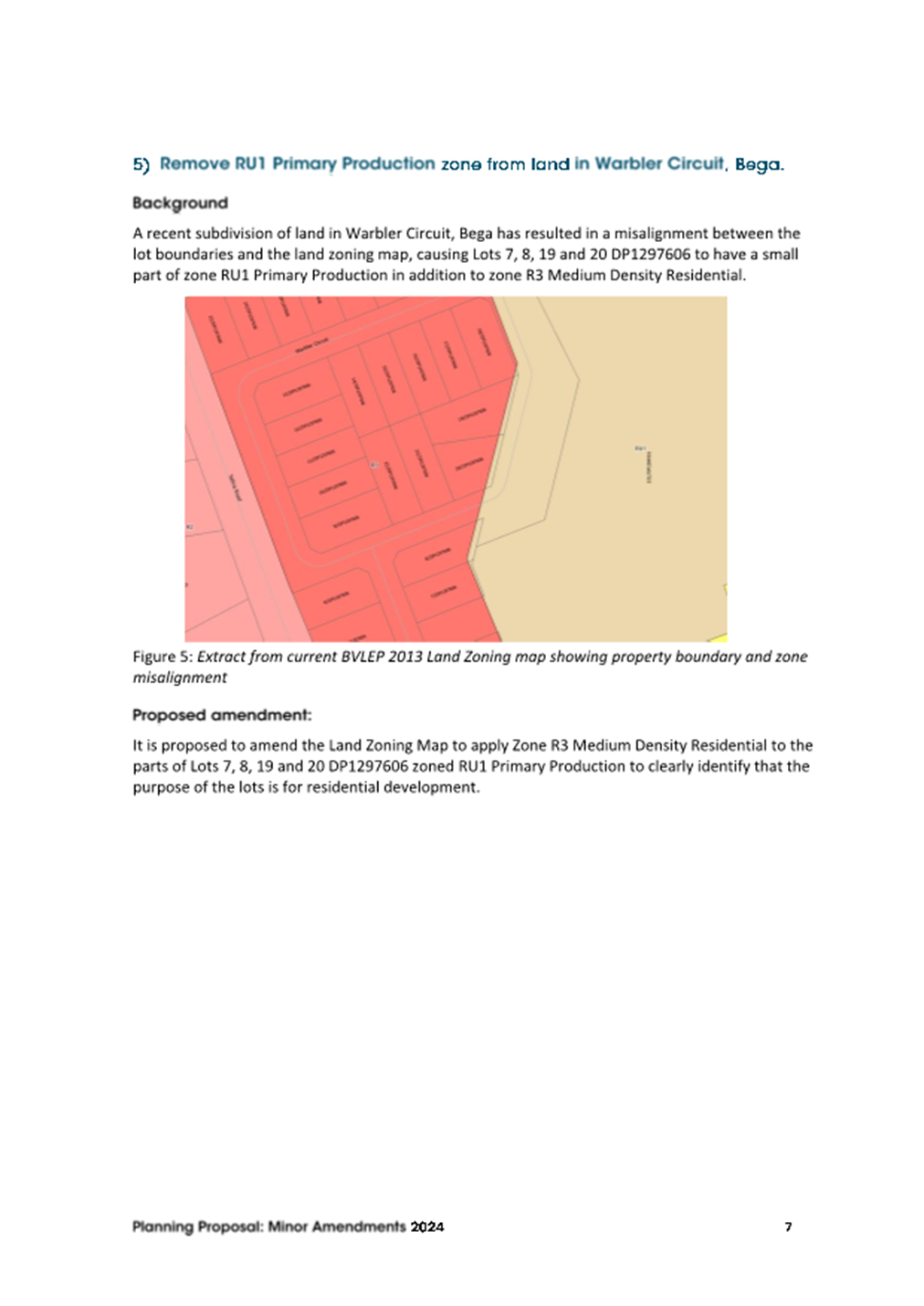

5. Remove zone RU1 Primary Production from land in Warbler Circuit, Bega following residential subdivision

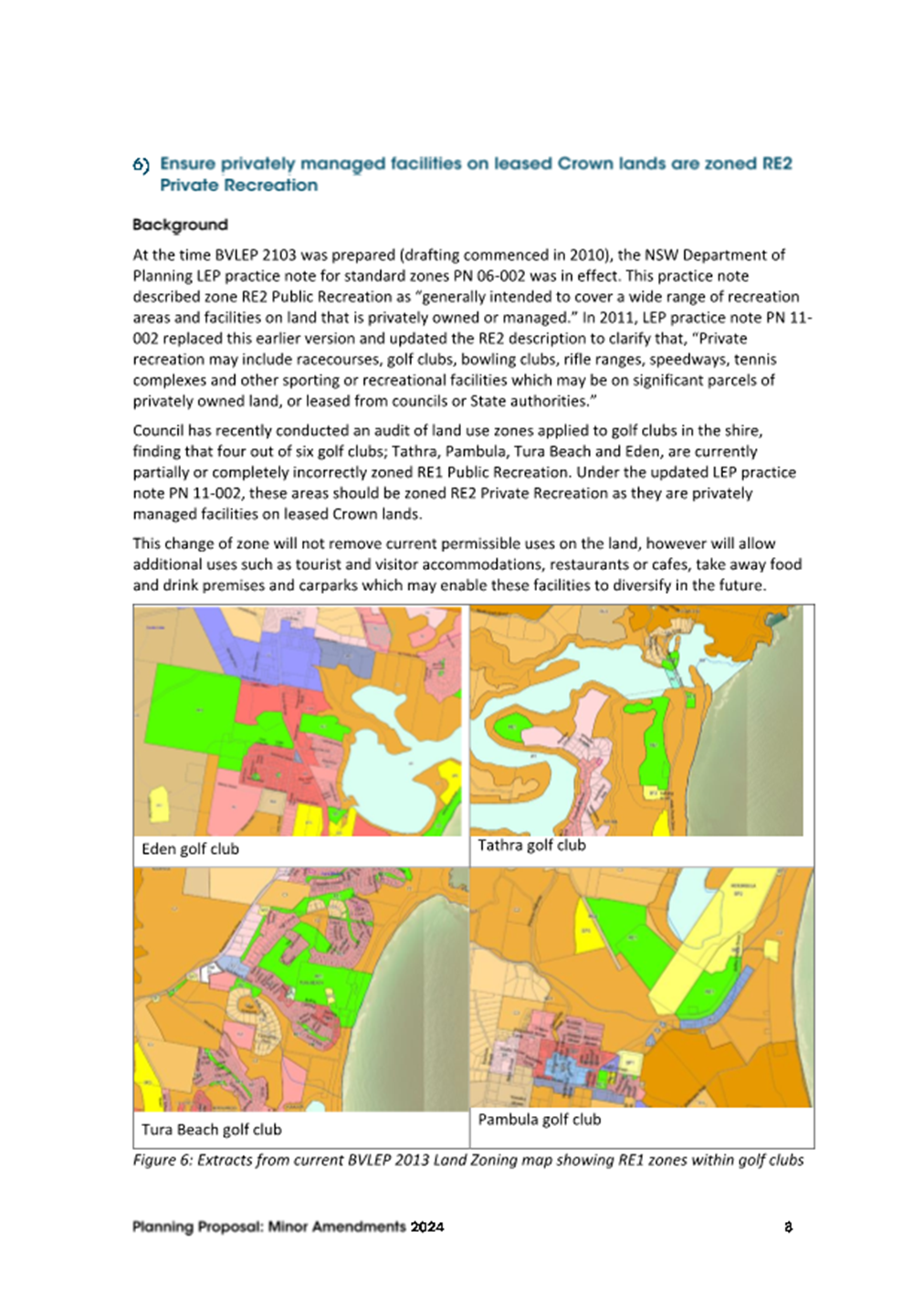

6. Ensure privately managed facilities on leased Crown lands are correctly zoned RE2 Private Recreation

7. Limit small lot community title subdivisions in the R3 Medium Density Residential zone to encourage housing diversity

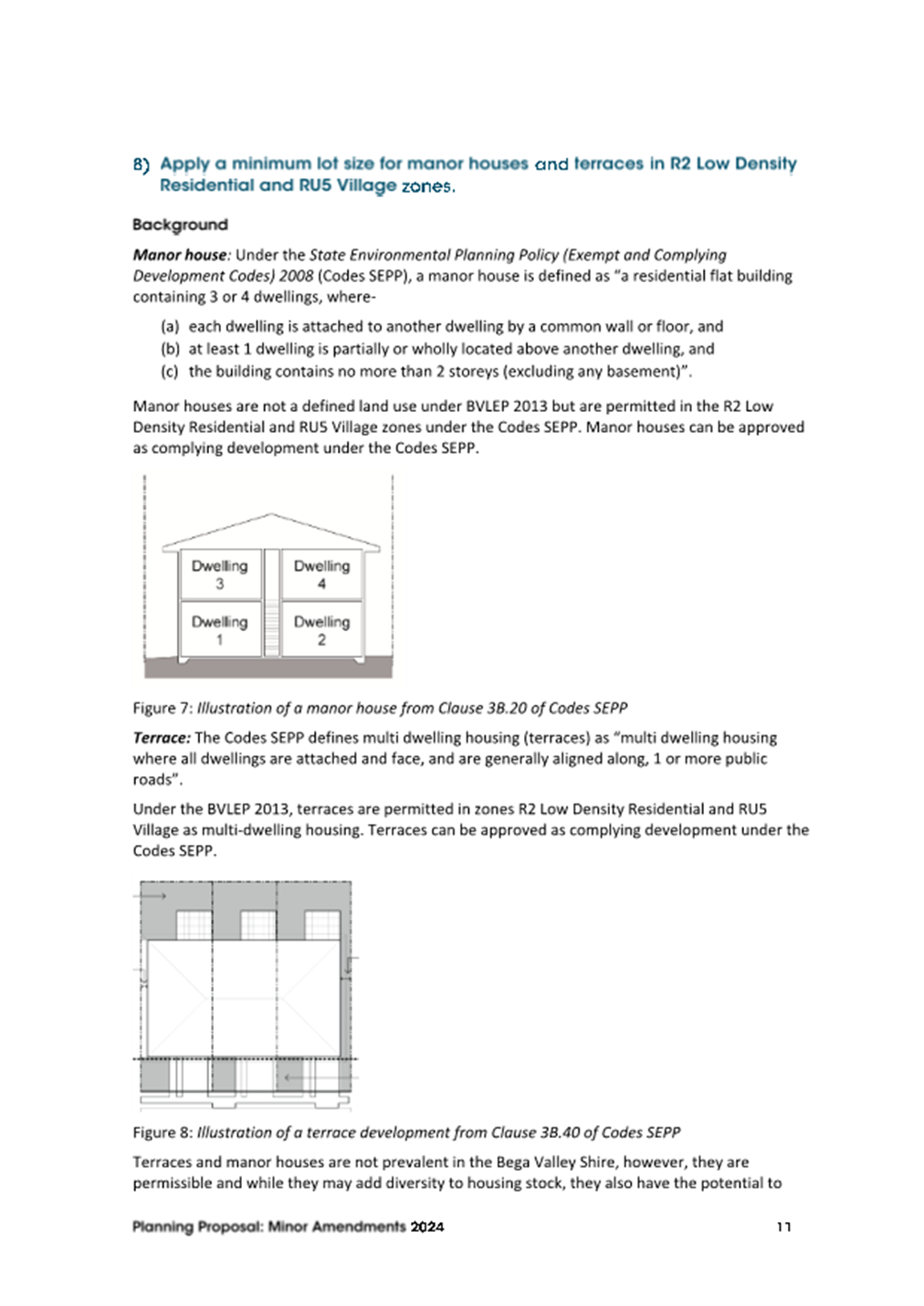

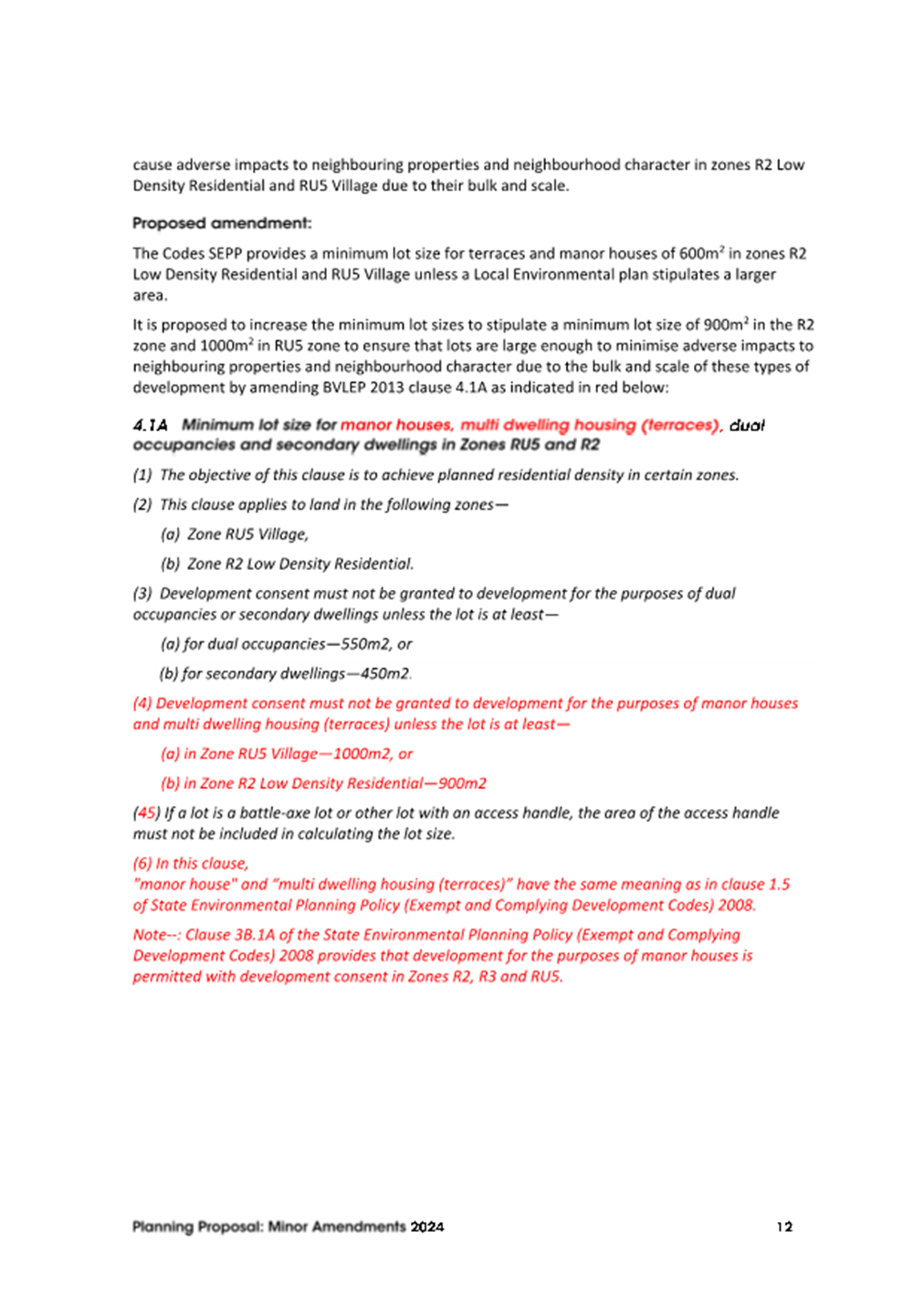

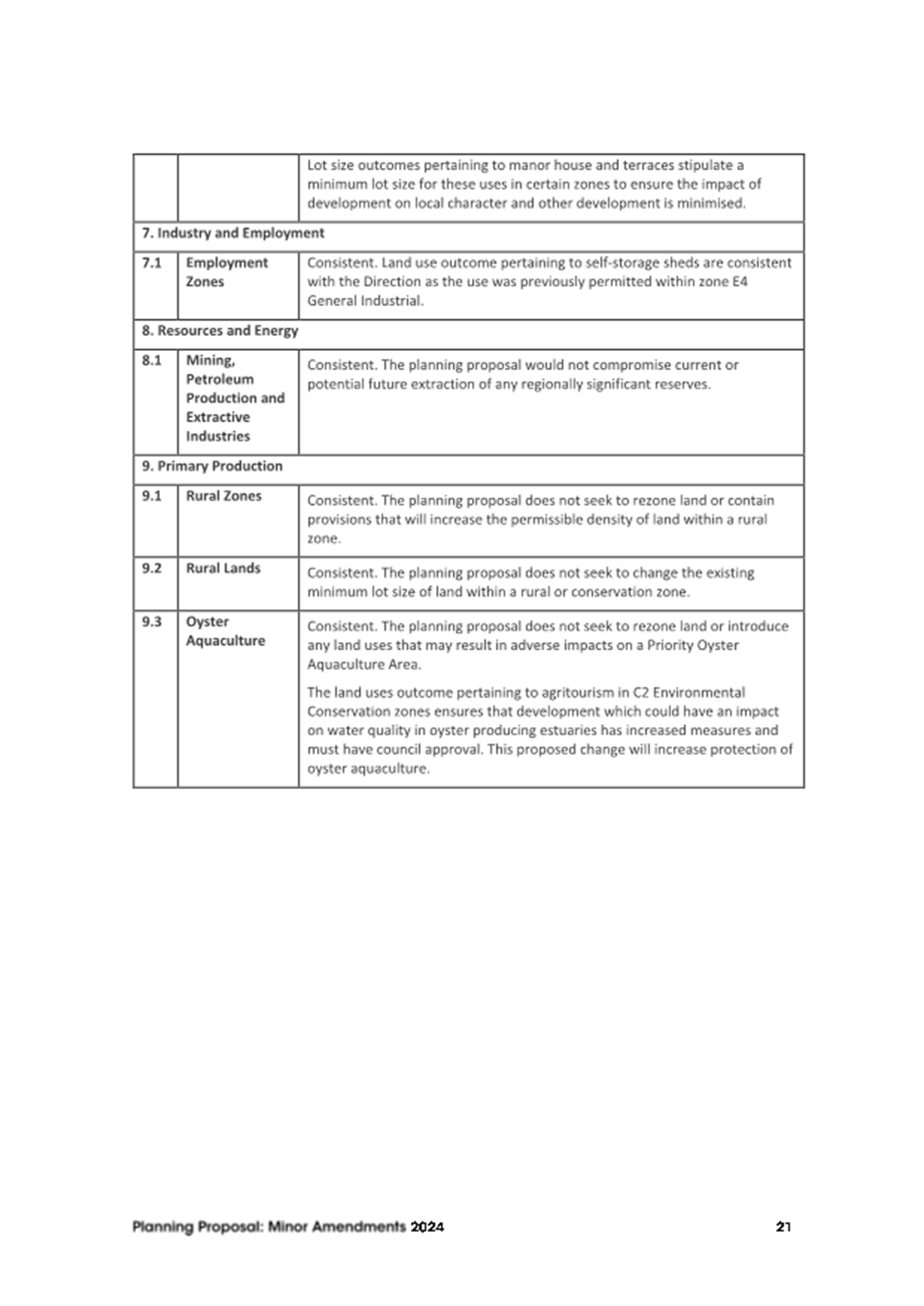

8. Apply a minimum lot size for manor houses and terraces in R2 Low Density Residential and RU5 Village zones to protect neighbourhood amenity and character from adverse development impacts

9. Allow subdivision to create first title resulting from Council-owned road closures as exempt development to streamline road closures processes

10. Permit cemeteries in C3 Environmental Management zone to ensure consistent application across other non-urban areas

11. Permit self-storage units in E4 General Industrial zone to rectify an error

12. Permit co-living housing in R2 Low Density Residential zone to encourage housing diversity

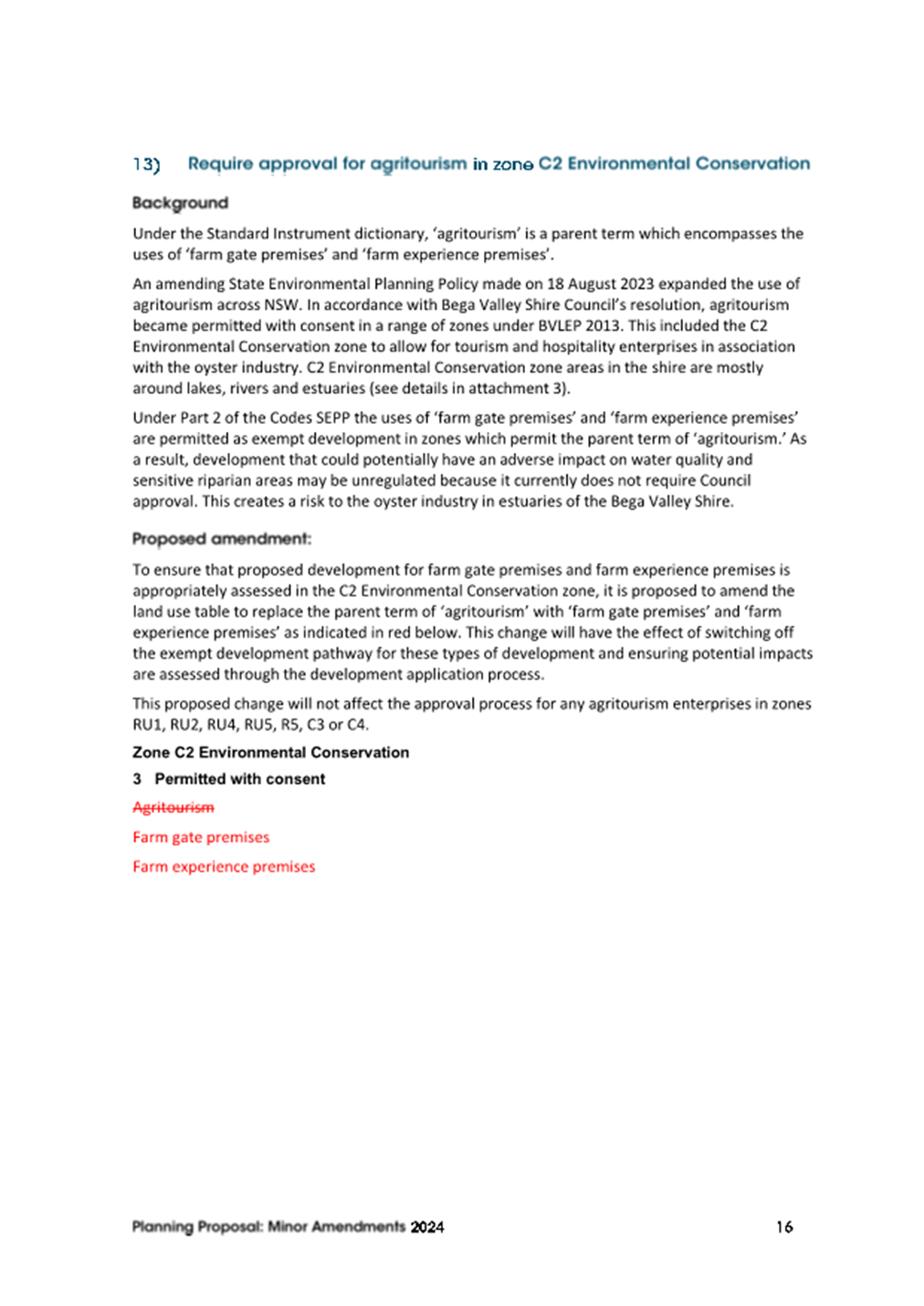

13. Require Council approval for agritourism in C2 Environmental Conservation zone to protect water quality in oyster catchments

The rationale and impact of each change is explained in the planning proposal (Attachment 1).

Strategic merit assessment criteria

The planning proposal:

· is not inconsistent with the South East and Tablelands Regional Plan 2036

· is not inconsistent with the Bega Valley Shire Local Strategic Planning Statement

· does not respond to a change in circumstances that has not been recognised by the existing planning framework.

Site-specific merit assessment criteria

The planning proposal does not include provisions that will unreasonably:

· increase the likelihood of additional impacts on the natural environment or other affected land

· increase the likelihood of additional impacts to existing uses, approved uses, and likely future uses of land in the vicinity

· impact services and infrastructure that are or will be available to meet demand.

This planning proposal is the seventh minor amendments (or housekeeping) planning proposal prepared by Council since the gazettal of BVLEP 2013.

Options

This report recommends that Council support the planning proposal to make minor, but important amendments to BVLEP 2013. These changes are important to ensure that BVLEP 2013 meets the requirements of landowners, the wider community and Council’s strategic directions.

Council could choose to not make these changes and the error, omissions, inconsistencies and issues would remain as there is no other avenue to make the proposed changes other than through the planning proposal process.

Community and Stakeholder Engagement

Engagement undertaken

No community consultation has yet been undertaken, however, Council staff have had conversations with property owners regarding the proposed amendments to the heritage schedule and re-introduction of self storage units to the E4 General Industrial zone.

Engagement planned

Community consultation for this planning proposal will be consistent with the requirements of the Bega Valley Shire Community Engagement Strategy, being a minimum exhibition timeframe of 28 days or as specified by the Gateway Determination.

Public exhibition of the planning proposal will include notification on Council’s website.

Should agency or community feedback be received that warrant substantial changes to the planning proposal, a further report will be prepared for Council outlining the submissions received and any changes to the planning proposal recommended in response to those submissions prior to resolving whether to proceed with amending BVLEP 2013.

If no objections to the planning proposal are received and no substantial changes are required to the planning proposal, it is recommended that Council resolve to authorise staff to proceed to finalise the proposed amendments to BVLEP 2013.

Financial and Resource Considerations

The processing of the planning proposal and its public exhibition will be undertaken as part of Council’s regular work program.

Legal /Policy

The planning proposal has been prepared in accordance with Section 3.33 of the Environmental Planning and Assessment Act 1979 and the NSW Department of Planning and Environment’s Local Environmental Plan Making Guideline (August 2024).

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

The planning proposal is consistent with the South East and Tablelands Regional Plan 2036, Bega Valley Community Strategic Plan 2024, and the Bega Valley Shire Local Strategic Planning Statement.

Environment and Climate Change

The planning proposal is largely administrative in nature and will not materially increase the risks associated with climate change or result in any significant impacts on the environment. The proposed amendment to the approval pathway for agritourism development in the C2 Environmental Conservation zone will ensure potential impacts on riparian areas and water quality are adequately addressed.

Economic

The planning proposal is largely administrative in nature and will not result in any significant positive or negative economic impacts.

Risk

The planning proposal seeks to address a broad range of risks to Council and the broader community by correcting an error, removing inconsistencies, ensuring that certain desirable land uses are permitted with consent, and reducing the risk of impacts to water quality in oyster catchments from unregulated agritourism development.

Social / Cultural

The planning proposal is largely administrative in nature and will not result in any material positive or negative social or cultural impacts.

Attachments

1⇩. Minor Amendments Planning Proposal 2024

|

Council |

27 November 2024 |

Staff Reports – Assets and Operations

27 November 2024

9.1 Request for Tender (RFT) 2425-010 Bemboka Reservoir Renewal.................................................... 2

9.2 Waste Grants Program FY 2025-26 to FY 2028-29... 2

9.3 Request for Tender (RFT) 2324-064 Brogo Tank 2 Replacement............................................................. 2

9.4 Regional Airport Program Round 4 (RAP4) Application............................................................... 2

9.5 Merimbula Airport Taxiway Charlie Culvert Upgrade - RAP3....................................................................... 2

|

Council 27 November 2024 |

Item 9.1 |

9.1. Request for Tender (RFT) 2425-010 Bemboka Reservoir Renewal

This report outlines the evaluation of Request for Tender RFT 2425-010 for the replacement of the existing Bemboka water reservoir and recommends negotiation with the preferred tenderer prior to awarding a contract.

Director Assets and Operations

1. That Council accepts the recommendations outlined in the attached Confidential Memo.

2. That Council rejects all tenders under clause 178 of the Local Government (General) Regulation 2021 and enter into negotiations with the preferred tenderer, with the intention to award a contract subject to variations and provisional sums.

3. That authority is delegated to the Chief Executive Officer to execute all necessary documentation in relation to tender RFT 2424-010.That all tenderers be advised of Council’s decision.

Executive Summary

This report evaluates RFT 2425-010 which seeks appropriate tenders for the replacement of the existing bolted-steel water reservoir at Bemboka. The tender seeks a qualified contractor to construct a new reservoir adjacent to the existing structures, with an optional provision for the demolition of the two existing reservoirs.

The reservoir is crucial infrastructure as it stores and supplies water to the township of Bemboka, however it has now reached the end of its serviceable life. The height requirement of the tank poses specific challenges in construction hence tenderers had an open brief to provide suitable compliant solutions.

All tender submissions have been assessed according to Council’s procurement criteria, with detailed evaluations provided in the attached confidential memo. After thorough review, a preferred contractor has been identified for the project.

Background

In 1988, Bemboka Reservoir 2 was constructed to replace Bemboka Reservoir 1. Reservoir 2 is a 430 kilolitre, 15m high tank with an anticipated design life of 25 years. It is currently operational and has been in service for approximately 36 years. The height of the tank is necessary to ensure that the pressure requirements of the town are met. Reservoir 1, a small unroofed concrete tank, is not able to supply water to the town due to lack of hydraulic pressure.

In 2019, Reservoir 2 was found to be leaking and corroding significantly on the outer surface. After the attempts to seal the leak in May 2020 were found to be ineffective, a formal condition assessment was conducted in February 2021. The inspection found significant corrosion inside the tank and it was concluded that the reservoir had reached the end of its serviceable life. A bypass system was installed in 2022 to mitigate the risk of tank failure and enable isolation of the tank.

Council sought tenders for the design and construction of a replacement tank, which is proposed to be built adjacent to the existing Reservoir 2. The location was chosen so that the existing reservoir could remain online during the construction of the new tank, minimising disruption to the water supply of Bemboka. Due to the specific height requirement, the scope allowed submissions for various tank construction types (e.g. steel, concrete, water tower), allowing Council to assess which type would be best for long term reliability and value. Additionally, Council requested provisional pricing for the demolition of both Reservoir 1 and Reservoir 2, as maintaining these decommissioned reservoirs would result in unnecessary costs and safety risks.

Tenders were advertised on the NSW Government eTendering system and local newsletters. Tenders were open from 27 August 2024 and closed on 01 October 2024. There was a non-mandatory site meeting conducted on 11 September 2024.

Five conforming tenders were received by the due date, supplemented by three non-conforming tenders. The tender evaluation was carried out in accordance with the Tender Evaluation Plan using a weighted scoring of 50% price and 50% non-price criteria. A preferred tenderer was identified in this process.

Options

Staff have considered several options which are presented below:

1. Enter contract negotiations with the preferred tenderer to construct a new bolted-steel reservoir (either glass-fused-to-steel (GFS) or fusion-bonded-epoxy (FBE)) and demolish both existing Reservoir 1 and Reservoir 2 (Recommended).

This option ensures a reliable water supply for Bemboka while eliminating the ongoing maintenance costs and negative visual impact of the decommissioned reservoirs. Council intends to enter contract negotiations to explore an FBE tank as a potential option which may result in cost savings when compared to a GFS tank. Demolition poses some challenges due to the proximity of power lines; however, further investigations will be conducted regarding potential power outages. Councillors and the community will be informed of any findings before work begins.

2. Enter a contract to construct a new steel reservoir and retain the two existing reservoirs (Not Recommended).

Even when decommissioned, the existing reservoirs would still require costly maintenance to preserve their structural integrity. Retaining them presents significant safety risks and would create an undesirable visual impact by having three reservoirs on the same site which is visible from the main road. Since these tanks would no longer serve a function, it would be in the Council’s best interest to proactively remove decommissioned assets, promoting a more positive visual outcome.

3. Enter a contract to construct a new concrete reservoir and demolish both existing Reservoir 1 and Reservoir 2 (Not Recommended).

A net present value (NPV) analysis comparing a 100-year concrete tank to a 50-year steel tank shows that, even after replacing the steel tank at 50 years, the concrete option remains approximately $500,000 more expensive in current value. This additional cost for the concrete tank would be manageable within a 50-year budget. However, choosing concrete would still need to be justified by benefits such as alignment with the Council’s existing concrete reservoirs, which would streamline maintenance schedules across assets. Additionally, concrete offers a better surface for potential community artwork, if the township of Bemboka decides to pursue this.

4. Do nothing (Not Recommended).

The current tank was assessed in 2021 as having reached the end of its serviceable life. It poses a high risk of failure, which would severely disrupt Bemboka’s water supply and result in emergency procedures to maintain water supply for an extended period.

Community and Stakeholder Engagement

|

Internal/External |

Level of Engagement |

|

|

Water and Sewer Services – Assets Water and Sewer Services – Maintenance Water and Sewer Services – Network Operations Water and Sewer Services – Treatment Operations |

Internal Internal Internal Internal |

Involve Involve Involve Involve |

|

General Public |

External |

Inform |

Engagement undertaken

Council has previously engaged with the community in relation to the proposal to construct a new reservoir. Nearby residents were informed via letter drop that Council was inviting tenders for the construction of a new reservoir. The letter also included information on why this project is necessary and when works are expected to start. There have been no negative responses or feedback received by Council.

Notification of the tender was also included in the BVSC Business newsletter dated 30 August 2024

Engagement planned

Once the tender has been awarded, a second round of communication will be issued via letter drop to all residents informing them of the result of the tender and project information such as type of tank, timeframes, and any potential disruptions expected. This information will also be made available via a project page on Council’s website and media posts, along with updates as the project reaches important milestones. Additionally, residents will be contacted via letter drop prior to any disruptive activities once the specific dates are known.

Financial and Resource Considerations

|

$ Excl GST |

|

|

Expenditure Detail |

|

|

Contract Price |

Refer to Confidential memo |

|

Provisional Sum |

Refer to Confidential memo |

|

Contingency |

Refer to Confidential memo |

|

Total Expenditure |

Refer to Confidential memo |

|

|

|

|

Source of Funds |

|

|

Allocated project budget |

$614,000.00 |

|

Water and Sewer Services – Water Fund |

Refer to Confidential memo |

|

Total income available |

|

|

Project funding shortfall |

Refer to Confidential memo |

Financial Option Impacts | Life Cycle Costing

|

Ongoing Financial Impacts |

$ Excl GST |

|

Capital Investment | Renewal |

Refer to Confidential memo |

|

Depreciation costs |

The new asset will be depreciated over 50 years |

Legal /Policy

The tender process complied with Section 55 of the Local Government Act 1993, part 7 of the Local Government (General) Regulation 2021 and Section 171 of the Local Government Regulations.

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

DP C.1.1 Operate a contemporary local water utility that enables sustainable development, supports social wellbeing and protects the environment.

OP C.1.1.2 Operate and maintain water supply and sewage network systems to meet health and environmental regulatory requirements and level of service objectives.

Environment and Climate Change

· Improve water storage efficiency and operations by minimising water loss currently occurring by leaks in the current tank.

· Enhance long term resilience to climate change by providing a reliable water supply during dry spells or bushfires, reducing our vulnerability.

Economic

Selecting a high-quality reservoir manufacturer and the use of durable materials will reduce the frequency and cost of repairs, inspections, and routine maintenance over time, leading to significant long-term savings for Council.

The proposal will have an immediate economic benefit during construction. The preferred tenderer has committed to using several local suppliers and subcontractors. This will promote jobs in the area as well as exposing local people to specialist skills, technologies and experience in the water treatment industry.

Risk

The current tank is failing and poses a high risk to operation. While attempts have been made to repair the tank, it is now necessary to construct a replacement. This project will mitigate the high risk of tank failure which poses significant operational risks.

Social / Cultural

Cultural heritage matters have been assessed as part of the REF process.

Attachments

1. Confidential memo RFT-2425-010 Bemboka Reservoir (Confidential - As this attachment contains commercial information of a confidential nature that would, if disclosed (i) prejudice the commercial position of the person who supplied it; or (ii) confer a commercial advantage on a competitor of the Council; or (iii) reveal a trade secret as per Section 10A(2)(d) of the Local Government Act 1993.

Although the above relates more explicitly to the discussion of closed business, it also forms part of the basis of justification as to why information relied upon in informing the public decisions made by Council are kept confidential. To consider this confidential material in open Council would be, on balance, contrary to the public interest (as defined in Section 14 of Government Information Public Access (GIPA) Act 2009) as it would potentially disclose private business information provided by tenderers in a confidential tender process and would also impact Council’s position in relation to its consideration, therefore impacting the tender process. This meets the requirements of Sect 10 D of the Local Government Act 1993 if Council were to close the meeting to discuss the details of individual tenderers.

|

Council 27 November 2024 |

Item 9.2 |

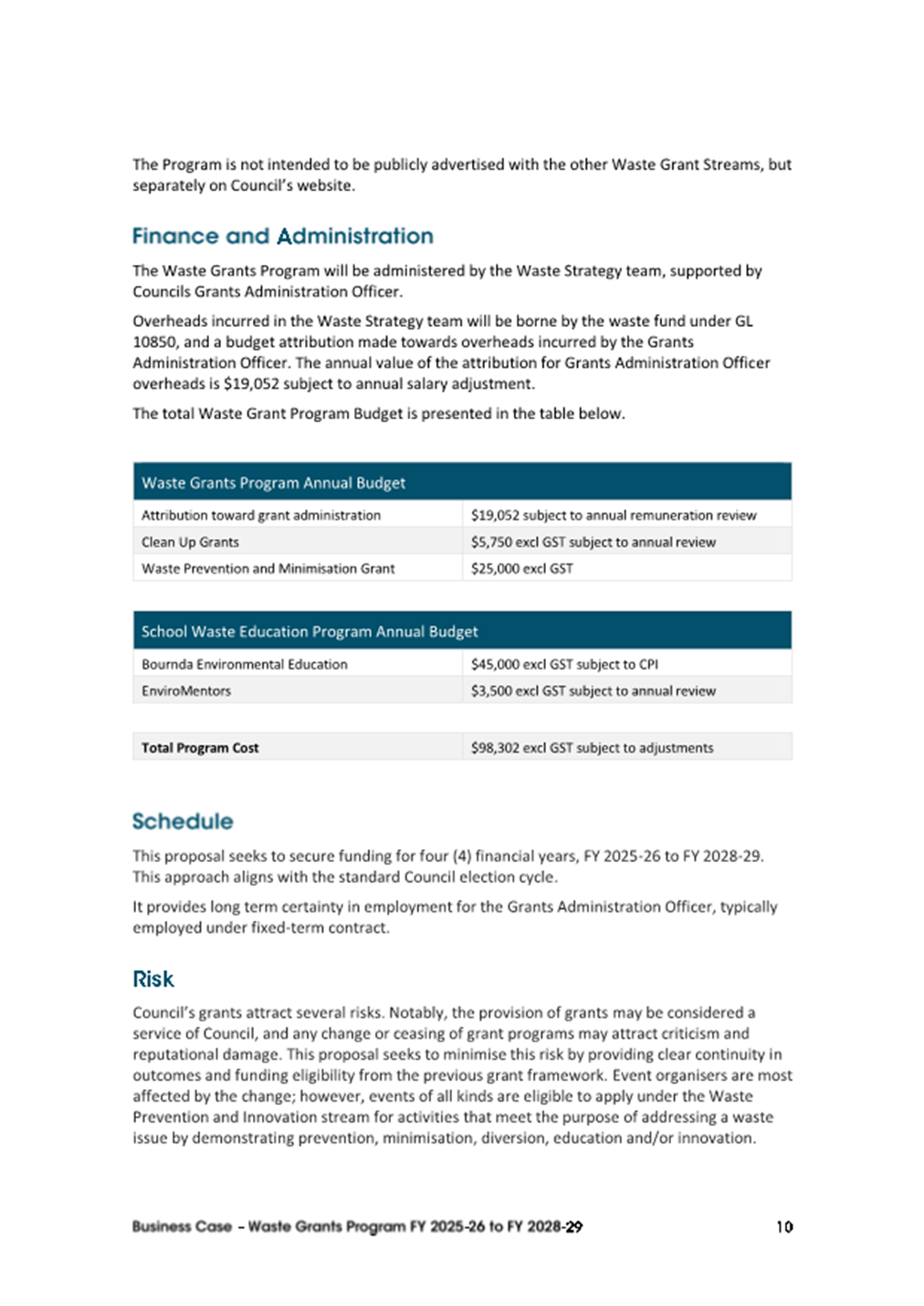

9.2. Waste Grants Program FY 2025-26 to FY 2028-29

This report is seeking approval of scope and funding for the next term of the Waste Grants Program from Council.

Director Assets and Operations

That Council approve the Business Case for the proposed Waste Grants Program for Financial Years 2025-26 to 2028-29.

Executive Summary

Council’s current Waste Grants Program was funded for three years up to Financial Year 2024-25. Further funding approval is required to continue the program.

Grant funding enhances the efforts of community members and volunteers as they work across the Shire to deliver projects, activities and events which benefit the community and which Council alone could otherwise not deliver. By providing waste and resource recovery-based grants, recipients who can demonstrate value for money using measures such as volunteer hours, co-funding or tonnes of waste diverted, assist Council in achieving its overall aims of increased community-led waste diversion and innovative approached to resource recovery.

A detailed business case has been developed to continue Council’s Waste Grants Program into the future. The recommended option is to streamline and restructure the program to improve governance and administration, whilst achieving Council’s waste and resource recovery objectives.

Background

Council’s Waste Grants Program has been providing funding to eligible applicants under five streams:

· Small Waste Grants

· Community Waste Minimisation Grants

· Waste Wise Events Grants

· School Waste Program

· Let’s Get It Sorted Program (directly funding Bournda Environmental Education Centre)

Program costs were budgeted at $118,912 excluding GST in Financial Year 2024-25. This amount included $19,052 towards salary and wages for Council’s Grants Administration Officer. The existing program is deemed to have run its course and usually does not expend all its budget under the program.

The recommended option reduces the funding budgeted to the program overall, whilst maintaining the most valued and impactful elements (as observed by Council staff and supported by community survey data) to limit public pushback on financial expenditure vs reduced services.

Options

The recommended option is to revitalise the Waste Grant Program per the “Scope – Proposed Program Structure” Section. This would see a reduction of approximately $20,000 per annum in overall funding under the program, and refine the scope to three streams:

· Clean-up Grants

· Waste Prevention and Innovation Grants

· School Waste Education Program

A do-nothing option would involve completely defunding and ceasing the program of waste grants.

An alternative option would be to continue the Waste Grants Program under its current structure and funding guidelines.

Community and Stakeholder Engagement

The impact and reach of the Waste Grants Program were assessed using the AIP2 Framework. The whole program can be considered to have moderate community impact, and moderate community scale, in large part due to the reach of the School Waste Education Streams. This involves a responsibility to “Inform – Consult – Involved – Collaborate”.

Assessing only those streams with more significant change, the community impact is assessed as being moderate, with lower community scale. This involves as responsibility to “Inform – Consult”.

The proposal has been socialised internally and externally with most relevant stakeholders.

Engagement undertaken

As the Grant Administration Officer provides support to other areas of Council, notably the Environment Team, and works under the Corporate Planning and Improvement department, they have been consulted in the development of this business case.

The community was broadly engaged through the “Waste Service Review and Customer Satisfaction Survey” with results strongly in favour of ongoing waste education. Whilst waste grants did not record high levels of engagement or satisfaction as a service area, the grants are a means of achieving education and prevention and diversion outcomes, all of which scored strongly in community desire for Council action.

Bournda Environmental Education Centre have been consulted on the proposed changes to the School Waste Education Program. A formal response in support of the School Waste Education Program is attached.

Some local events stakeholders have been consulted with generally positive comments however there are still some reputational risks.

Engagement planned

The most impactful change is in ceasing the Waste Wise Events Grants Stream. There are several notable applicants each year.

· Eat Merimbula Festival

· Yuin Folk Festival

· Cobargo Show

· Bega Show

· Candelo Village Festival

Should the recommended option be approved, Council’s waste team will contact the organisers for each event and explain the change in grant streams, and how they may still apply for funding under the Waste Prevention and Innovation Grants Stream.

Broader community engagement will be undertaken via clear communication on Council’s website and usual communications channels, and through the grant application process. The Grants Administration Officer will provide information to regular grant recipients via direct email prior to the next grant round opening.

Financial and Resource Considerations

Funding is sourced from waste revenue and does not rely on General Funds. A small grant attribution is received from the Canberra Region Joint Organisation (CRJO) waste education funding but is reported and managed separately. The figures provided below are annual costs for year one of the program, which will be adjusted annually per the business case for the program duration.

|

Item |

$ Excl GST |

|

Expenditure Detail |

|

|

Attribution toward grant administration |

$19,052 subject to annual remuneration review |

|

Waste Grants Program |

$30,750 subject to annual review |

|

School Waste Education Program |

$48,500 subject to annual review |

|

Total Expenditure |

$98,302 subject to annual adjustments |

|

|

|

|

Source of Funds |

|

|

Waste Fund |

$98,302 |

|

CRJO Waste Education Funding |

$4,300 |

|

Total income available |

$98,302 subject to annual budget adoption |

|

Project Funding Shortfall |

$0 |

Legal /Policy

Council manages its grant programs aligned to the NSW Governments best practice guidelines and templates for grant funding agreements, creating a legally binding framework that makes clear the responsibilities of grantors and grantees.

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

Providing grant funding for waste and resource recovery activities aligns with the Community Strategic Plan.

“We are leaders in sustainable living and support innovative approaches to resource recovery and the production of renewable energy and food.

C.3. Collaborate with partners and our community to support innovative approaches to waste minimisation and increase reuse and recycling opportunities.”

NSW state targets, set in support of the National Waste Policy Action Plan, aim to reduce total waste generated per person by 10% by 2030, have an 80% average recovery rate from all waste streams by 2030 and to halve the amount of organic waste sent to landfill by 2030.

Environment and Climate Change

The funding enhances the efforts of community organisations and volunteers in delivering waste-related projects, activities and events which benefit the whole of the community with a focus on sustainable living, education, minimisation and diversion.

By providing a waste and resource recovery-based grant, recipients who can demonstrate value for money using measures such as X numbers of volunteer hours, $Y of co-funding or Z tonnes of waste diverted, assist Council in achieving its overall aims of increased community-led waste diversion and innovative approaches to resource recovery.

Economic

The recommended grants program provides financial relief for organisations undertaking a cleanup of public reserves or assisting people with complex hoarding behaviours. They may also seed fund innovative approaches to waste management and prevention of waste.

Risk

Several risks have been identified in the Business Case and are described below.

1. Reputation: The provision of grants may be considered a service of Council, and any change or ceasing of grant programs may attract criticism and reputational damage. This proposal seeks to minimise this risk by providing clear continuity in outcomes and funding eligibility from the previous grant framework. Event organisers are most affected by the change; however, events of all kinds are eligible to apply under the Waste Prevention and Innovation stream for activities that meet the purpose of addressing a waste issue by demonstrating prevention, minimisation, diversion, education and/or innovation.

2. Financial: Any financial transaction risks fraud or misuse. This risk is minimised by clear eligibility criteria for applicants and project activities. Evidentiary requirements for expenditure are still necessary to claim funding. Reporting is streamlined so it is appropriate to the amount of funding offered.

3. Safety and inclusion: Council liability is mitigated by adopting the NSW Governments best practice guidelines and templates for grant funding agreements, creating a legally binding framework that makes clear the responsibilities of grantors and grantees.

Social / Cultural

Educational activities, community events and public art that focus on waste themes are eligible for funding under the proposed program.

Attachments

1⇩. Community Waste Grants Business Case 2025-2028

2⇩. BEEC Feedback to BVSC 2025 Grant Framework Proposal

|

Council 27 November 2024 |

Item 9.3 |

9.3. Request for Tender (RFT) 2324-064 Brogo Tank 2 Replacement

This report outlines the evaluation of Request for Tender (RFT) 2324-064 for the replacement of the existing Brogo Tank 2 water reservoir and recommends award of a contract to the preferred tenderer.

Director Assets and Operations

1. That Council accepts the recommendations outlined in the attached confidential memo.

2. That Council accept the tender from xxxx in relation to the contract for the works described in in RFT 2324-064, in the amount of $xxx (incl. GST), subject to variations and provisional sums.

3. That authority is delegated to the Chief Executive Officer to execute all necessary documents in relation to tender RFT 2324-064.That all tenderers be advised of Council’s decision.

Executive Summary

This report evaluates RFT 2324-064 which seeks to replace the Brogo Tank 2 (BT2) concrete water reservoir.

Water and Sewerage Services have sought a qualified contractor to demolish the existing reservoir and construct a new concrete reservoir in the same location. BT2 is crucial infrastructure as it supplies water to the Brogo-Bermagui water system and its current structural condition poses challenges and risks. Despite attempts to rehabilitate the tank, it is no longer considered a viable option. Consequently, a replacement tank is considered a more durable option which presents lower long-term risks. A new concrete reservoir will provide the most beneficial and secure outcome for the Brogo-Bermagui water supply system.

All tenderer submissions have been assessed according to Council’s procurement criteria, with detailed evaluations provided in the attached confidential memo. After thorough review, a preferred contractor has been identified for the project.

Background

The Brogo Tank 2 (BT2) is a reinforced concrete reservoir constructed in 1985 and has been in service for approximately 40 years. If built to current standards, concrete reservoirs are designed to last 80-100 years with proper maintenance. BT2 was constructed pre-1988, before durability clauses were first introduced to the Australian Standard for Concrete Structures (AS 3600). These clauses were designed to ensure that concrete structures would have a longer service life by addressing factors such as exposure to environmental conditions, material quality, and construction techniques. Despite this, Council owns other pre-1988 built reservoirs that remain operational and are not scheduled for replacement. While the exact cause of failure for BT2 is difficult to determine, poor construction methods are likely a key contributing factor. Built at a similar time, Brogo Tank 1 (BT1) also prematurely reached the end of its expected service life and was replaced as part of the Brogo Water Treatment Plant project in 2021.

Structural degradation of the tank has been observed by operational staff over several years and was confirmed in two independent specialist reports completed in 2019. A bypass system was installed in 2022 to mitigate the risk of tank failure and enable isolation of the tank. Rehabilitation work was initiated in November 2023 under contract RFQ-2223-103 however only a portion of the contract was able to be completed as further issues were found in the internal joint material.

Subsequently, Council sought updated quotes for removal of existing joints and alternative methods for internal joint repairs. The revised costs were substantial and the proposed rehabilitation works would only extend the tank’s life by an estimated 20 years. The success of the repairs was also dependant on the soundness of the existing materials and accuracy of assumptions regarding the tank’s points of failure.

The high cost of rehabilitation, combined with uncertainty regarding its effectiveness, poses a significant risk. There is a strong possibility that after 20 years, either a new tank would need to be built or further costly repairs would be required. A replacement tank was determined as a more viable long-term solution. Since BT2 is within NSW State Forest, the existing tank must be demolished, and new tank built in the same location.

The current tank is approximately 1.6 megalitres (ML) capacity while the proposed replacement will have a reduced capacity of 1.0ML. A population study determined that the current capacity is significantly oversized and a 1.0ML operating capacity would be more than sufficient for the forecasted growth for the service life of the tank. This reduced size option will result in cost savings while continuing to provide long-term supply to the Brogo-Bermagui system.

Tenders were advertised on the NSW Government eTendering system and local newsletters. Tenders were open from 30 August 2024 and closed on 04 October 2024. There was a non-mandatory site meeting conducted on 11 September 2024.

Six conforming tenders were received by the due date. The tender evaluation was carried out in accordance with the Tender Evaluation Plan using a weighted scoring of 50% price and 50% non-price criteria. A preferred tenderer was identified in this process.

Options

1. Enter a contract with the preferred tenderer to demolish the existing reservoir and construct a new reinforced concrete reservoir in the same location (Recommended).

This option ensures a reliable water supply for the Brogo-Bermagui system while eliminating risk of costly repairs and risk of asbestos contamination.

2. Do repair work only (Not Recommended).

The rehabilitation of the reservoir would be complex, expensive and would not extend the life of the structure sufficiently to be worthwhile.

3. Do nothing (Not Recommended).

The current tank was assessed in 2021 as having reached the end of its serviceable life. It poses a high risk of failure, which would put unnecessary strain on the existing bypass assembly for an extended period.

Community and Stakeholder Engagement

|

Stakeholder Group |

Internal/External |

Level of Engagement |

|

Water and Sewer Services – Assets Water and Sewer Services – Maintenance Water and Sewer Services – Network Operations Water and Sewer Services – Treatment Operations |

Internal Internal Internal Internal |

Involve Involve Involve Involve |

|

General Public Forestry Corporation of NSW |

External External |

Inform Consult |

Engagement undertaken

Council has consulted the Forestry Corporation of NSW (FCNSW) for the purpose of sourcing a permit for Council, subcontractors, and sub-consultants to access and complete works within Cowarra State Forest. The permit includes the already installed bypass system and the proposed demolition and construction of the new reservoir.

As this is an internally driven project for essential infrastructure, there has not been any engagement with the general public as of yet.

Internal stakeholders from Water and Sewer Services have had ongoing involvement through the repair works and defining the project scope for the new reservoir.

Engagement planned

Council will engage with FCNSW with further details of the nature of works, access plans and machinery that are to be used as well as notice when work is timed to commence on site. Council will continue to promulgate any further information, clarification or approvals that may be required as the works progress.

General public engagement planned for the next phase of the project includes informing the residents and broader community via periodic media releases and updates to a project page on Council’s website.

Ongoing involvement will occur throughout the project duration with the internal Water and Sewer Services teams.

Financial and Resource Considerations

This project was started several years ago as a major repair to BT2 and approximately $100k was expended in the abortive repair due to excessive damage and asbestos content in the tank fabric and joints. A new project budget was set based on best estimates of costs and similar projects for full replacement.

|

Item |

|

$ Excl GST |

|

Expenditure Detail |

|

|

|

Contract Price |

|

Refer to Confidential memo |

|

Provisional Sum |

|

Refer to Confidential memo |

|

Contingency |

|

Refer to Confidential memo |

|

Total Expenditure |

|

Refer to Confidential memo |

|

|

|

|

|

Source of Funds |

|

|

|

Allocated project budget |

|

$1,080,000.00 |

|

Water and Sewer Services – Water Fund |

|

Refer to Confidential memo |

|

Total income available |

|

|

|

Project funding shortfall |

|

Refer to Confidential memo |

Financial Option Impacts | Life Cycle Costing

|

Ongoing Financial Impacts |

$ Excl GST |

|

Capital Investment | Renewal |

Refer to Confidential memo |

|

Depreciation costs |

The new asset will be depreciated over 100 years |

Legal /Policy

The tender process complied with Section 55 of the Local Government Act 1993, part 7 of the Local Government (General) Regulation 2021 and Section 171 of the Local Government Regulations.

Impacts on Strategic/Operational/Asset Management Plan/Risk

Strategic Alignment

The proposed new reservoir relates to the following actions and/or activities contained within Council’s Delivery Program 2022-25 and Operational Plan 2024-25 respectively:

DP C.1.1 Operate a contemporary local water utility that enables sustainable development, supports social wellbeing and protects the environment.

OP C.1.1.2 Operate and maintain water supply and sewage network systems to meet health and environmental regulatory requirements and level of service objectives.

Environment and Climate Change

A formal Review of Environmental Factors (REF) has been completed for the project outlining measures to protect the environmental values of the area during construction. In addition, the proposed new reservoir will:

· Improve water storage efficiency by minimising water loss currently occurring by leaks in the current tank.

· Enhance long term resilience to climate change by providing a reliable water supply during dry spells or bushfires, reducing our vulnerability.

· Remove the risk of contamination of asbestos to our water supply by safely removing the existing reservoir.

Economic

Constructing a new quality concrete reservoir will reduce the frequency and cost of repairs, inspections, and routine maintenance over time, leading to significant long-term savings for Council.

Risk

The project mitigates the risks of failure, contamination, or water shortages due to aging infrastructure. It will also provide enhanced safety with a structurally sound reservoir.

Social / Cultural

Attachments

1. Confidential memo RFT-2324-064 BT2 Reservoir (Confidential - As this attachment contains commercial information of a confidential nature that would, if disclosed (i) prejudice the commercial position of the person who supplied it; or (ii) confer a commercial advantage on a competitor of the Council; or (iii) reveal a trade secret as per Section 10A(2)(d) of the Local Government Act 1993.

Although the above relates more explicitly to the discussion of closed business, it also forms part of the basis of justification as to why information relied upon in informing the public decisions made by Council are kept confidential. To consider this confidential material in open Council would be, on balance, contrary to the public interest (as defined in Section 14 of Government Information Public Access (GIPA) Act 2009) as it would potentially disclose private business information provided by tenderers in a confidential tender process and would also impact Council’s position in relation to its consideration, therefore impacting the tender process. This meets the requirements of Sect 10 D of the Local Government Act 1993 if Council were to close the meeting to discuss the details of individual tenderers.

|

Council 27 November 2024 |

Item 9.4 |

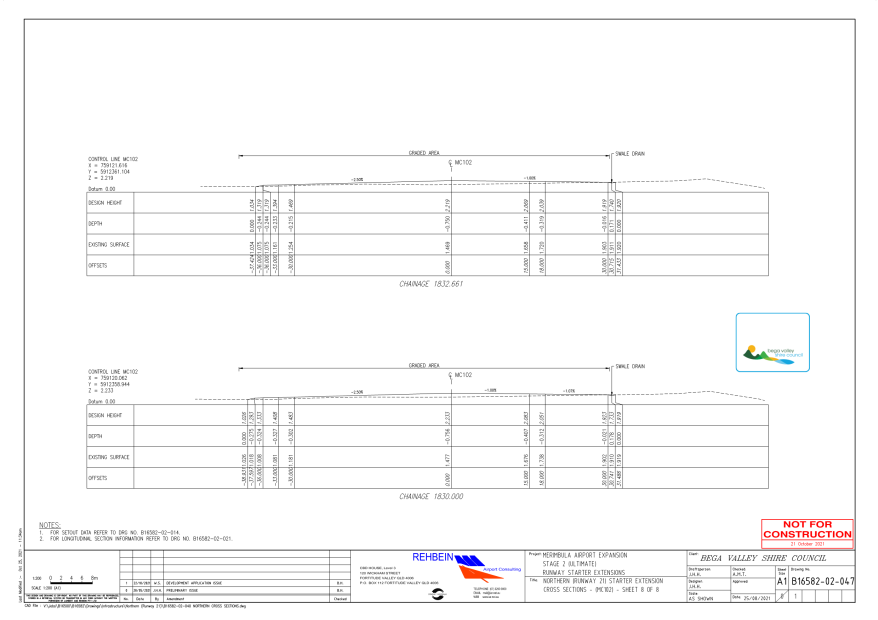

9.4. Regional Airport Program Round 4 (RAP4) Application

This report relates to a Regional Airport Program Round 4 (RAP4) application for the second stage of runway starter extensions for the Merimbula Airport and Council’s options to source funds for biodiversity offsets and a grant co-contribution for this project.

Director Assets and Operations

1. That Council notes that on 18 November 2024 Bega Valley Shire Council submitted a Regional Airport Program Round 4 (RAP4) application for $4 million to partially fund the $10 million Merimbula Airport runway starter extensions project, stage two.

2. That Council endorses Council officers to:

· Approach the NSW Government to fully fund the required co-contribution.

· Review Council’s LTFP to identify lower priority projects that can be delayed or withdrawn, and these funds be reassigned to this co-contribution and provide a further report to Council outlining these options

3. Should sufficient grant or redirected funds not be available, that Council endorses